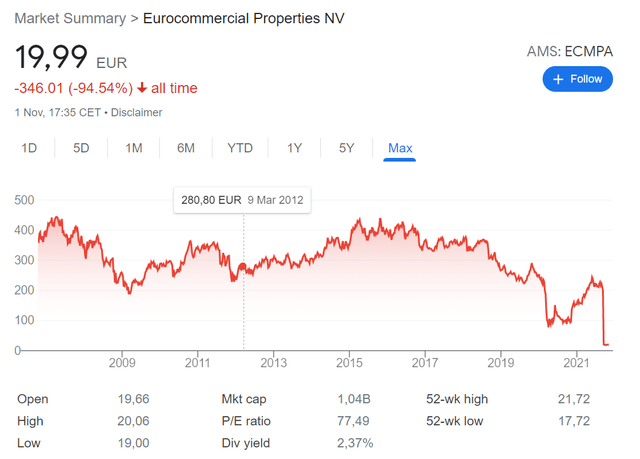

November 2, 2021

Eurocommercial Properties Stock Analysis – Yielding 9% EPRA

I don’t particularly like real estate stock investments because those are only great investments in times of crisis, but in... Continue reading

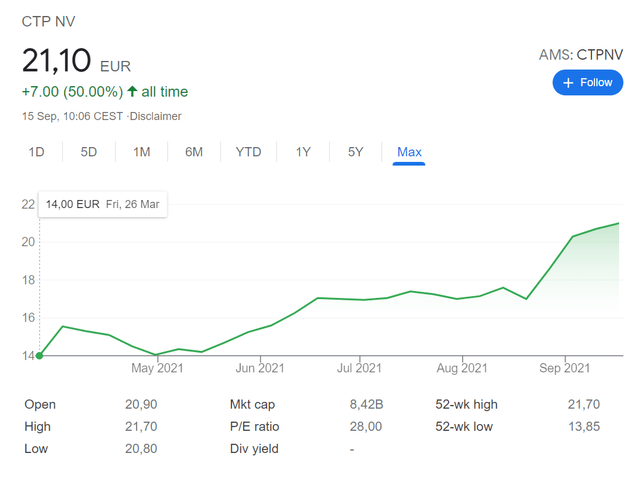

September 15, 2021

CTPNV Stock Analysis – Fast Growing Logistics (e-commerce) Play

This CTPNV stock analysis is part of my complete research on the Amsterdam stock exchange, stock by stock (you can... Continue reading

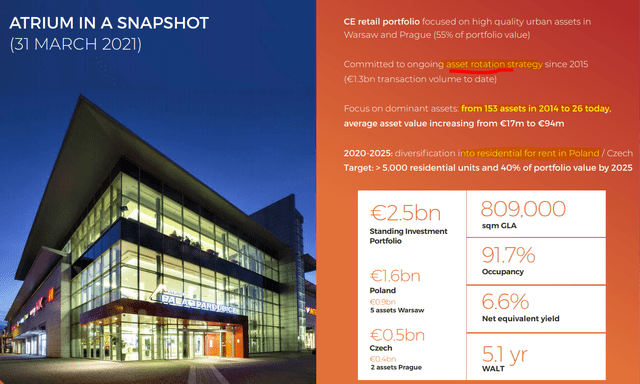

June 11, 2021

Atrium European Real Estate Stock Analysis – Poland REIT With 6% Dividend

This Atrium European Real Estate stock analysis (AMS: ATRS stock, VIE:ATRS) is part of my full analysis of every stock traded... Continue reading

May 11, 2021

Aedifica Stock Analysis – ‘We Are Getting Older’ REIT Investment

This Aedifica stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My... Continue reading

December 28, 2020

S Immo Stock Analysis – Good Dividend, Good Value

S Immo AG stock analysis is part of my full, stock by stock analysis of the Austrian Stock Market that... Continue reading

August 17, 2020

Immofinanz Stock Analysis – Risky Real Estate Business

Immofinanz AG is a European real estate company focused on offices, retail parks and shopping centres. This analysis will comprehend... Continue reading

June 25, 2020

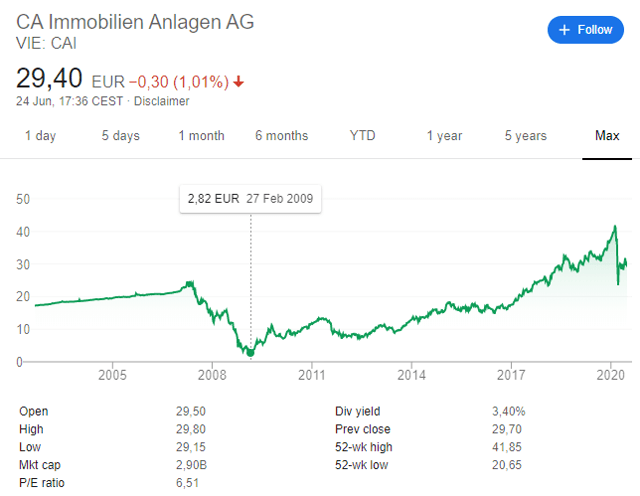

CA Immo Stock Analysis – Constant revaluations create houses of cards

This CA Immo stock analysis is part of my full analysis, stock by stock of all the stocks listed on... Continue reading

June 24, 2020

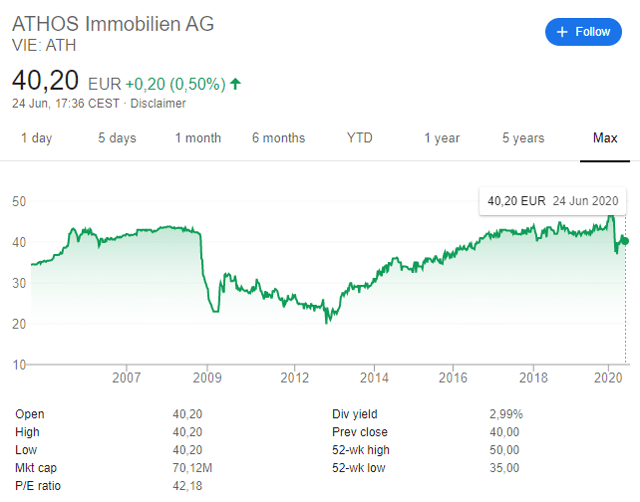

Athos Immobilien Stock Analysis – Own Homes In Linz (Simple and Easy)

Athos Immobilien Stock Vienna: ATH Athos Immobilien stock price Athos Immobilien stock analysis is part of my full analysis, stock... Continue reading

July 11, 2019

NorthWest Healthcare Properties REIT Stock Analysis – 10% Returns Possible

I’ve looked again at US healthcare REITs (Real Estate Investment Trusts) and other REITs and I sense high risk. There... Continue reading

June 12, 2019

How To Invest In REITs – Pros, Cons And Simon Property Group Example Analysis

Content: How To Invest In REITs – Pros, Cons And What Are REITs Introduction – REITs have been the best... Continue reading