Eurocommercial Properties Stock Analysis – Yielding 9% EPRA

I don’t particularly like real estate stock investments because those are only great investments in times of crisis, but in times of crisis you also have other amazing opportunities. So, as with other real estate stocks, the first thing to do is to understand the value creation pattern by adjusting for the accounting shenanigans, sorry, real estate revaluations or dividend distributions in stocks, and then understand exactly how much value is created.

Let’s analyse Eurocommercial Properties stock by first taking a look at the stock price, give a business overview, adjust the financials and conclude with an investment thesis.

This ECMPA stock analysis is part of my complete research on the Amsterdam stock exchange, stock by stock (you can check many more analyses there). My goal is to learn about as many businesses that I can find and then select those that I think can offer interesting, low risk and high reward investment opportunities over time. I run a Stock Market Research Platform where my job is to follow and cover the best businesses out there and to find the best times to invest in those.

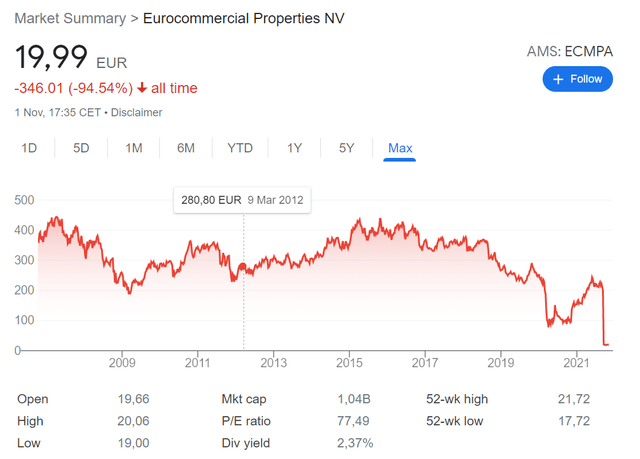

Eurocommercial Properties Stock Price Overview

There was a stock split recently with some depositary shares turned into normal shares and that is the reason for the stock drop below on the chart which is not real. Anyway, ECMPA stock didn’t do much over the last 15 years, actually the returns are negative as the stock split was 1:10. ECMPA stock is now at 50% of its price in 2007 and 2016. However, the financial engineering where they pay the dividend in share receipts complicates the issue further here.

Reason for drop: stock split in September 2021

But, investing is not about the past, it is about what will the business deliver in the future.

Eurocommercial Properties Stock Analysis – Business Overview

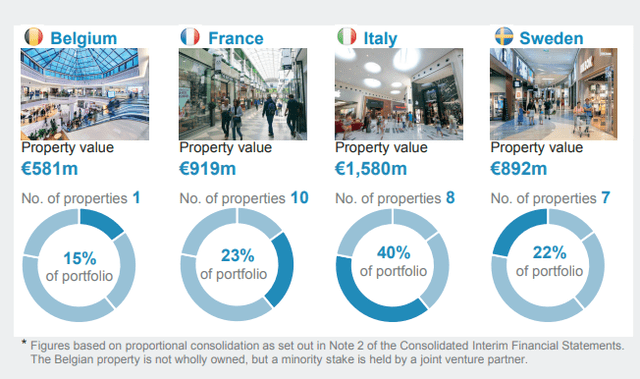

Eurocommercial Properties has 5 flagship shopping centres and 21 suburban ones.

Their net value estimation is at 3.9 billion EUR, but the market seems to disagree with that as the market capitalization is (49.4 million shares * 19.9 EUR) 1.04 billion EUR and thus much lower than the presented net value. Of course, the net value depends on a market appraisal made by the company while the market value depends on what the market thinks is a fair value. Appraisals assume everything will stay as is forever, while the market value also includes risks into the equation. As analysts, we have to see who is right.

On the business side, one can now elaborate on the long-term outlook for commercial properties, but that is impossible to know. Maybe we will stop shopping there, or new ones will be built and in 10 years these older ones will be refurbished or who knows what. I’ll stick here to an overview and try to give you an indication where to look if you are interested more in depth (hint: how will these properties look in 10 years – look around yourself, there are some where people still go, but there are also old centres that have been replaced by new ones).

Woluve shopping is in the suburbs of Brussel.

I don’t know whether there will be new projects or not in the future, bigger or if customers will see their preferences change. But those are factors to at least think of before investing.

Eurcommercial Properties Stock Analysis – Financials

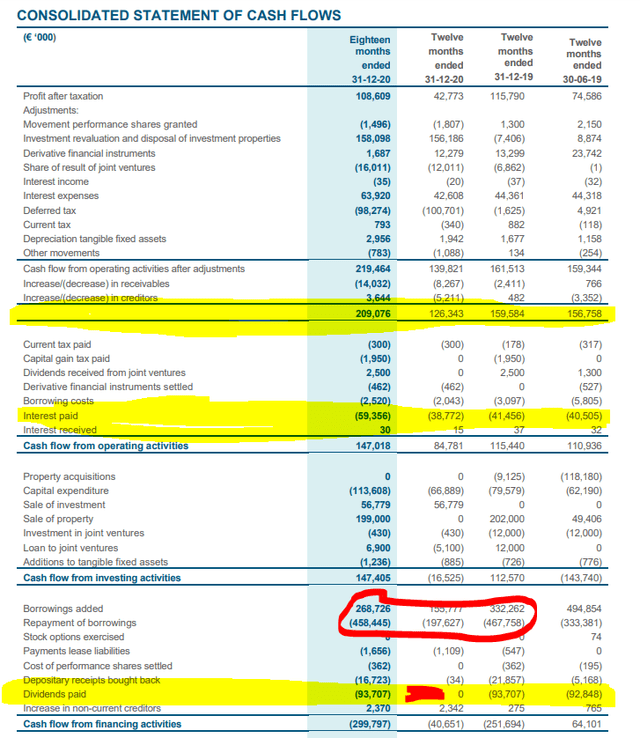

To go straight to the point, i.e. cash flows

The company makes around 160 million in operating cash flows from which we have to deduct approximately 45 million EUR in interest payments. That leaves around 115 million to work with. Of that, there is an approximate capital expenditure of around 60 million per year, even higher lately, plus, there was previously a dividend expenditure of 92 million, but that was alongside increasing debt which the company focused on lowering over the last year.

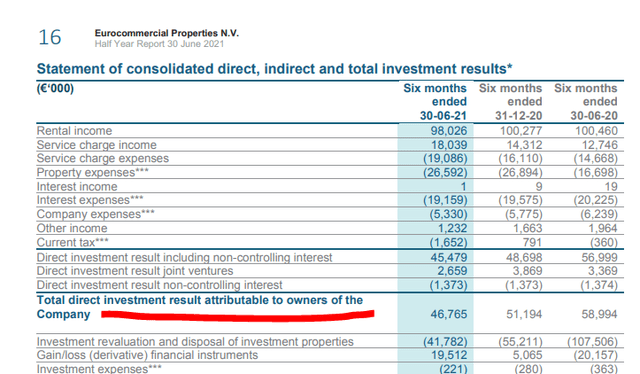

The below is for 6 months and thus we have to double it for yearly results.

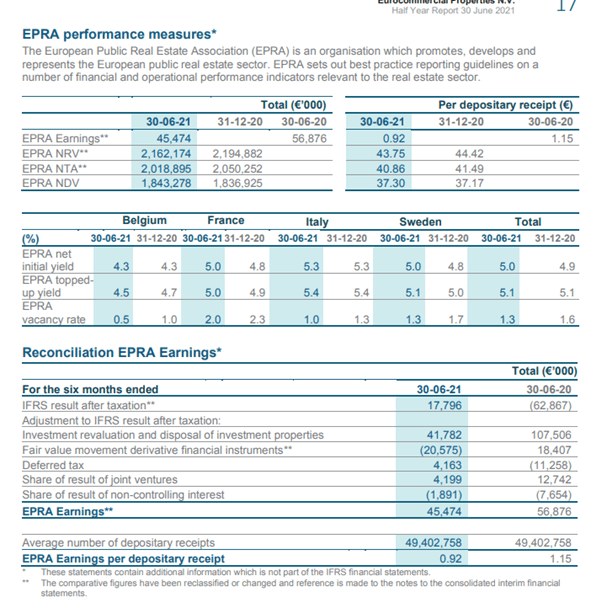

They make approximately 90 million per year in rents after other costs. Compared to 1 billion in market cap it looks like a yield of 9%. This is in line with their reported EPRA earnings.

Investing Perspective

If they make 90 million EUR on a 1 billion valuation, plus enjoy further real estate value appreciation alongside increasing rents, the investment thesis sound great. However, as I have analysed Aedifica Stock and CTPNV Stock, required yields by the market are in the high single digits which means there is definitely to think about risk. Possible risks are:

- A change in interest rates. Going from free money to mean historical interest rates would practically obliterate net income and the net asset value leaving you with a big fat zero as debt issues would repercussion across the whole European RE sector (think insurance, banks, RE etc.)

- Customer preferences. I hate shopping malls and buy most things online, but that is me.

- Demographics. Less and less people in Europe no matter how you turn it.

- Competition. One thing is see that as soon as one mall is cool, there quickly comes another that is newer and cooler – that is especially easy with these suburban malls that have no moat or location advantage.

The reward is tempting, especially from a dividend perspective, but there are also risks. I personally don’t like the RE kind of risks described above, I feel I can find things that offer such returns plus unlimited future growth. This doesn’t mean Eurocommercial Properties is a bad investment, it just doesn’t fit my risk and reward requirement.