April 1, 2025

Coal Stocks: A Deep Dive into the Risk and Reward of Investing in a Controversial Sector

The coal industry, often viewed as a relic of the past, continues to play a critical role in global energy... Continue reading

November 2, 2020

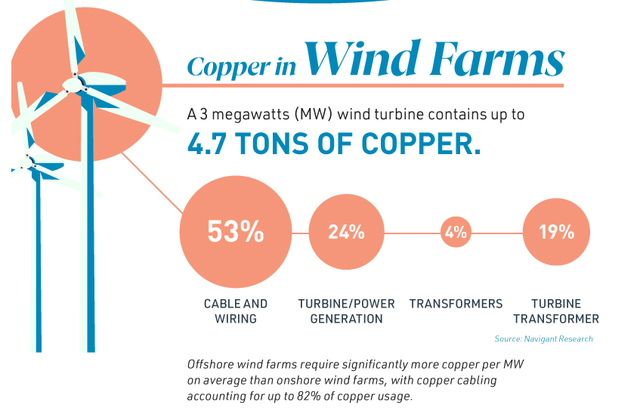

Copper Stocks Investment Thesis (Risk & Reward = When To Buy!)

Investing in copper Investing in copper is done through investing in copper mining stocks or a copper ETF. With copper... Continue reading

December 23, 2019

15 WASTE MANAGEMENT STOCKS LIST & SECTOR ANALYSIS – Detailed Analysis on 15 Stocks

Waste Management Stocks Global Sector Investment Analysis by Sven Carlin Ph.D. – Stock Market Research Platform. This report starts with... Continue reading

October 8, 2019

Shipping Investors Have Capitulated – Time to Invest – SEA ETF

Contents Shipping’s terrible past investment performance – is it time to invest now? Shipping investing thesis – without shipping there... Continue reading

October 6, 2019

XOM Stock Analysis – The End of BIG OIL

The biggest risk when it comes to investing in XOM is that the management never stops believing in the everlasting... Continue reading

March 6, 2019

Food Stocks Sector Analysis And Investment Strategy

Do food stocks offer a margin of safety? Before discussing food stocks as investing opportunities, let me just tell you... Continue reading

January 29, 2019

Zinc Stocks List and Sector Analysis

Summary Zinc and copper are in a similar situation, low commodity prices over the last few years have put off... Continue reading

January 11, 2019

Altria Stock Analysis + BTI and PMI + Tobacco Industry

Contents Altria stock analysis and fundamentals. Reason for stock price decline. Tobacco business overview Discounted cash flows for MO BTI... Continue reading

January 6, 2019

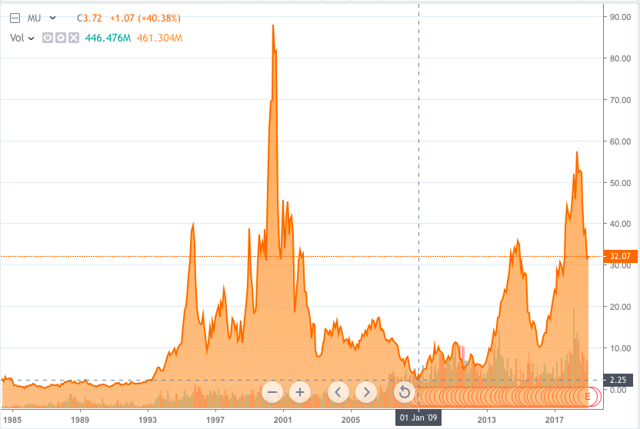

Micron stock analysis

To invest in Micron, one has to understand the industry's cycle. A PE ratio of 2.5, doesn't mean much as... Continue reading

January 3, 2019

Investing In Uranium – Bullish And Bearish Thesis On 5 Uranium Stocks

The bullish thesis for uranium is strong; growing demand coming from Japanese restarts and developing Asia, alongside production cuts. However,... Continue reading