October 14, 2020

When To Sell A Stock – 7 Strategies (20% Portfolio Stock Sale Practical Example)

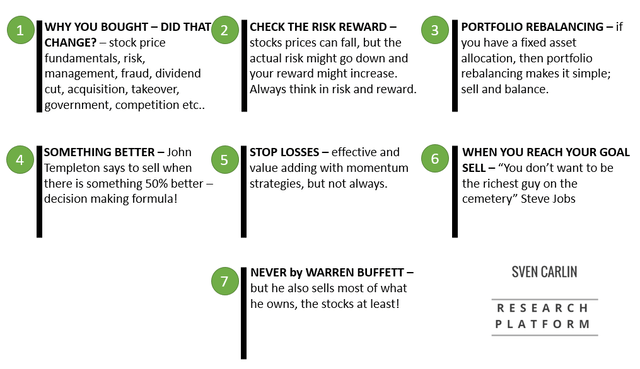

When to sell a stock – the hardest part of investing I’ve recently sold a stock that made 20% of... Continue reading

May 15, 2019

Trying to Explain Nassim Taleb’s Views on the Economy and Markets

Nassim Taleb just had an interview on Bloomberg discussing the latest topics in finance: Modern Monetary Policy – Monetary Policy... Continue reading

December 20, 2018

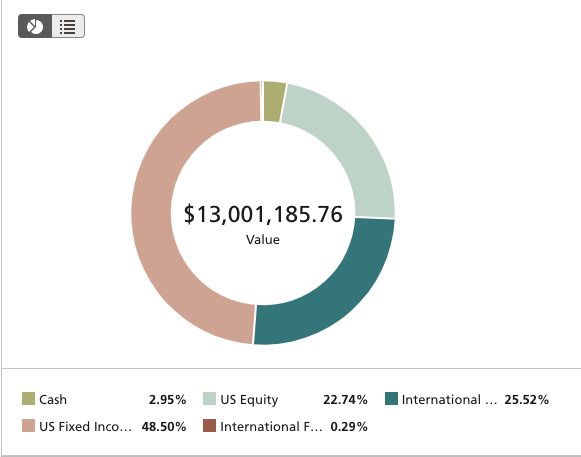

$13 Million-Dollar Investment Bank Managed Stock Market And Bond Portfolio Review

A month or something ago, I was contacted by an investor that had just set up a portfolio with an... Continue reading

November 14, 2018

How to invest in businesses with dr. Per Jenster

I recently had the privilege to interview dr. Per Jenster. He is a Fullbright scolar, author of many books, former... Continue reading

November 6, 2018

Nassim Taleb is warnings us – situation worse than in 2007

The US government has $21 trillion of debt, but few know and think about the $49 trillion in hidden debt.... Continue reading

September 26, 2018

Ray Dalio – Big Debt Crises – Summary (video/audio)

Ray Dalio, the legendary hedge fund manager is out with a new book. After the success he achieved with his... Continue reading

July 26, 2018

Latest Canada Pension Fund Investing Strategy

This pension fund investing strategy is for a Canadian customer that asked for my help when it comes to her... Continue reading

July 24, 2018

Perfect Stock Market Portfolio

How to build a perfect portfolio How to manage a stock portfolio It is all about portfolio risk reward STOCK... Continue reading