Atrium European Real Estate Stock Analysis – Poland REIT With 6% Dividend

This Atrium European Real Estate stock analysis (AMS: ATRS stock, VIE:ATRS) is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As.

AMS: ATRS Stock Price Overview

Whenever I look at European REITs, they are always in the process of asset rotation. The same is with Atrium European Real Estate, in 2015 they had many smaller properties, now they have only bigger, their initial focus was on commercial now they are targeting residential. It seems to me that these REITs never figure it out and just chase trends. At least the management is busy and perhaps it is just to justify their salaries and bonuses.

They must rotate because the market doesn’t like what they have been doing and the stock has been in a downward trend since the IPO, while the S&P 500 is up 4 times.

Let’s see whether there is something more to Atrium that could make it an interesting investment proposition.

Atrium European Real Estate Stock Analysis – Overview

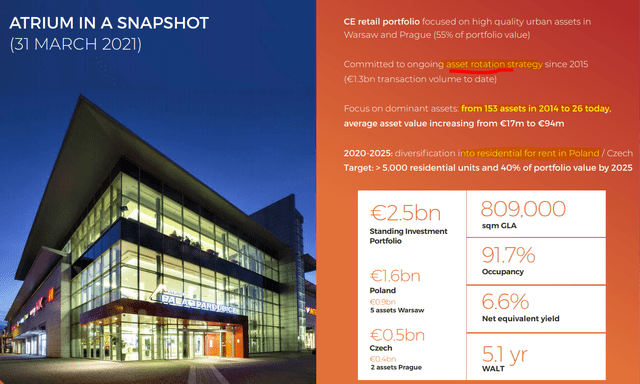

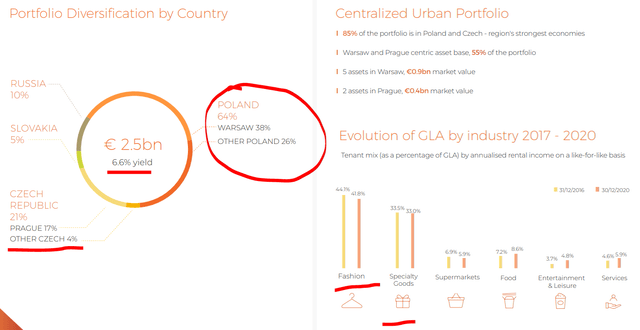

Atrium’s focus is Poland where 64% of the assets are and given their residential strategy, the exposure is likely to increase up to 2025.

Atrium’s current holdings are shopping centres. Now, I’ve looked at a few of such REITs as there are more in Europe and if I just take a common-sense approach and look at what is going on in Eastern Europe; as one shopping centre is finished there is a new being built. Add on top the fast switch to online deliveries (I am ordering everything online as it is cheaper for me to pay 3 EUR for deliver than to sit in a car and drive 30 minutes to the nearest shopping centre even if they are now building one in my town too).

I don’t think these businesses have any kind of moat and therefore I find them very risky to invest in because if you are profitable, you will have a new centre next to you in a few years. Plus, population trends are negative in Europe. This is probably also the reason why Atrium is rotating towards residential properties.

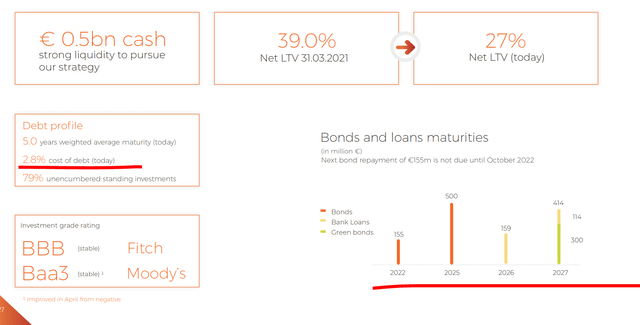

On top of everything there is always interest rate risk, regulatory risk etc. If interest rates go up and they are not allowed to increase rents or tenants don’t pay, REITS will be in a bad situation. Atrium’s average debt cost is just 2.8% which is ridiculously low for Eastern Europe.

As there is risk, if you wish to take it, you need to be paid very well. So, let’s take a look at Atrium’s financials.

Atrium stock analysis – fundamentals

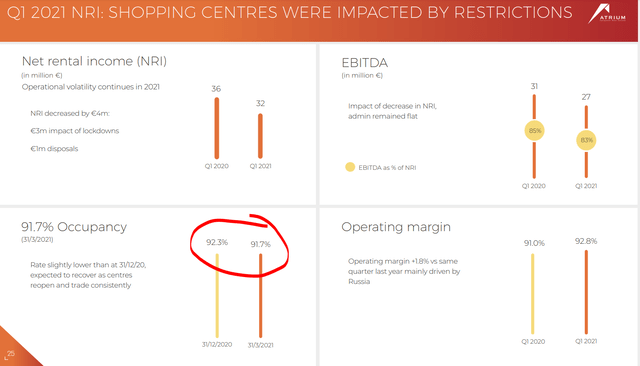

Even before COVID occupancy wasn’t stellar and that also explains the higher yield you get in Poland.

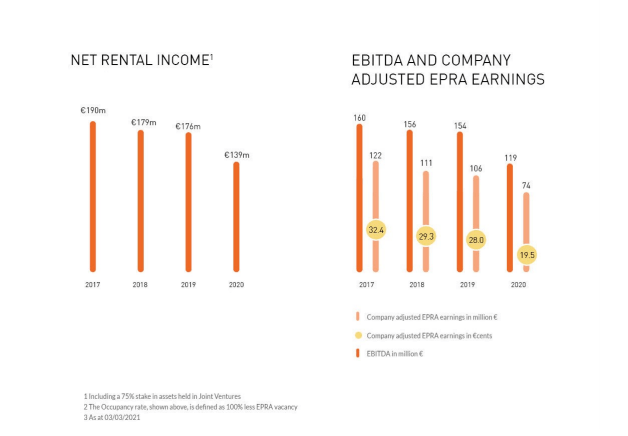

Net rental income is around 35 million EUR in a normal quarter. There is no AFFO or EPRA in their presentation so I have to check their financial statements but it is strange that they don’t talk about dividends or AFFO (adjusted funds from operations) in their presentation, that is the key with REITs. Ok, in the Annual Report we find EPRA and they don’t talk about it because EPRA has been going down.

That is 19.5 cents per share for a 6% yield.

Atrium Stock Investment Thesis

When it comes to European REIT stocks or other REIT stocks, it all boils down to what you wish to own and what is the yield there. Atrium is focused on Poland and thus the yield is around 6% which is on the lower side for commercial properties in Eastern Europe.

Aedifica is a REIT with a 2.5% dividend yield but in a very positive investing sector, the elderly care sector. Athos Immobilien owns properties in Austria and offers an even lower yield of just 1.6% but likely more safety, no currency risk if you key currency is EURO etc. CA Immo is a bit more leveraged as is Immofinanz. If you go global, you can find also very interesting yields with Store Capital or SmartCentres in Canada. Here is a video touching on them. Store Capital REIT Stock + Douglas Emmett & Smartcentres

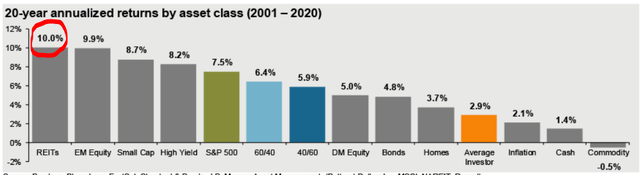

I personally am not looking deeply at REITs now because everything is so good for them in the form of low interest rates and an abundance of liquidity. This leads to many investments and one day there will definitely be oversupply. Declining interest rates made REITs the best performing asset class over the last 20 years, but I don’t think we can expect the same over the next 20 years, especially if the interest rates trend changes.

Anyway, this is just a personal perspective and the key is that you see how REITs fit you, especially how the bottom up analysis of an individual REIT strategy fits you, the dividends are there and definitely better than in many other sectors. I simply think that I can find better than commercial or residential properties in Poland.

If you wist to get a bi-weekly summary of my stock analyses, please subscribe to my newsletter.

About the author: Sven Carlin Ph.D. is a dedicated investing educator and stock market researcher focused on finding investment opportunities with a value investing perspective. His research is summarized on the Sven Carlin Research Platform where he covers many stocks and shows his portfolios. The educational part is shared on YouTube and the Free Stock Market Investing Course.