January 24, 2025

How To Calculate Intrinsic Value

(this article is part of the free value investing course by Sven Carlin, check it out) In this crazy world... Continue reading

April 13, 2021

Li Lu Himalaya Capital 2021 Interview – Value Investing In Asia

Li Lu, Charlie Munger’s famous Chinese right hand and manager of Himalaya Capital, recently gave an interview for the Columbia... Continue reading

October 14, 2020

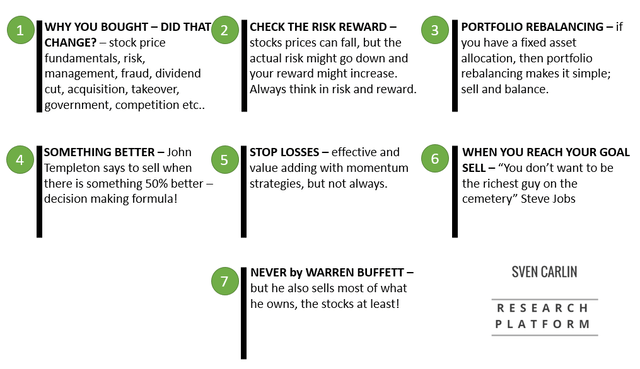

When To Sell A Stock – 7 Strategies (20% Portfolio Stock Sale Practical Example)

When to sell a stock – the hardest part of investing I’ve recently sold a stock that made 20% of... Continue reading

May 16, 2020

Stocks Crash 70% And 76% Will Underperform – Can You Handle That?

Stocks crash and stock markets too Before investing, you must know that stocks can crash 70% anytime and 50% of... Continue reading

February 19, 2020

When To Buy Stocks And When To Sell Stocks – The Six Stocks Categories Tool by Peter Lynch

Six Categories of Stocks – When to buy stocks, when to sell stocks! From One Up On Wall Street by... Continue reading

February 3, 2020

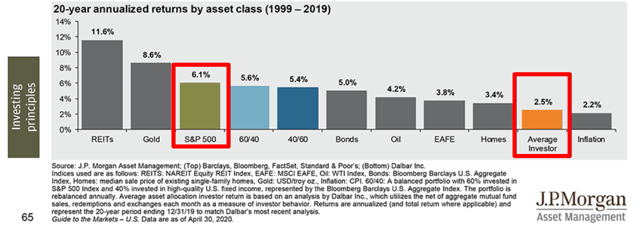

Index Fund Investing Explained with a 150 year Return Analysis of the S&P 500

Index fund investing I recently received an email from Peter asking about investing in index funds. He likes the idea... Continue reading

November 1, 2019

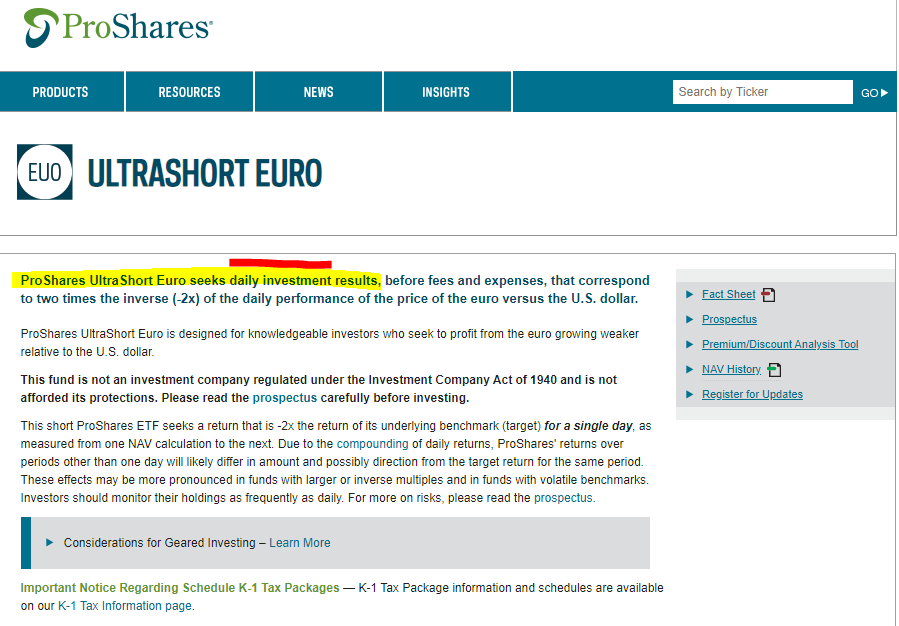

Currency Hedging – Why I Am Not Doing It

Currency Hedging? As I am an international investor, I often get the question on how to hedge for currencies. Many... Continue reading

September 15, 2019

INDEX FUNDS Investing – NEXT Market CRASH WILL BE UGLY

Mortgage crisis Dr. Burry - Compares Index funds to subprime bubble! Dr. Michael Burry, famous for predicting the subprime mortgage... Continue reading

June 27, 2019

How To Invest With Coming Debt Crisis – Don’t Be The Turkey

Three extremely important pieces of information released over the last weeks for investors are: The increase in US budged spending... Continue reading

June 18, 2019

How To Invest $1000 – 6 Rules For Investing Your First 1000 Dollars

Before discussing the 7 rules to follow when investing $1000 and an example of where I am investing my $1000s,... Continue reading