January 31, 2025

JDE Peets: A Comprehensive Analysis of the World’s Leading Coffee and Tea Company

JDE HistoryBusiness OverviewLeadership and ManagementFinancial PerformanceIntrinsic Value and ValuationMargin of SafetyDividend and Capital AllocationRisks and OpportunitiesConclusion Check out the full... Continue reading

November 4, 2021

Fagron Stock Analysis (Balance Sheet Risks)

This Fagron stock analysis (AMS: FAGR) is part of my full analysis of every stock traded on the Amsterdam Stock Exchange.... Continue reading

November 3, 2021

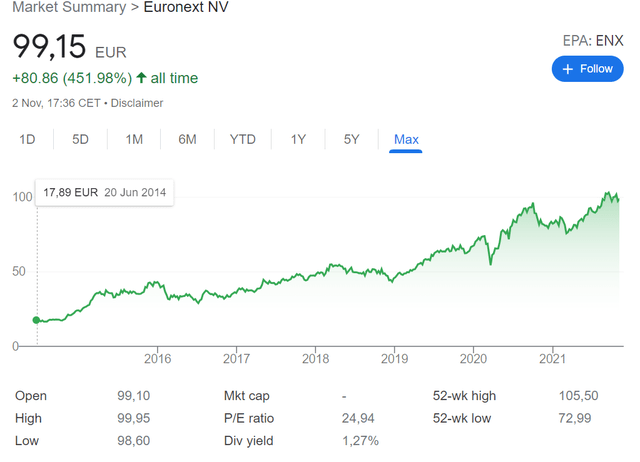

Euronext Stock Analysis – Too Expensive Even if Good Business

Euronext stock is very interesting because it represents a stock exchange. Stock exchanges usually have moats as the companies listed... Continue reading

June 11, 2021

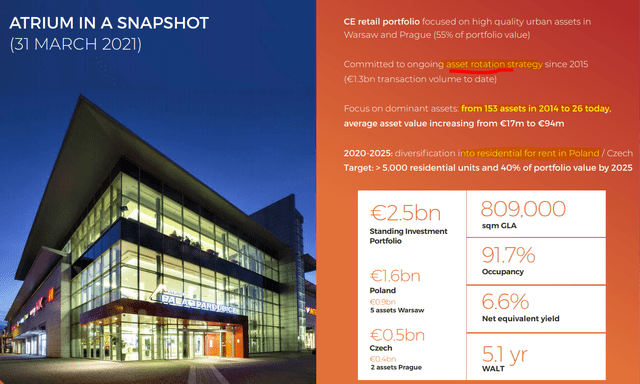

Atrium European Real Estate Stock Analysis – Poland REIT With 6% Dividend

This Atrium European Real Estate stock analysis (AMS: ATRS stock, VIE:ATRS) is part of my full analysis of every stock traded... Continue reading

June 10, 2021

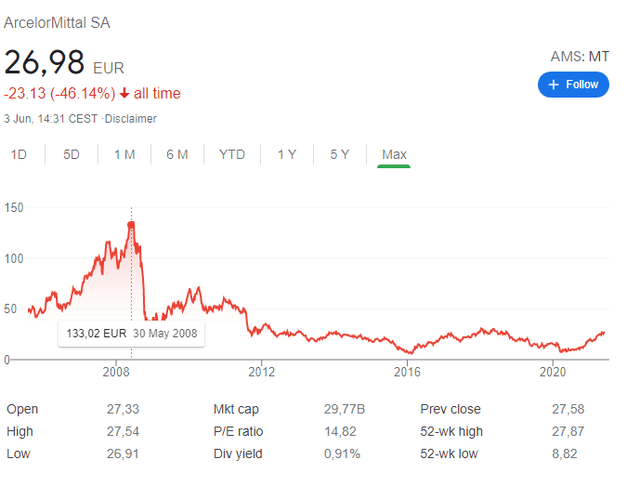

ArcelorMittal Stock Analysis – Business Is Improving, Cash Flows Up

This ArcelorMittal stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal... Continue reading

May 20, 2021

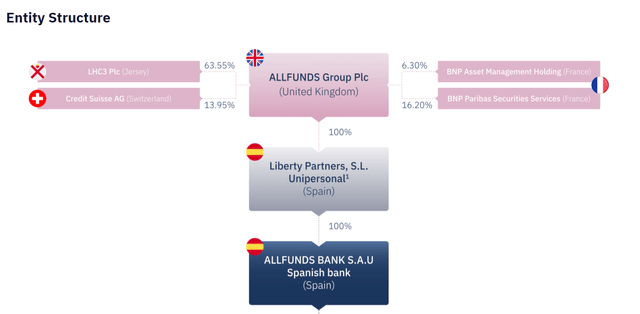

Allfunds Group Stock Analysis – AMS: ALLFG – ! AVOID !

Allfunds Group stock is a very recent IPO. It is a Spanish company, headquartered in the UK that has listed... Continue reading

May 12, 2021

Akzo Nobel Stock Analysis – Stock Price Going Up Thanks To Buybacks

This Akzo Nobel stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My... Continue reading

May 11, 2021

Aedifica Stock Analysis – ‘We Are Getting Older’ REIT Investment

This Aedifica stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My... Continue reading

May 7, 2021

Accsys Technologies PLC Stock Analysis – 5x Growth Ahead

Accsys Technologies PLC Stock Analysis – LON: AXS AMS: AXS This Accsys Technologies PLC stock analysis is part of my... Continue reading

Accell Stock Analysis – Good Business But Difficult Sector

This Accell stock analysis is part of my full analysis of the stocks traded on the Amsterdam stock exchange. I... Continue reading