January 22, 2019

Afi Development, LSR Group, Etalon Stock Analysis – Russian Real Estate Developers

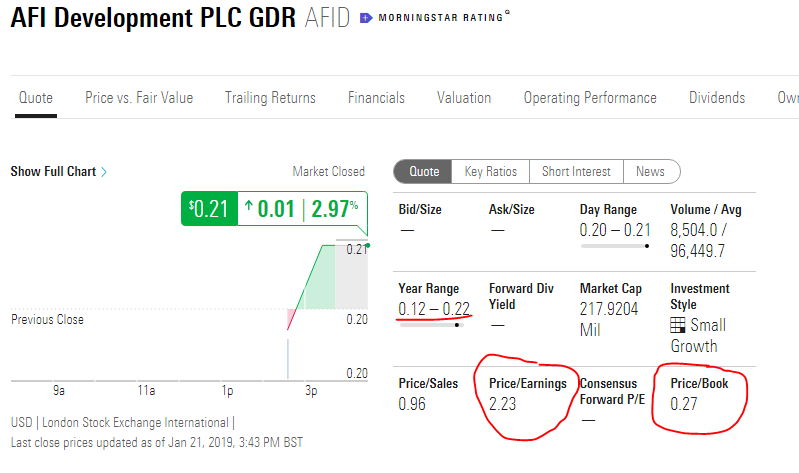

Russian Real Estate Developers Stocks – AFI Development and LSR Group A few months ago, I looked at Chinese real... Continue reading

January 6, 2019

Gazprom stock analysis

Gazprom is one of the most undervalued stocks in the world from a cash flow and book value point of... Continue reading