NorthWest Healthcare Properties REIT Stock Analysis – 10% Returns Possible

I’ve looked again at US healthcare REITs (Real Estate Investment Trusts) and other REITs and I sense high risk. There is simply too much money chasing growth and investment opportunities, that I don’t feel like investing there. Plus, yields are globally the lowest.

Therefore, I’ve been looking at Canadian REITs and found some interesting ones of which one is NorthWest Healthcare Properties (OTC: NWHUF, TSE: NWH.UN), a globally diversified healthcare REIT offering a dividend yield of 6.69%.

NorthWest Healthcare Properties REIT company overview

Source: Northwest Investor Relations

The company owns medical office buildings and hospitals in Canada, Brazil, Germany and Australia.

They have an interesting investment strategy with high occupancy, long-term lease contracts, indexed rents to inflation and a strong development pipeline.

Source: Northwest Investor Relations

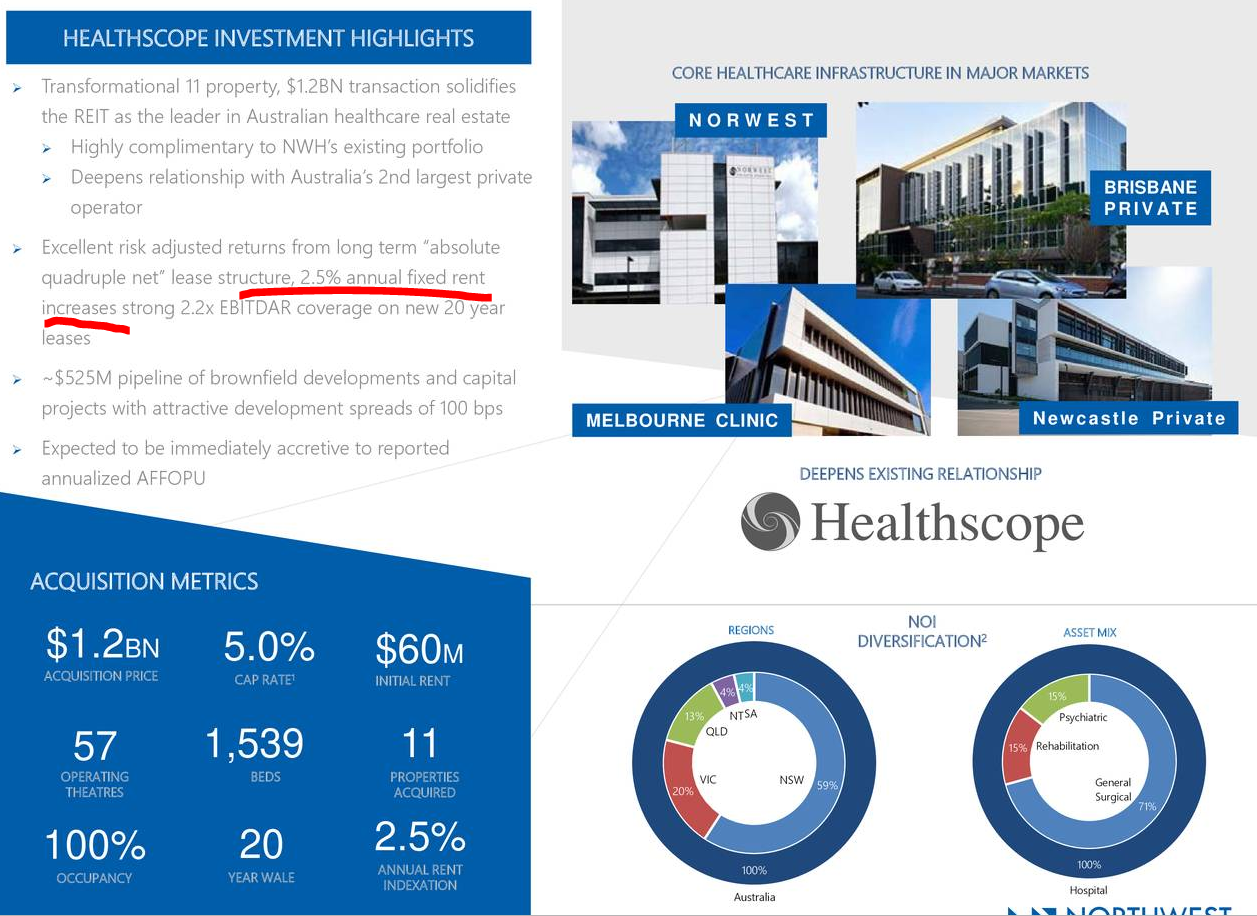

They recently made an acquisition in Australia that describes well what they do.

Source: Northwest Investor Relations

First, they take advantage of the low interest rates within financial markets. This allows for better investing spreads, especially in Australia and Germany. Second, they buy assets where you can increase rents, 2.5% per year in the above case. Keep in mind that the debt doesn’t increase, this increases profits. Thirdly, if interest rates go down, in general or just for them, they’ll make even more money. If interest rates go up, they have most of their income indexed to inflation.

Current market circumstances, with low interest rates, allow them to make acquisitions that have positive spreads and are immediately accretive to funds from operations.

Source: Northwest Investor Relations

An FFO improvement of $0.11 per share will probably lead to FFO growth of 10%, that is significant and might lead to share price appreciation next year. More deals like this and this company could easily continue to grow. Business growth will equal stock price growth.

They don’t acquire with total ownership but always build a JV. This allows for better financing deals and higher margins.

Source: Northwest Investor Relations

By continuing what they have been doing, we could expect more growth.

Source: Northwest Investor Relations

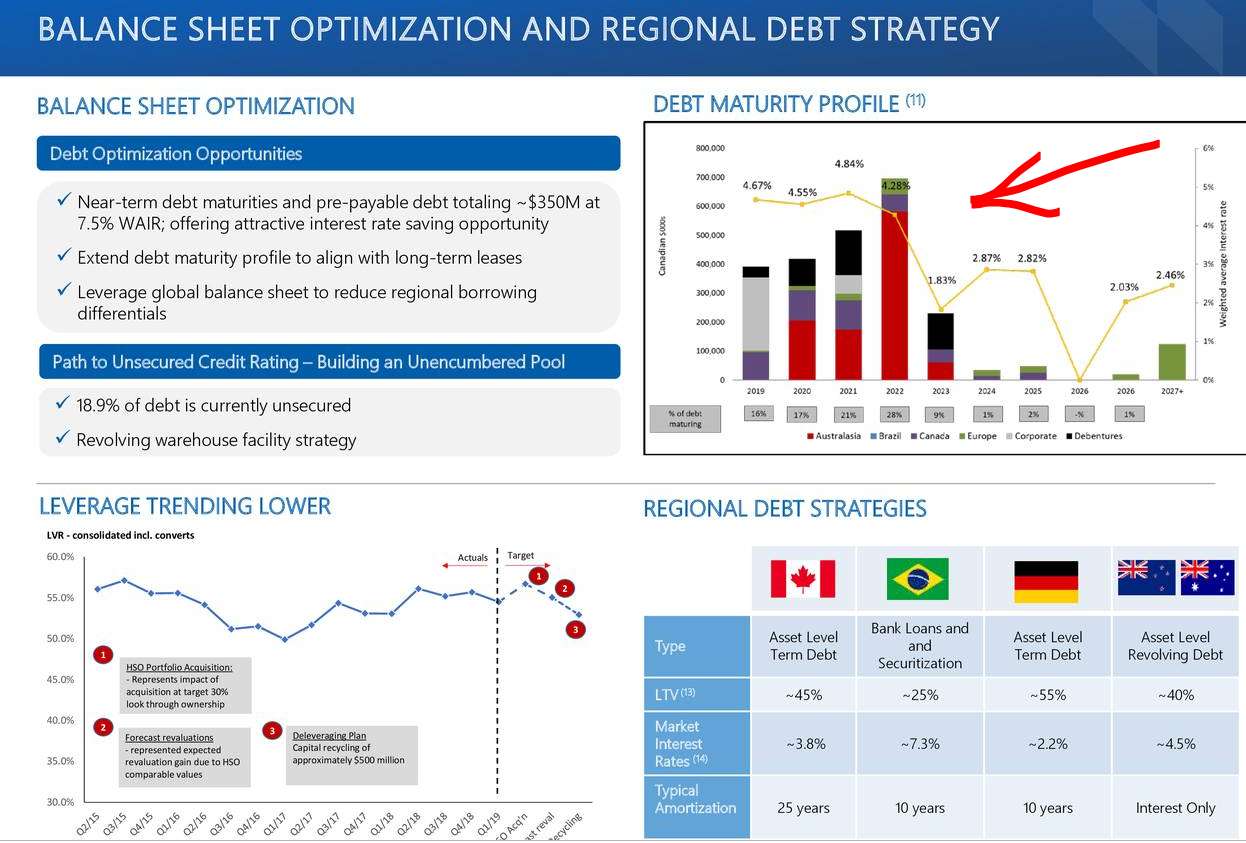

However, acquisitions and debt also mean risk.

NorthWest Investing Risk

The debt looks good but it has short term maturities. This is good in a declining interest rate environment but not so good in a rising rate environment.

Source: Northwest Investor Relations

But, perhaps we are done with rate hikes globally so this REIT might do good. In any case, hospitals should be recession proof so not much to worry there.

Another risk might be Brazil, with the largest tenant being from there, but it looks like a well-diversified REIT exposed to global aging trends. As for currencies, you never know what will happen there so again, better to be diversified.

Conclusion on NorthWest Healthcare REIT

The targets are simple and standard. Slow growth from higher rents and acquisitions while improving the capital structure.

Source: Northwest Investor Relations

From an investing perspective, given the nature of the assets I don’t think there is much risk for dividend cuts, so investors should be sleeping well with the 6.69% yield. If they grow FFO as promised, the yield might go up, up and up over the years. Therefore, with a growth rate of 5% and a yield of 6.69%, the long-term return from this could get to 12% and beyond. Not bad! However, there will always be ups and down, various issues, delays etc. So, one might add 3% average growth and get a 10% long-term return. Still not bad at all.

If you want to get an even better return, you should wait for a time where the growth isn’t priced in, but just the dividend.

It doesn’t yet hit my 15% return after taxes, so I’ll wait and watch it. Perhaps one day over the next 10 years it will hit my mark.

All in all, one of the best REITs out there. Some are afraid of global diversification; it makes me sleep well.

Note: see how you would be taxed on the dividend if you fancy owning a REIT like this.

I’ve listened to the conference call, and nothing strange to report. The CEO is the majority owner and they manage this as their own business. Interesting to follow.