CA Immo Stock Analysis – Constant revaluations create houses of cards

This CA Immo stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian Stock Exchange. Austria is one of the cheapest stock markets globally at the moment so please check the Austria Stock List for interesting investments.

Here is the video on real estate stocks investing using the CA Immo stock analysis as example. Written analysis continues below the video.

CA Immo Stock Analysis

Give me a second, I’ll just give 20,000 EUR to my father. Let me call him and then we can continue with the CA Immo Stock Analysis. This is the transcript:

Sven: Hi Dad!

Dad: Hi!

Sven: Do you remember the 6,000 square meters of wood land you own in the middle of nowhere that you inherited?

Dad: Yes, what about it?

Sven: Well, I know you value it at 1 EUR per square meter and think the value could be 6,000 EUR, but I think the value could be 6 EUR per square meter and the total value 36,000 EUR!

Dad: That is wonderful, thanks!

Sven: Your welcome, I just made you 30,000!

Dad: Thanks son, you are great!

Sven: Your welcome!

Dad: Now son, can we sell it then for that price?

…… (no connection)

……

……

Why this discussion at a start of the CA Immo stock analysis? Well, this is exactly how CA Immo creates value. Here is my analysis and you can then decide what to focus on and what to invest in; property revaluations or cash flows – it makes a huge difference!

Here is the video discussion with higher focus on general investing in REITs while using the CA Immo Stock Example, article continues below.

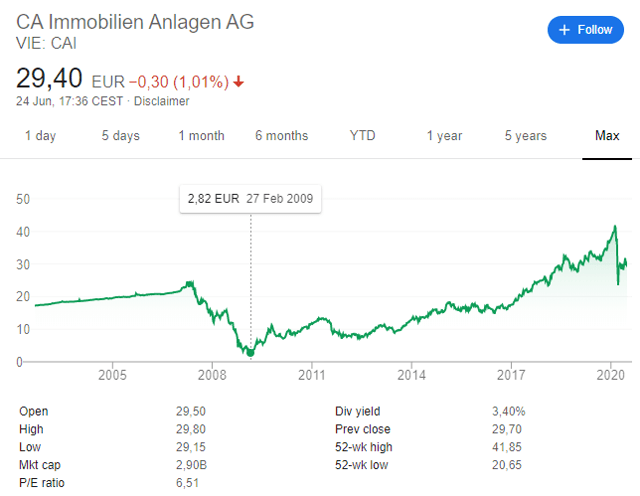

CA Immo Stock Quote – CA Immobilien Anlagen AG

Vienna stock quote: CAI

OTC: CAIAF (low volume)

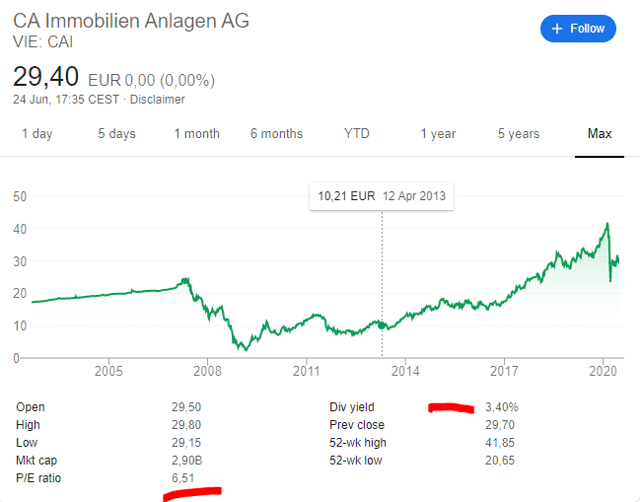

The stock has fallen recently but is still a 10 bagger from 2009, plus the 2007 – 2009 situation was ugly. So, we have a few things to watch out for and see whether such a bad period can happen again. The dividend is fair at 3.4%.

This CA Immo stock analysis has a short business overview, a valuation, a fundamental analysis and investment thesis conclusion with the key factors to watch out for when it comes to investing in CA Immo stock.

CA Immo Stock Analysis – Business Overview

CA Immo is a specialist in office properties in Central European capitals.

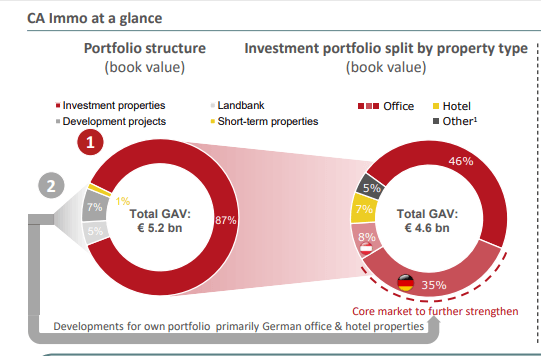

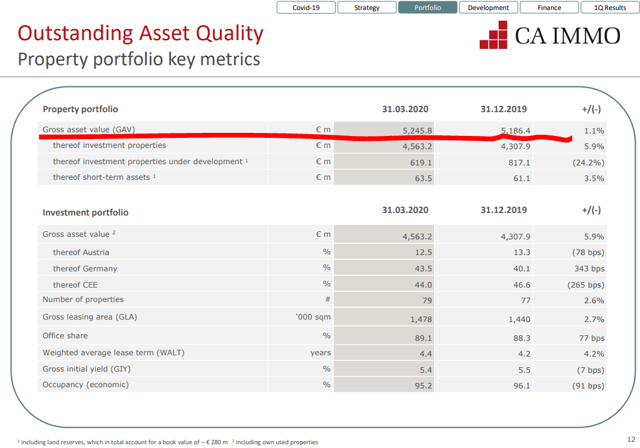

CA Immo is a real estate company with its headquarters in Vienna and branch offices in seven countries of Central Europe. Its core business involves leasing, managing and developing high-quality office buildings. The company covers the entire value chain in the field of commercial real estate, based on a high degree of in-house construction expertise. Founded in 1987, CA Immo controls property assets of around € 5.2 bn in Germany, Austria and Eastern Europe.

It is focused on commercial properties; it has 4 development projects and some landbank. 88% of the properties are offices.

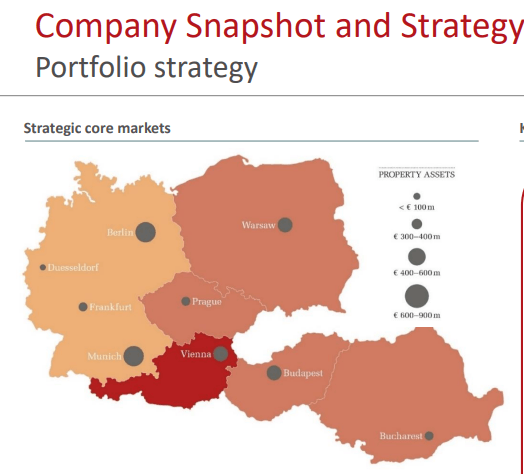

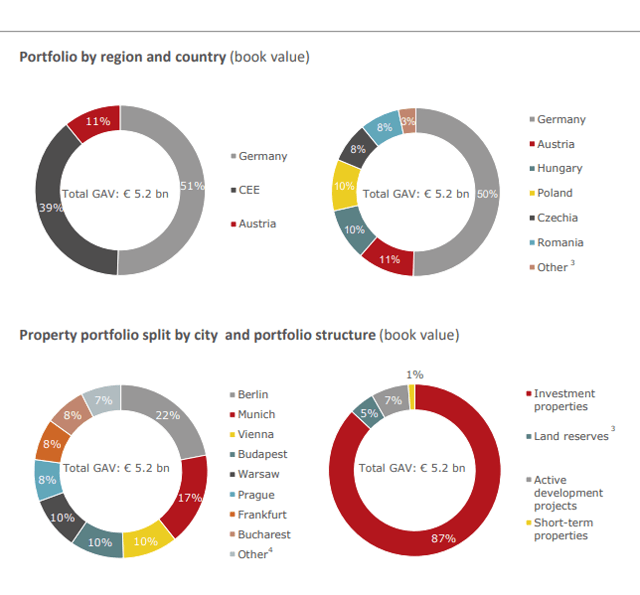

Their largest single market is Germany with 51% where the percentage is expected to grow when the projects are completed as all the new projects are in Germany.

The highest value of the properties is in Berlin, followed by Munich, Vienna, Budapest, Warsaw etc.

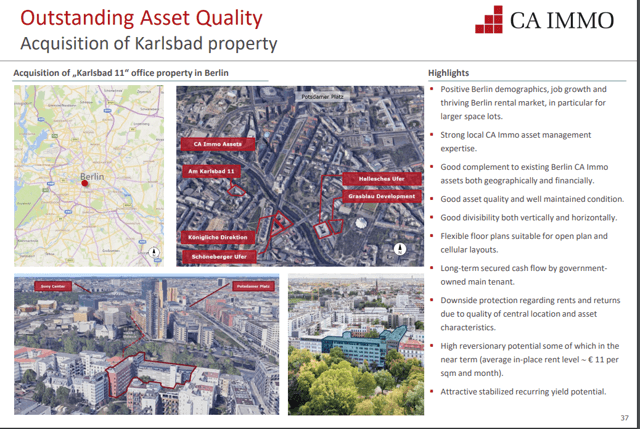

In short, the company focuses on central locations withing the above-mentioned cities offering commercial space. Like in the example below for Berlin.

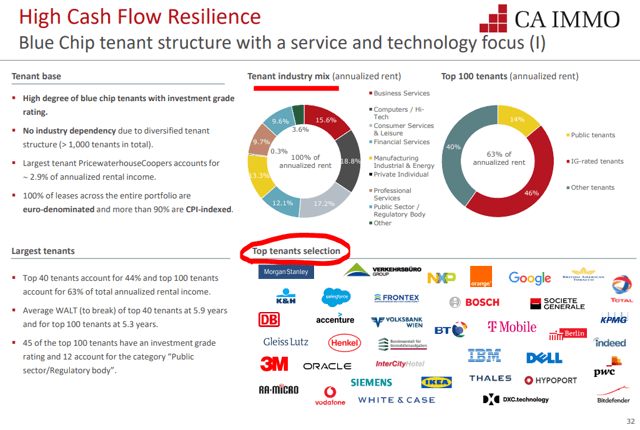

The tenants are well diversified and many of them of top quality that you will likely recognize.

CA Immo Stock Analysis – Valuation

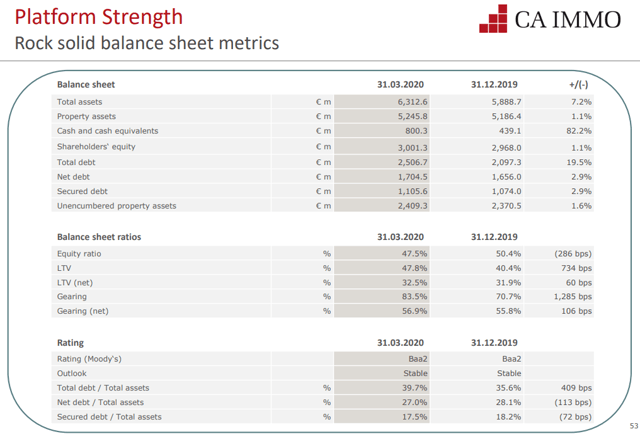

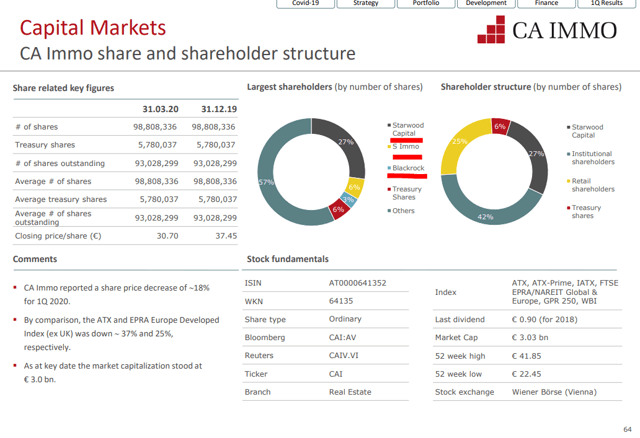

There are two ways to value a real estate business. One is the way most do it by looking at the value of the assets. In the case of CA Immo, the gross asset value is 5.24 billion EUR.

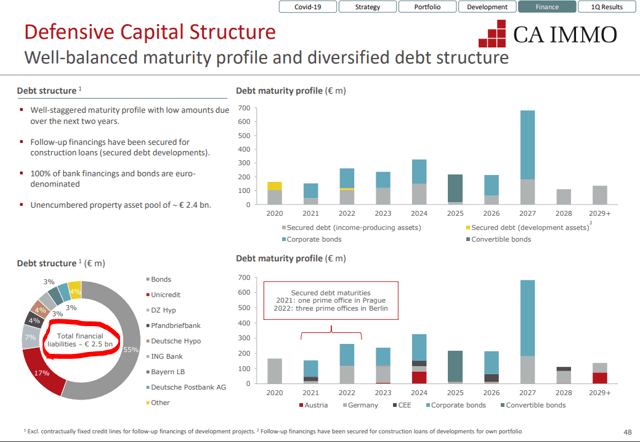

You then deduct the liabilities of 2.5 billion EUR and you get to a net asset value of 2.7 billion EUR. When we add the cash and deduct other liabilities, the shareholder equity is at 3 billion EUR.

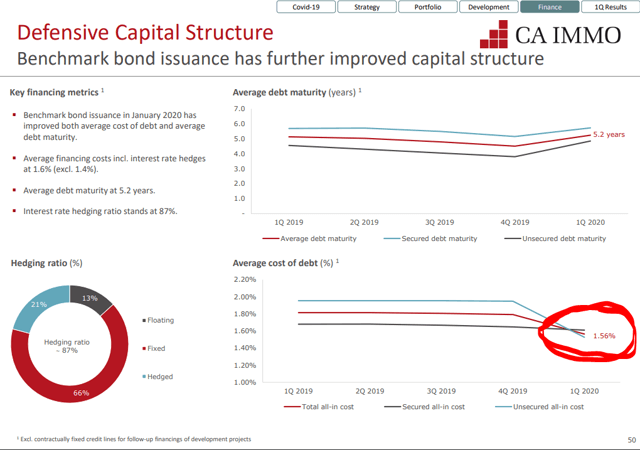

Their cost of debt is ridiculously cheap at 1.56%, which makes it worthwhile to invest into properties for a yield of just 3.9%. This is also the reason why you as a European will have to come up with a lot of money to buy property yourself. I guess the situation is similar in most developed countries with low interest rates.

If they can borrow at 1.56% and rent out at 4%, that is a huge spread and that is what they are investing in.

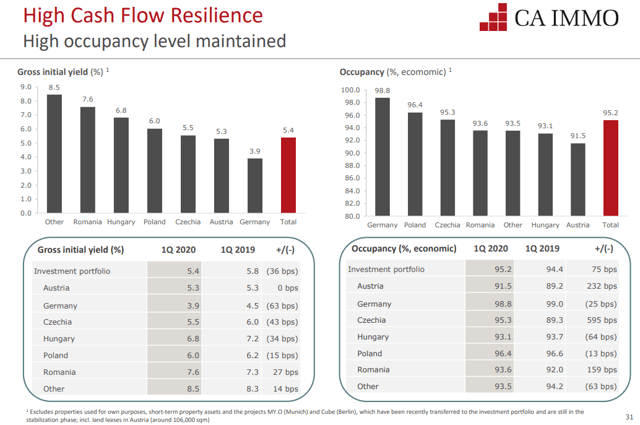

Real estate valuations are made on what is the accepted or required yield on the asset. For example, in Germany a yield on the value of 3.9% is considered good, while in Romania a 7.6% yield is what CA Immo gets. Consequently, property valuations are different and depend on the required yield.

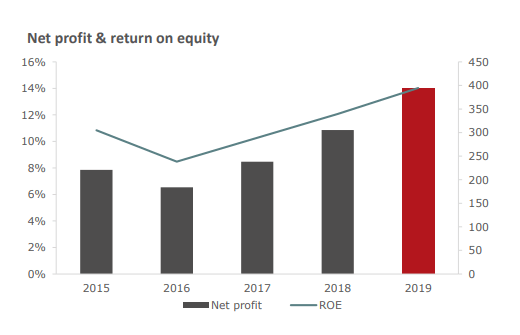

The large spread between the cost of money and rent yields leads to high return on equity for the company.

As value investors, we have to focus on cash flows streams. Cash flow streams that we can compare to other investing opportunities. Real estate values depend firstly on interest rates and as nobody can predict that, it is more an opinion, like accounting. What matters are the cash flows you will get and whether the business fits your investing requirement.

The management is so focused on property values, but we can focus on the cash flows that are relatively stable.

Hoping that all the companies renew their leases. In difficult economic times, occupancy rates will be lower as some tenants will go bankrupt. That is something that is inevitable at some point in time. Perhaps not just as now given that there is so much free money which allows even unprofitable companies to survive for longer and the market mechanics are completely distorted, but one day it will happen and I don’t want to be a CA Immo shareholder on that day. A think to carefully watch if you are thinking or invested in CA Immo stock.

Plus, when the situation gets though, they need to fairly revalue the property values as they have been doing all these years. The current shareholder value is 3 billion EUR, but most of that comes from revaluation.

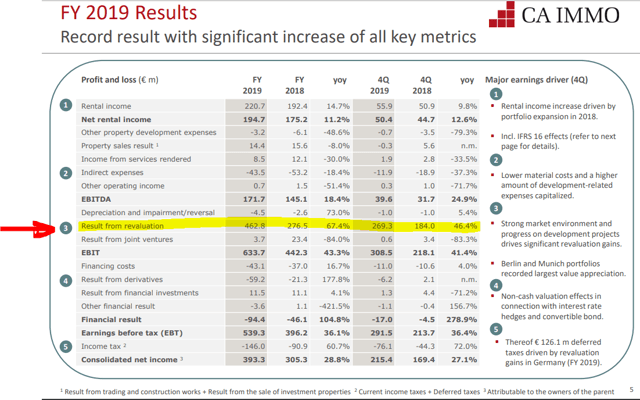

Just in 2019, they increased the value of their assets by 462 million EUR, 226 million EUR in 2018. Revaluations are a non-taxable accounting exercise that increased net profits and that is why you see the low PE ratio next to CA Immo stock.

But, don’t get confused. In case of trouble, these revaluations might be reversed, or kept unrealistically at the same level and suddenly all the metrics would look much different. As investors, there is one metric that is best – cash flow. When it comes to real estate investing it is called FFO – Funds from operations.

CA Immo stock analysis – Cash flow or FFO

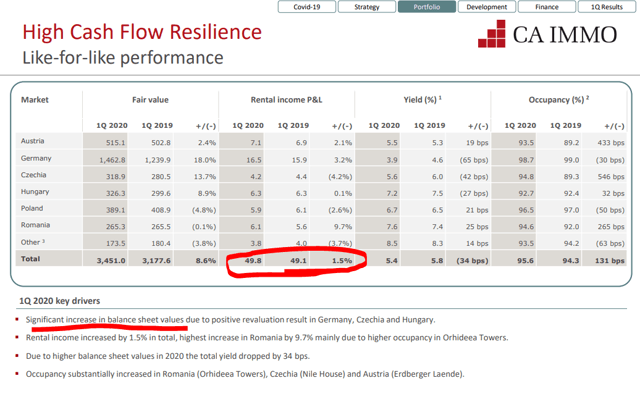

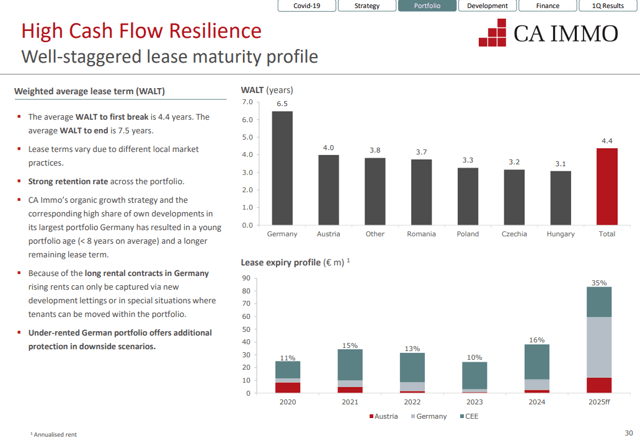

The average leasing term is 4.4 years which gives you some certainty, but you also depend on the economic situation.

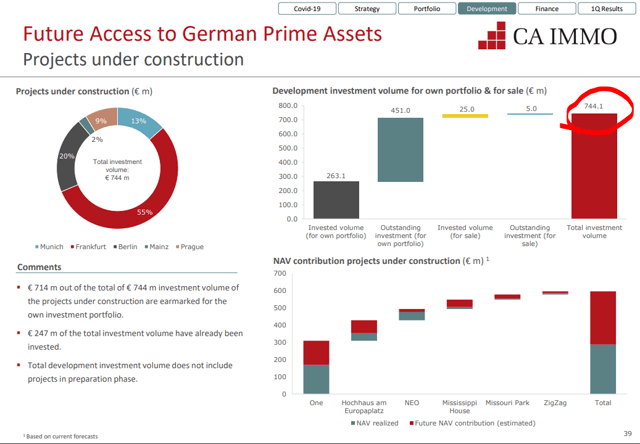

They are planning to invest 744 million that should add another 45 million to the yearly rent income if all is occupied at a 6% yield on cost.

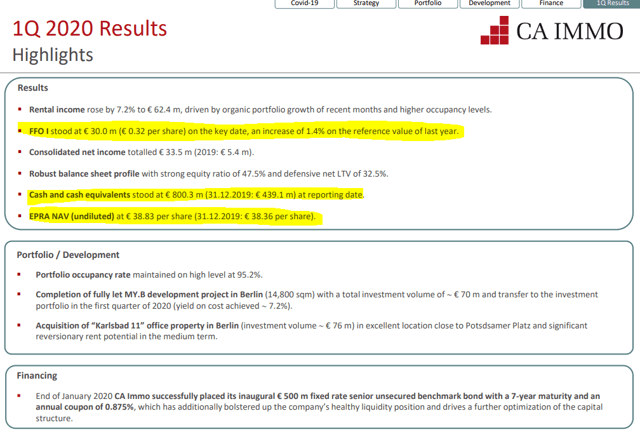

All in all, funds from operations were 30 million EUR in Q1 2020, which gives a hope for 120 million per year.

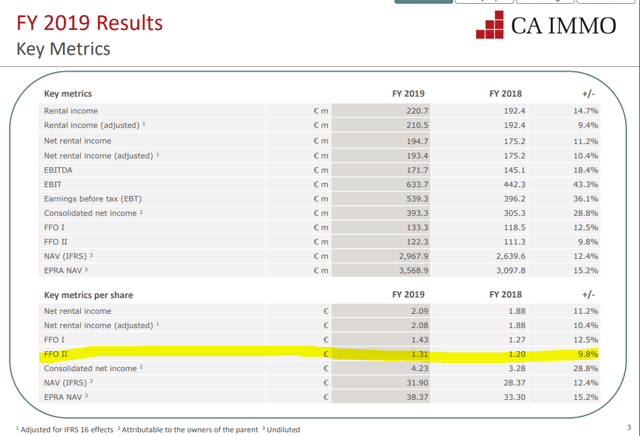

On a yearly basis, the adjusted FFO is around 1.31 EUR per share and that is the real return you as an investor should focus on.

With a bit of growth, we could add 30 million from the new projects and hoping on some rent increases here and there, we can get to a growth rate of 3% per years in a good environment.

However, even if the management says they haven’t been impacted by COVID that much, we will see the real impact over the next years for commercial properties.

All in all, the value created for shareholders is 1.3 EUR per year in a good year. That gives a cash flow/earnings yield of 4.4% on the current stock price and translates into a dividend of 3.4%. If you look at CA Immo stock price, you will see a PE ratio of 6.51, but that is just thanks to the revaluations. The real return is around 4% which is a bit risky for investing into commercial properties in Europe, at least for me. On the other hand, it is top quality locations and for that you have to pay a premium. So, see how it fits your requirements.

A similar stock that I’ve analysed is Athos Immobilien, but they own housing in Lienz, don’t do much revaluations and have a similar dividend. If you want more safety, check it out.

The CA IMMO Stock Analysis is part of the full Austrian Stock Market Analysis make by Sven Carlin for the Sven Carlin Stock Market Research Platform.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: