February 21, 2025

CNH Industrial: A Cyclical Play in the Agriculture and Construction Equipment Sector

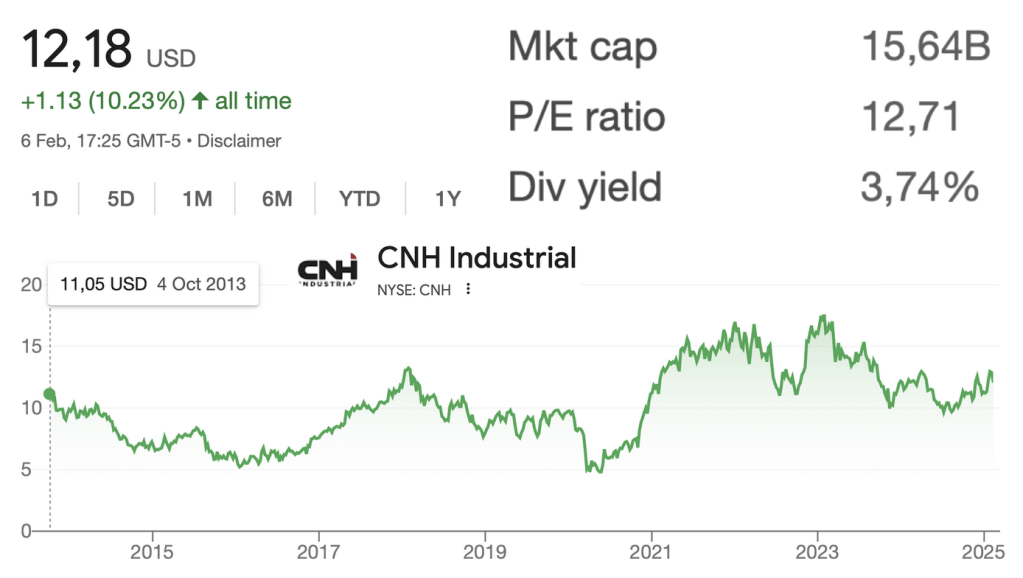

Contents:CNH StockBusiness OverviewCyclical Dynamics and Recent PerformanceFinancial Services and Construction SegmentOutlook and Strategic PrioritiesValuation and Risk-Reward AnalysisConclusion CNH Stock CNH... Continue reading

January 17, 2021

3 Good Grocery Stocks To Watch For Your Portfolio (KR, SFM, AHOLD)

Adding Grocery Stocks to Your Portfolio - Rationale If there are boring stocks that you can add to your portfolio,... Continue reading

Ahold Stock Analysis |Strong Dividend & Buybacks + BOL.COM

Ahold Stock Analysis Ahold Delhaize group – Source: Ahold Here is the video overview discussing Kroger, Sprouts Farmers Market and Ahold for... Continue reading

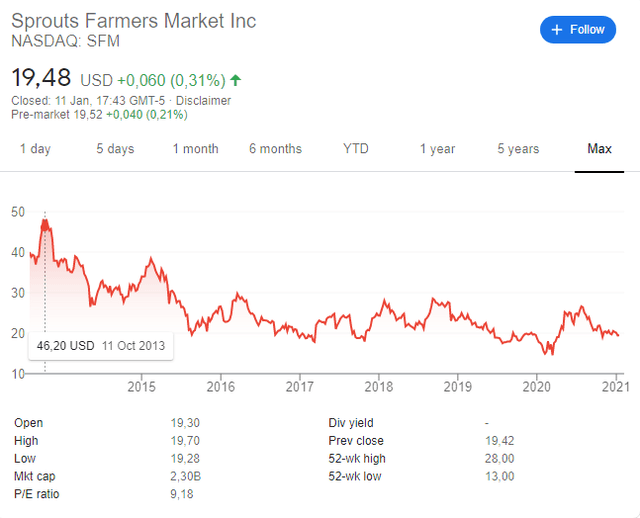

Sprouts Farmers Market Stock Offers Growth And Strong Buybacks

SFM stock analysis video, written analysis continues below. Ahold & Kroger in video too. https://www.youtube.com/watch?v=4dpm_9rBT20 SFM stock analysis SFM stock... Continue reading

Kroger Stock Is Offering Good Dividend & Great Buybacks

Kroger stock analysis Kroger's historical stock price chart shows the company is a compounder, but also that Kroger's stock price... Continue reading

March 16, 2019

ADM – A dividend stock to own for the long term

Contents ADM company overview Investment strategy A few notes from the last conference call My personal opinion I analysed Bunge,... Continue reading

March 12, 2019

Ingredion stock analysis – 10% yield

Summary - Ingredion The operating cash flow yield is 11%, the company expects to grow earnings at 8% per year... Continue reading

March 6, 2019

Food Stocks Sector Analysis And Investment Strategy

Do food stocks offer a margin of safety? Before discussing food stocks as investing opportunities, let me just tell you... Continue reading