March 7, 2025

The Evolution of Financial Goals and the Power of Value Investing

Investing is not just about growing wealth; it’s about aligning your financial decisions with your life goals. Over time, these... Continue reading

December 15, 2020

How To Calculate Intrinsic Value (Formula – Excel template & AMZN Example)

Made by Sven Carlin Ph.D. for the free Stock Market Investing Course. Disclaimer: all content is just for educational purposes... Continue reading

November 7, 2020

Inelastic Market Hypothesis – You Crash Markets

Who Moves Stock Prices? You Do! Inelastic Market Hypothesis Explains Market Volatility. Here is the less technical video, article explaining... Continue reading

February 19, 2020

When To Buy Stocks And When To Sell Stocks – The Six Stocks Categories Tool by Peter Lynch

Six Categories of Stocks – When to buy stocks, when to sell stocks! From One Up On Wall Street by... Continue reading

February 3, 2020

Index Fund Investing Explained with a 150 year Return Analysis of the S&P 500

Index fund investing I recently received an email from Peter asking about investing in index funds. He likes the idea... Continue reading

September 30, 2019

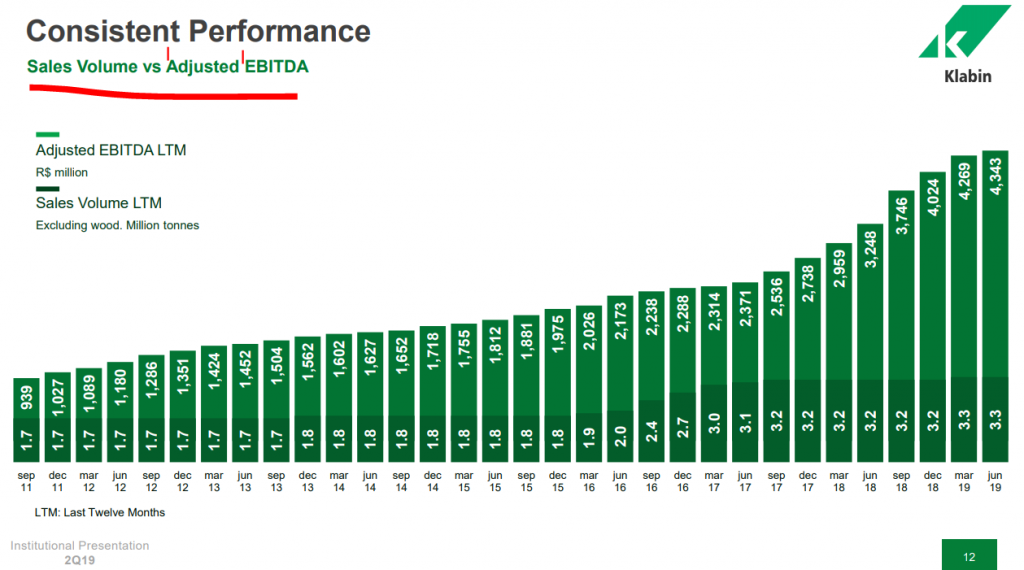

Accounting for investors – Misuse of EBITDA explained

An Accounting Warning by Charlie Munger I am reading Poor Charlie’s Almanack and will discuss the things I find most... Continue reading

September 23, 2019

Fixed versus variable mortgage interest rate – what is the difference in 2019

I’ve made a few videos discussing real estate investing as brick is a key component of one’s financial life. If... Continue reading

May 23, 2019

Tesla Stock Crash – My Message To Tesla Investors

I’ve been a Tesla stock bear over the last years and I would always receive a lot of hate when... Continue reading

May 12, 2019

You can retire by investing in the stock market – just don’t invest like everybody else in index funds

It is possible to retire earlier using the stock market if you focus on investing in businesses. Investing is all... Continue reading

November 14, 2018

How to invest in businesses with dr. Per Jenster

I recently had the privilege to interview dr. Per Jenster. He is a Fullbright scolar, author of many books, former... Continue reading