March 7, 2025

The Evolution of Financial Goals and the Power of Value Investing

Investing is not just about growing wealth; it’s about aligning your financial decisions with your life goals. Over time, these... Continue reading

February 21, 2025

Value Investing: A Strategic Approach to Building a $100,000 Portfolio

What is Value Investing?The Key Drivers of Value Investment ReturnsBuilding a $100,000 Value Portfolio1. U.S. Treasuries (Low Risk)2. Berkshire Hathaway... Continue reading

February 10, 2025

How to Allocate Your Portfolio: A Framework for Investors

ContentsThe Role of Diversification: Knowledge MattersA Practical Framework for Portfolio AllocationKey Drivers of Allocation DecisionsReal-World Examples: What I Own and... Continue reading

November 22, 2024

The Value Investing Risk & Reward Quadrant by Sven Carlin

The core of value investing is taking advantage of market irrationalities by finding low risk and high reward investing opportunities.... Continue reading

November 26, 2020

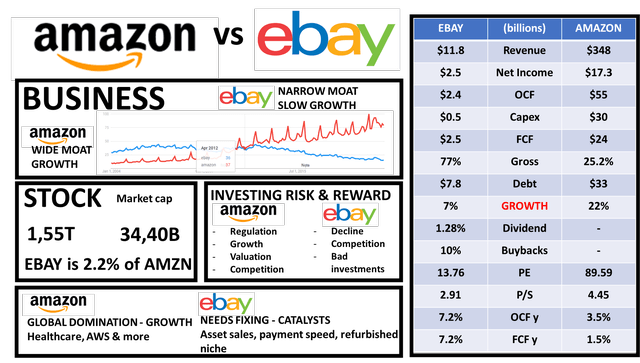

EBAY vs. AMAZON Stock – Both Good

Ebay stock research rationale and Amazon comparison Ebay stock vs Amazon stock – Source: Sven Carlin Ebay is Seth Klarman’s... Continue reading

November 14, 2020

Is Value Investing, Dead Or Alive, Something For You?

There is a plethora of articles and videos attacking value investing, discussing whether it is dead, detrimental, whether people like... Continue reading

March 9, 2020

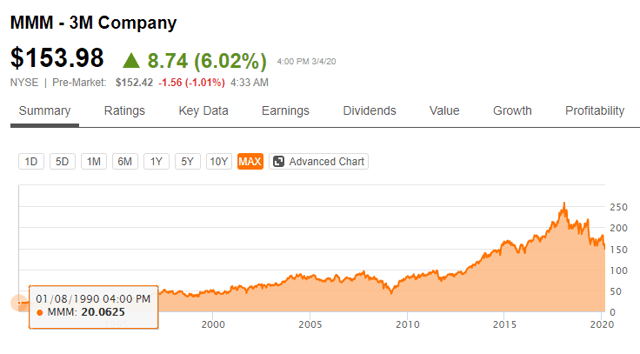

3M Stock Analysis – It is About You, Not 3M

You can write a book about investing in 3M stock (stock MMM), the great business it is, the 118,000 patents... Continue reading

May 10, 2019

How to quickly exclude stocks from further research

Welcome to Value Investing School, article 1 – How to quickly exclude stocks from further research. With this article I... Continue reading

April 3, 2019

Michael Burry’s Stock – CorePoint Lodging REIT Stock Analysis

Introduction. CorePoint Lodging – Business analysis Cash flow calculations Selling properties to unlock value Stock catalysts already there The risks... Continue reading

March 29, 2019

To Buy or to Sell Stocks with Crash Coming? Doesn’t Matter for Value Investors – Buy Value

I received this very interesting comment from a subscriber as I bought my 5th stock for my lump sum portfolio... Continue reading