April 1, 2025

Tesla at a Crossroads: Separating Vision from Investment Reality

If you want a deep dive into Tesla stock, watch the full video about the Magnificent 7 Stocks: https://youtu.be/AgnNJUoXqdU The... Continue reading

Analyzing the Growth Potential of Vital Farms: A Small-Cap, Organic Egg Producer

In recent months, egg prices have become a hot topic among investors and consumers alike. Amidst this discussion, one company... Continue reading

March 7, 2025

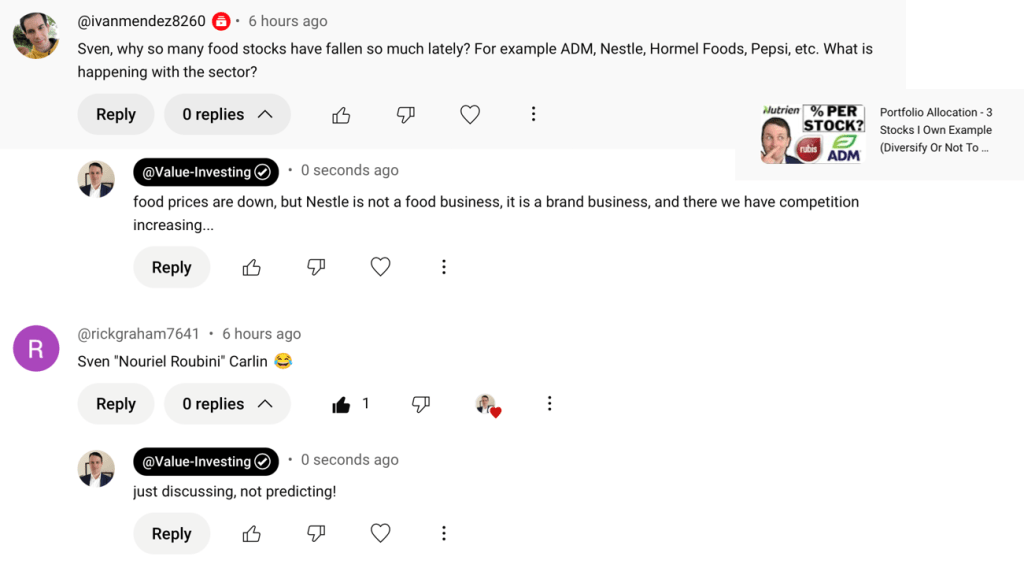

Exploring Opportunities in the Food Sector: A Deep Dive into Food Stocks and Brand Dynamics

The food sector has recently faced significant challenges, with notable declines in stocks such as ADM, Nestle, Hormel Foods, and... Continue reading

Berkshire Hathaway: A Fortress Built for Long-Term Compounding

The full video analysis of Berkshire is on my channel if you want a more in depth analysis: https://youtu.be/JKZQgnBPlb0 Berkshire... Continue reading

High-Yield Dividend Chemical Stocks: Are Dow, BASF, and LyondellBasell Worth the Risk?

Check out the full video on YouTube, if you prefer reading however, keep scrolling. https://youtu.be/EeKhMJyO20k The chemical industry has long... Continue reading

The Enduring Appeal of S&P Global: A Deep Dive into a “Wonderful Business”

In the world of investing, few businesses stand out as consistently exceptional. S&P Global (SPG) is one such company, a... Continue reading

February 21, 2025

Is Ford Stock a Buy Now? A Deep Dive into the Cyclical Nature of the Automotive Giant

Contents:The Cyclical Nature of Ford’s BusinessRecent Performance and ChallengesDividend Sustainability and Cash FlowAnalyst Sentiment and Market OutlookThe Recession RiskIs Ford... Continue reading

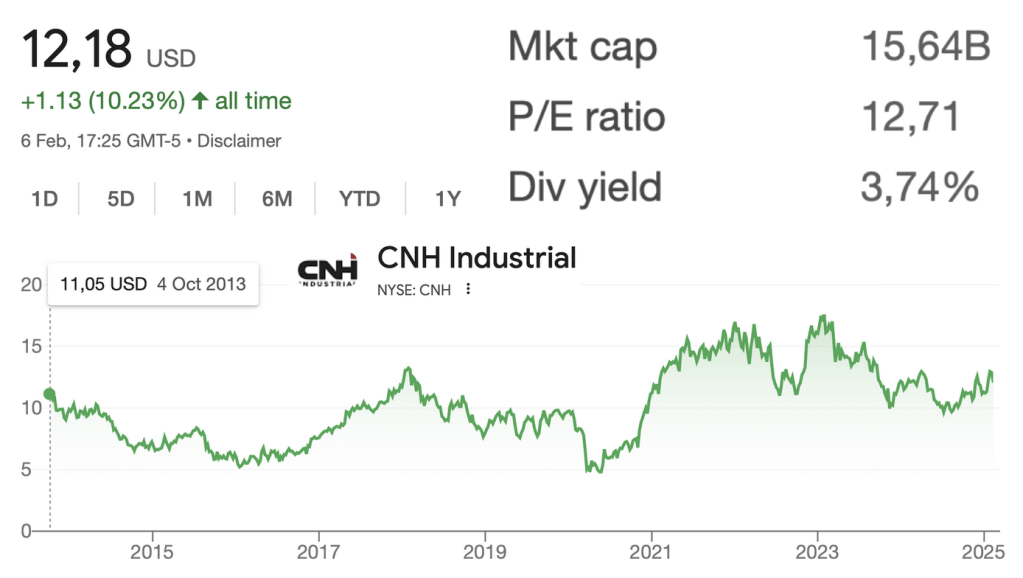

CNH Industrial: A Cyclical Play in the Agriculture and Construction Equipment Sector

Contents:CNH StockBusiness OverviewCyclical Dynamics and Recent PerformanceFinancial Services and Construction SegmentOutlook and Strategic PrioritiesValuation and Risk-Reward AnalysisConclusion CNH Stock CNH... Continue reading

February 10, 2025

Understanding the Intrinsic Value of the S&P 500: A Guide for Investors

Contents:What is Intrinsic Value?Key Inputs for Calculating Intrinsic ValueAnalyzing S&P 500 Earnings and DividendsEstimating Earnings GrowthValuation and Expected ReturnsRisk and... Continue reading

January 25, 2025

Is Apple Still a Good Investment? Analyzing China Risks, Buybacks, and Intrinsic Value

Apple’s Challenges: China and Declining iPhone SalesThe Buyback Debate: Warren Buffett’s PerspectiveIntrinsic Value AnalysisWall Street’s Expectations vs. RealityRisks to ConsiderIs... Continue reading