March 7, 2025

Berkshire Hathaway: A Fortress Built for Long-Term Compounding

The full video analysis of Berkshire is on my channel if you want a more in depth analysis: https://youtu.be/JKZQgnBPlb0 Berkshire... Continue reading

June 13, 2021

Is Berkshire Hathaway Stock A Buy Now? Not in my opinion! (50% downside)

I have been following Berkshire Hathaway stock for years now and I even bought BRK.B in May of 2020 because... Continue reading

February 11, 2021

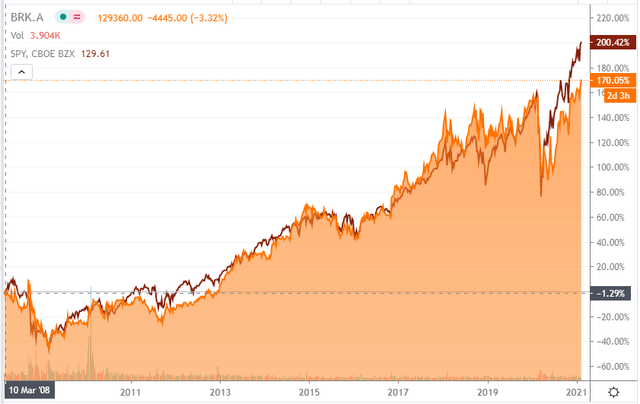

Berkshire did not underperform the S&P 500 despite returning ‘only’ 9% yearly vs 12% since 2008

Whenever I discuss Warren Buffett and Berkshire there is multitude of comments on how Warren Buffett underperformed the S&P 500... Continue reading

October 7, 2020

Berkshire Stock When Buffett Dies (Management Outlook)

I’ve recently made a Berkshire stock sum of parts valuation and, like it is always the case when I talk... Continue reading

September 30, 2020

Berkshire Hathaway Stock Valuation – Just Burlington is Worth $200 billion

Berkshire Hathaway stock valuation - sum of parts I recently did a full sector analysis of railroad stocks and to... Continue reading

May 9, 2020

Berkshire vs S&P 500 – BRK is Better (Quality over Quantity)

BRK stock went down during last week because many focus on the negative conotations from Buffett's shareholder meeting; airlines, no... Continue reading

October 15, 2019

BYD Stock Analysis – The Chinese EV Maker Owned by Buffett

BYD Stock and Chinese stocks in general are getting cheap; trade wars, fears of China slowing down and a global... Continue reading

August 25, 2019

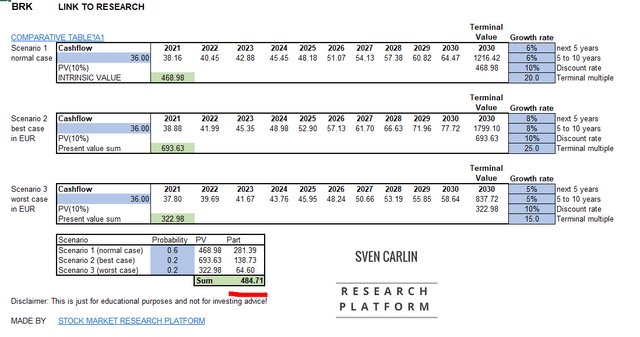

Berkshire Hathaway – Intrinsic Value Calculation

Contents Defining intrinsic value Berkshire’s return on invested capital Berkshire’s future cash flows Insurance business Railroads, manufacturing, utilities and other... Continue reading

January 27, 2019

Kraft Heinz Stock Analysis – Let’s go to the store

Contents Introduction. 1 KHC’s stock fundamentals. 3 KHC’s business strategy. 5 Increasing dividend would make KHC great again. 5 You... Continue reading

October 21, 2018

Berkshire stock is better than the S&P 500 – check your portfolio holdings!

BERKSHIRE's INVESTING MINDSET Towards the end of Benjamin Graham's book, The Intelligent Investor, we can find the following advice (Chapter... Continue reading