S Immo Stock Analysis – Good Dividend, Good Value

S Immo AG stock analysis is part of my full, stock by stock analysis of the Austrian Stock Market that offers interesting investing opportunities. Check my Austrian Stocks List for more Austrian stocks.

The analysis consists of a stock price discussion, a business overview presentation, a valuation, and an investing conclusion.

S Immo stock price analysis – VIE:SPI

The S Immo stock didn’t reward shareholders between 2009 and 2014. However, it exploded afterwards by over 400 % until the COVID-19 crisis in 2020.

The stock crashed about 50 % and is still down 38 % from its all-time high. S Immo is one of the few stocks that did not recover yet and is a potential bargain compared to past price levels. On the other hand, the real estate environment might have been changed forever by COVID, so we have to analyze the specific impact on S Immo.

S Immo offers a 4.38 % dividend. The sharp March 2020 stock price does not mean that the S Immo stock is undervalued. First, we need to look at the business fundamentals and the valuation, then see how it fits one’s portfolio.

S Immo stock analysis – Business overview

S Immo is an international real estate group that is involved in buying, selling, and real estate project development. Additionally, S Immo operates hotels and shopping centers and renovates properties. Those are not great places to be at the moment, but if things return back to pre-COVID levels, S Immo could be back on track again.

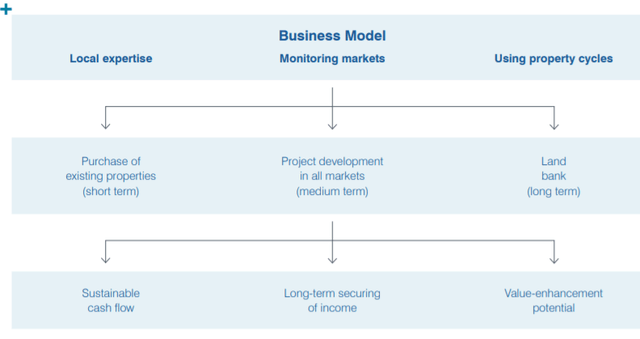

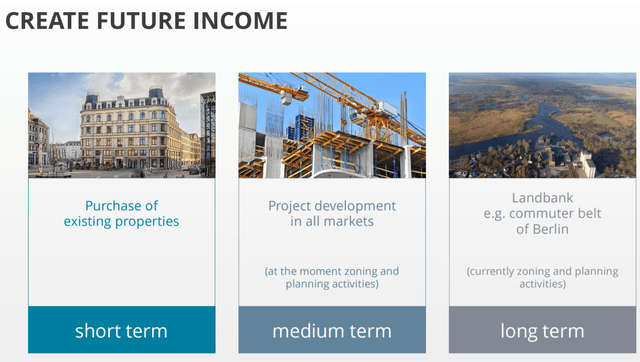

S Immo long-term goal is to achieve sustainable cash flow, secure long-term income, and value-enhancement potential through purchasing existing properties, project development, and developing its land bank. S Immo’s land bank is near larger German cities with good demographic and economic potential like Leipzig, Kiel, and Erfurt. Also, S Immo owns land in Berlin. During the last two years, S Immo acquired 2 million square meters of space in Berlin’s commuter belt.

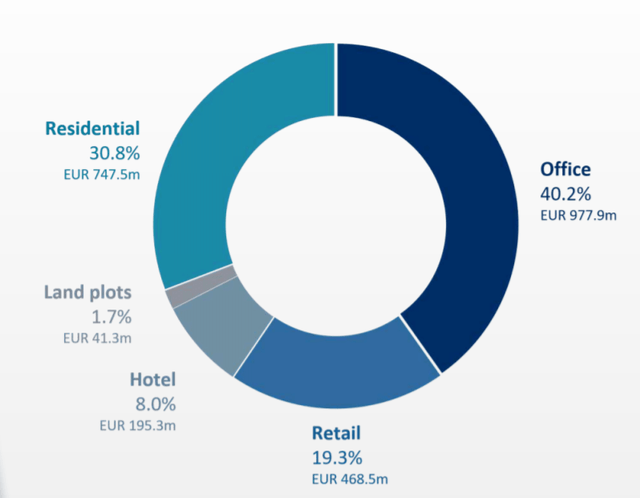

Retail, office and hotel could have issues going forward due to COVID and those make almost 70% of S Immo’s property values.

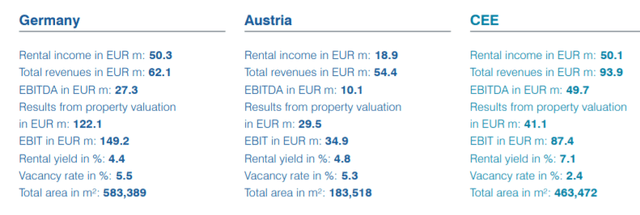

In Germany and Austria, the rental yield is nearly the same as is the vacancy rate. Properties in the central and eastern European countries (CEE) have a much higher rental yield and lower vacancy rate which is very interesting. The valuation of real estate depends on the required yield and therefore varies from country to country. In total, their rental yield is 5.4 % which is a good cap rate for real estate in general. This number is important for later in this analysis when comparing it to their cost of capital and expected yield for investors.

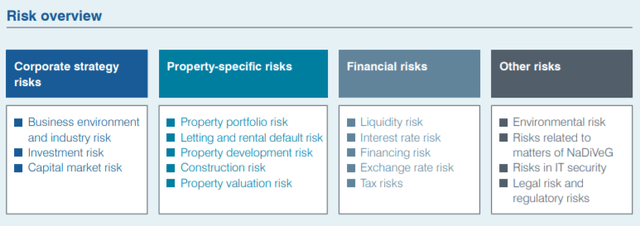

The risks of the business model are seen below.

Nothing quite frightening there as these are standard risks for all of the real estate companies out there. The company focuses on a diversified property portfolio in central Europe (Germany, Austria) and promising countries from eastern Europe.

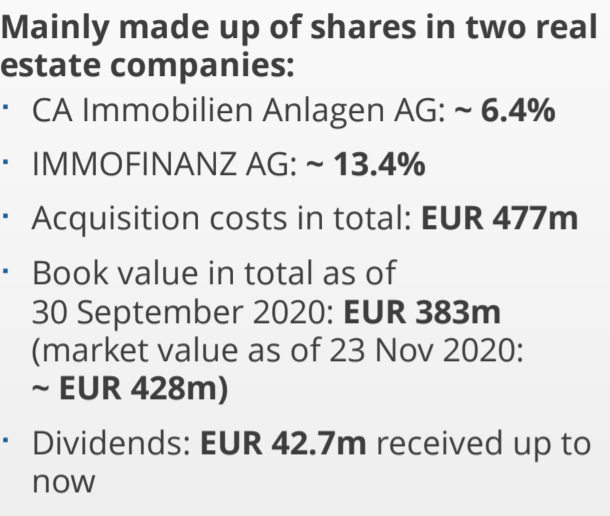

Besides their primary business model, S Immo holds stakes in CA Immobilien (CA Immo stock analysis) and ImmoFinanz (ImmoFinanz AG stock analysis) shares and receives 42 million EUR dividends in 2019. CA Immobilien offers a cash flow yield of 4.4%. Both companies are not the safest real estate best and a change in environment could be tricky long-term.

On the COVID-19 crisis, the management says that “This crisis will also pass.” In detail: On residential properties, they expect no negative impact on rent levels and vacancies. However, they see a positive effect on demand and valuations. For offices, there is a decline expected, but it is minimal. They do not think that retail will suffer much as they hope for multi-channeling, so stationary and online trade complementing each other. This is merely hoping by the management as recent surveys show that people shop online more and more, and the number is still rising. 80 % of every internet user in the US ordered something online in 2019. For their hotels, they expect the recovery to take two to three years.

S Immo Stock analysis – Valuation

A real estate business can be valued either by looking at the value of its assets or the cash flow. I prefer the cash flows are the value can only be determines when you sell, accounting values are just in accounting values.

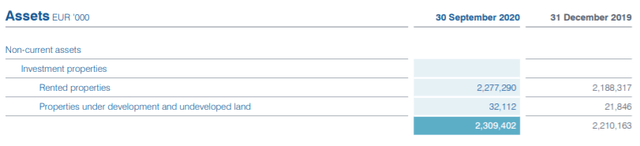

S Immo has 2.3 billion EUR in assets; after deducting 1.6 billion EUR in non-current and current financial liabilities, the result is about 700 million EUR in net asset value. Adding the cash and removing other liabilities, the shareholder equity is at 800 million EUR which is below the market capitalization of 1.1 billion EUR.

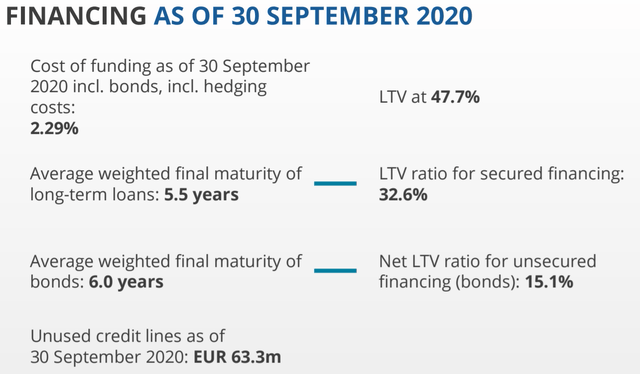

S Immo has a one bond with a coupon near its rental yield but most of the debt is lower and will likely be refinanced even lower given the low rates situation in Europe.

The general cost of funding for S Immo is about 2.29 %. So, the spread between the rental yield (5.4%) and the cost of capital is 3.11 %. This spread is what the company invests in and how the company makes money, on top of the invested equity.

The value of real estate depends on interest rates (resulting in the cost of funding). The value of the stock will also depend on interest rates, but forecasting interest rates is really hard. On the other hand, the cheap debt and real estate could offer protection in case we see higher interest rates due to inflation. Something that might happen give the amount of money being printed in Europe and the bad economies with high government debt levels.

Given future interest rates are hard to predict, a better way for a value investor is to look at the cash flow because these are comparable to other investing opportunities. Then you can decide whether if the company fits your investing requirements. Why take the cash flow and not earnings?

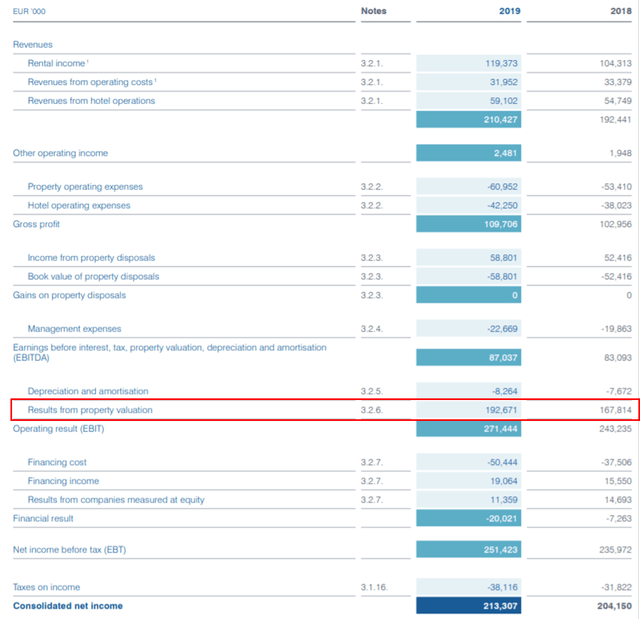

An accounting practice often applied by real estate companies is a constant positive revaluation of its properties. These revaluations are non-taxable accounting practices that increase net profits. But in case the market turns against the company, these revaluations must be reversed which is something that can happen. Of the 213 EUR in net income came 192 million EUR from the revaluations of the properties, which is about 90 % of the net income.

The funds from the operation, which are the best way to value a real estate company, are 64 million EUR or 0.87 EUR per share in 2019. With the current stock price of around 16 EUR, S Immo generates a value of 5.2 % for the investors. The fund from operation yield is near the dividend of 4.48 %.

Future growth depends on new purchases of existing properties in the near term. S Immo’s latest acquisition is the Zagrebtower, a thoroughly let office property with a total rental area of 26,000 square meters. With their rental properties, S Immo can increase the rent for a bit of growth in line with inflation. No major catalysator for a stock price increase is hidden within the company. In good years the company can grow by 3 to 4 % through acquisitions and project development.

S Immo Stock analysis – Conclusion and investing outlook

In conclusion, S Immo creates a shareholder value of 0.87 EUR in a good year for a 5.2 % cash flow yield. That might sound low, but compared to what you get in a bank or compared to other dividend yields these days, it could also be a really good play for dividend investors looking for real estate exposure.

Let’s say that they can increase their rents by 2% per year and that the value of the real estate increases too 2% per year due to inflation. In that case your long-term investing returns will be determined by the dividend, the capital gain on the real estate values and the growth in income.

If you are looking into a diversified German/Austrian real estate player, S Immo is a good option for a portfolio.