How To Invest In REITs – Pros, Cons And Simon Property Group Example Analysis

Content:

How To Invest In REITs – Pros, Cons And What Are REITs

Introduction – REITs have been the best investment over the last two decades

What impacts REITs as investments – dividends and capital appreciation

Pros and cons of investing in REITs

The pros of REITs

The cons of investing in REITs

Simon Property Group REIT analysis (NYSE: SPG)

SPG company overview

Densely populated areas and high demand lead to positive lease spreads

Dividend is just 65% of funds from operations but still yielding 5%

Self-funded growth and investments

SPG’s debt

The retail environment in the coming years

This article is about the general pros and cons of investing in REITs and about Simon Property Group (NYSE: SPG), used as an example to show what to look at when investing in REITs.

Introduction – REITs have been the best investment over the last two decades

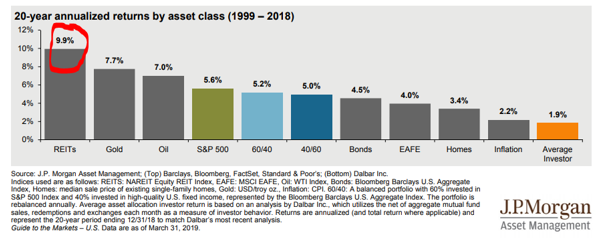

REITs (Real Estate Investment Trusts) have been the best performing asset class in the last 20 years with an average return of 9.9%. This much better than the 5.6% return of the S&P 500 and even better than gold or oil.

Source: Raymond James

The most important point to note is that despite the S&P 500 returned 5.6% per year, the average investor got a return of 1.9%. This really emphasizes Graham’s statement:

“The investor’s chief problem — and even his worst enemy — is likely to be himself.”

Buffett always suggests to read chapter 1, chapter 8 and chapter 20 of Benjamin Graham’s book The Intelligent Investor (full summaries in the links) to avoid making the mistakes average investors usually make, which is to buy high during exuberant times and sell low in panicky times. I know some that sold in March of 2009 and bought back only in 2015. Nevertheless, this is not a story about investment mindset on which you already have the links to Graham’s book above, this is a report on whether it is smart to invest in REITs now and whether we can expect a similar performance in the next decade or two. In this article we will discuss:

- Why did REITs do that good

- What impacts REITs as investments – dividends and capital appreciation

- Pros and cons of investing in REITs

- Put all into perspective by analysing Simon Property Group (NYSE: SPG)

The goal of this article is to check whether it is smart to invest in REITs now, compare the possible rewards to the risks and avoid being the average investor, as average investors will again underperform almost anything else over the long term.

Why did REITs do that good over the past 20 years?

The main reason REITs did good are interest rates. In 1999, from when the previous chart measured performance, interest rates have gone mostly down.

Source: Raymond James

In 1999, you would get $6,000 on $100,000 in a normal savings account while during the last years, you would get less than $1,000.

However now, some cash investments accounts do generate around 2% as interest rates increased. Consequently, REITs did extremely well up to 2016, then as interest rates started going up, then there was a bit of a pause due to the FED making a few hikes, but since Powel capitulated on higher interest rates, REITs resumed their growth.

Source: iShares Core U.S. REIT ETF

The above clearly indicates that REITs are interest rate plays. If you can get a 6% return on government guaranteed savings, you are going to expect a much higher yield from various real estate investments that are always risky.

However, real estate investments, unlike bonds, offer inflation protection as the value of the properties might go up in the future and you can increase rents, thus some REITs should even deserve a premium. Additionally, REITs usually borrow money to acquire real estate or mortgage backed securities and thus interest rates play two roles. One comparative for investors that we just explained and the second for their margins as the higher the interest rate spread, the higher the profits of the REIT. The interest rate spread is the difference between the interest the REIT is paying on the loan and the yield on the mortgage backed security it bought, for example.

The iShares Core U.S. REIT ETF has a yield of 3.5%. If investors would suddenly expect a yield of 7% because of a higher interest rates environment, the value of REITs would probably half.

Source: iShares Core U.S. REIT ETF

One might look at the above 3.5% yield and say no way because it is too low, but we don’t invest in markets or indexes, we invest in individual businesses and therefore we must look at individual opportunities. Plus, REITs are not only about dividends.

What impacts REITs as investments – dividends and capital appreciation

Many focus on dividends as the only return metric for REITs. However, investors can expect returns in the form of capital appreciation too. If you can increase rents, the value of the underlying real estate will probably go up in the future. Plus, as the targeted inflation rate is above 2%, we can add a minimal 2% yearly dividend return that we can expect from capital appreciation.

This is also what I am going to focus on while researching REITs:

- First, we have the dividend that is paid out of the REIT’s funds from operations (FFO).

- Second, if the dividend is smaller than the FFO, it means that the REIT has space to self-fund its growth, that should add too to the investment picture.

- Third, given the huge money printing over the past decade and likely increase in the future, I think there is a high chance of high single digit inflation where owning good real estate comes in handy.

Let’s summarize the pros and cons of investing in REITs and start this REIT overview by looking at the largest position of the USRT REIT, Simon Property Group (NYSE: SPG). The stock is close to its 52-week lows, offers a 5% yield, so it looks like a good start to understand the sector better.

Pros and cons of investing in REITs

The pros of REITs:

- You can own real estate without the hustle of repairing toilets

Real estate investment trusts are internally self-managed or externally managed vehicles that take care of real estate for you; collect rent from tenants, pay expenses and give you what is left in the form of dividends. There two main types of REITs; equity and mortgage REITs. Mortgage REITs invest in mortgage backed securities while equity REITs invest directly in real estate.

Further, you have many various specialized REIT like land REITs, apartment, senior housing, single family, hotels, retail, commercial, offices, healthcare, storage, data centres, industrial, timberland and many other specializations. There is a REIT for practically anything related to real estate and those that do more are called diversified REITs.

- REITs have to pay out at least 90% of income through dividends and pay no income tax

REITs are especially attractive to income seeking investors as more than 90% of income has to be paid out in the form of dividends. If not, a REIT might lose its REIT status which also brings the benefit of no corporate income taxes. Therefore, payments to shareholders can be substantial, especially over time.

Finding the REIT that manages to grow, have a higher yield from the invested properties than the cost of capital and thus the capacity to increase dividends, is the holy grail of investing in REITs. We are going to do out best to find REITs that have the potential.

- Real estate usually appreciates in value and offers inflation protection

Apart from the above-mentioned dividend and income, REITs can offer huge returns from capital appreciation. If there is inflation and you own real estate while you have long term debt with fixed interest rates, you would be in REIT heaven. (we already used the holy grail anecdote so heaven is better here). REITs can simply increase rents or hotel room prices if there is inflation. Of course, if the property offers quality.

The key is to hold those REITs that will continue to see the value of their real estate appreciate. Empty malls, ghost cities or abandoned factories are definitely not a good sign for capital appreciation.

- Liquidity

Even if liquidity should not be a concern for long term investors, you can sell your REIT by on click on your mouse. Something you can’t do when you own real estate.

The cons of investing in REITs:

- Interest rate risk

We already mentioned how REITs depend on interest rates as lower interest rates have been a key factor in their boom. However, if a REIT is a great business, has great properties and a good business model, you shouldn’t worry much about interest rates as lower REIT stock prices would allow you to increase your yield on the reinvested dividends and consequently your long-term returns.

- REITs use a lot of leverage

As REITs have to pay out more than 90% on their income there isn’t much left for growth. As ‘no growth’ is practically the most hated situation on Wall Street, managements tend to do whatever it takes to keep growing which includes risky acquisitions or mergers, overinvesting in new properties even if the market is saturated and not having a margin of safety within the interest rate spread.

- There is high competition

Investing in real estate is like investing in stocks. As would Peter Lynch say, the more stones (stocks) you turn, the number of great investments you find will be larger. You can check my video on How to invest in real estate here if you wish to hear my views on what makes the difference when it comes to investing in real estate.

However, REITs usually invest in large properties, there are usually many bidders for such projects and, especially if the property is of high quality, initial investment prices can be sky high. Therefore, by investing in REITs you miss on the opportunity to really find the best bargain in the neighbourhood or a fix-up that doesn’t really need that much work but others don’t see it. Such laser focused real estate investing allows you to make money immediately when you buy as you pay less than what the property is actually worth.

Some REITs trade below net asset value but there is usually a reason for that, it can be the management, trends, new competition etc.

- Most people already own a home

By owning your home, you are already exposed to many of the real estate benefits mentioned, especially if you have a low interest rate 30-year fixed mortgage. Therefore, having a heavily weighted REIT portfolio alongside owning a home and maybe a rental unit, might make you too exposed to the real estate market that, as we have seen from 2009 to 2013, doesn’t always go up.

- The dividends are taxed as income

Taxes are always personal but you have to check how will the dividends you receive from REITs be taxed or you might want to hold REITs in non-taxable accounts. This is an even bigger mess for non-U.S. investors.

- Some real estate sectors are being hit hard, think of retail

Given the boom in e-commerce, retail is hit hard and consequently REITs owning retail stores suffer. On the other hand, REITs owning distribution centres do well, so be careful when buying REITs and either buy absolute bargains or REITs that have strong sector tailwinds.

- REITs were created in the 1960s and boomed only in the last 30 years

The first REITs were created in the 1960 while REIT investing became really popular only in the last few decades. Therefore, you might be buying in exuberance as average investors usually flock into buying exuberantly priced assets after the low risk/high return gains have already been made.

- The risk of a recession

When discussing almost any business, you will hear how it would be impacted by a recession. REITs would be no exception but perhaps investors still have a bit too much of 2009 in their memories. Further, as we can’t anticipate a recession, perhaps it is best to simply know your portfolio will suffer, at least temporarily, reinvest the dividends and enjoy the ride up when the recession is over. Therefore, yes, earnings might fall and dividends might get cut, but that is with every business and many didn’t invest in 2010 fearing a recession. No need to mention how they feel now.

Let’s now put all the above into perspective by analysing a very large REIT, Simon Property Group.

Simon Property Group REIT analysis (NYSE: SPG)

I want to start this REIT analysis series by analysing one of the best REITs out there, Simon Property Group (NYSE: SPG). I’ll also use it to explain what you need to know when investing in REITs:

- The dividend yield, buyback, growth and capital appreciation return

- The interest/lease spread

- Funds from operations (FFO or AFFO – adjusted)

- Focus on debt

- Sector trends

SPG company overview

SPG owns malls and outlets in the US, Europe and Asia.

Source: SPG – The Shops at Crystals, Las Vegas NV

I am going to focus on the key aspects of investing in SPG and avoid a purely descriptive chapter as you can learn much more about the business from their Investor Presentation. Just shortly, 79.5% of net operating income comes from U.S. malls and outlets, 11.7% from the Mills, a REIT they acquired in 2007, and 8.7% is international.

Source: SPG

The key factors for SPG are the following:

Densely populated areas and high demand lead to positive lease spreads

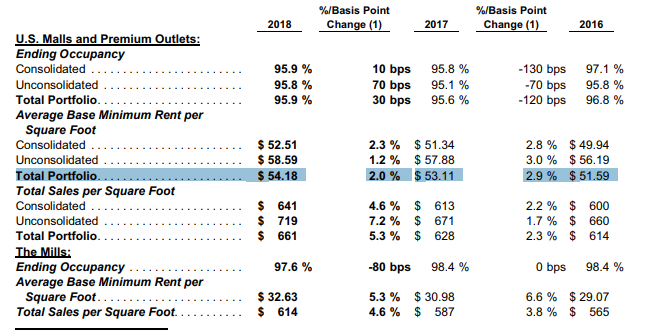

Despite the turmoil in the retail sector, SPG keeps increasing rents and keeps occupancy at high levels. Average leases per square foot increased from $51.59 in 2016 to $54.18 in 2018. If a company can increase rents and keep a high occupancy rate, it means their customers aren’t really in that much trouble.

The lease spread is the difference between the new lease in comparison to the lease of the previous tenant.

Source: 2018 Annual Report

SPG is considered a high-quality REIT, with great assets and therefore it can increase leases.

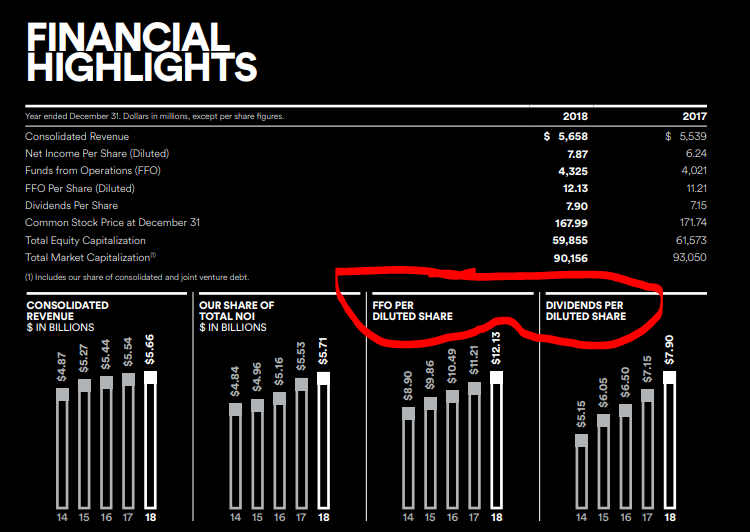

Dividend is just 65% of funds from operations but still yielding 5%

Funds for operations (FFO) is a crucial metric when it comes to analysing REITs. FFO describe what is left after all the expenses are paid. The management has to distribute more than 90% of net income as dividends but don’t forget that a non-cash expense when owning real-estate is depreciation. Thus, the cash flows are usually higher than net income. Therefore, SPG can self-finance its growth as it is practically distributing only 65% of what it could distribute. This leaves room for buybacks and investments on top of the 5% dividend yield.

Source: 2018 Annual Report

In February 2019 SPG announced a new $2 billion dollar buyback program for 2019 and 2020. If they spend all the available $2 billion on buybacks, that would add a 1.7% yearly buyback return to the dividend as the market cap is currently $57 billion. This would put the expected investment return to 6.7% already. But that is not all, there is still room for growth.

Self-funded growth and investments

The company is building new developments and refurbishing existing malls.

Net operating income growth was 3.2% in 2018 and 4.2% on average over the last 4 years (this includes inflation). Even if we put a conservative 3% growth rate on net operating income, the growth should increase income by 80% over the next 20 years that should consequently add another 3% to the return from SPG.

Summing up the 5% dividend, 1.7% buybacks and 3% growth, the expected yearly return from SPG could be 9.7% over the next decade or two.

SPG’s debt

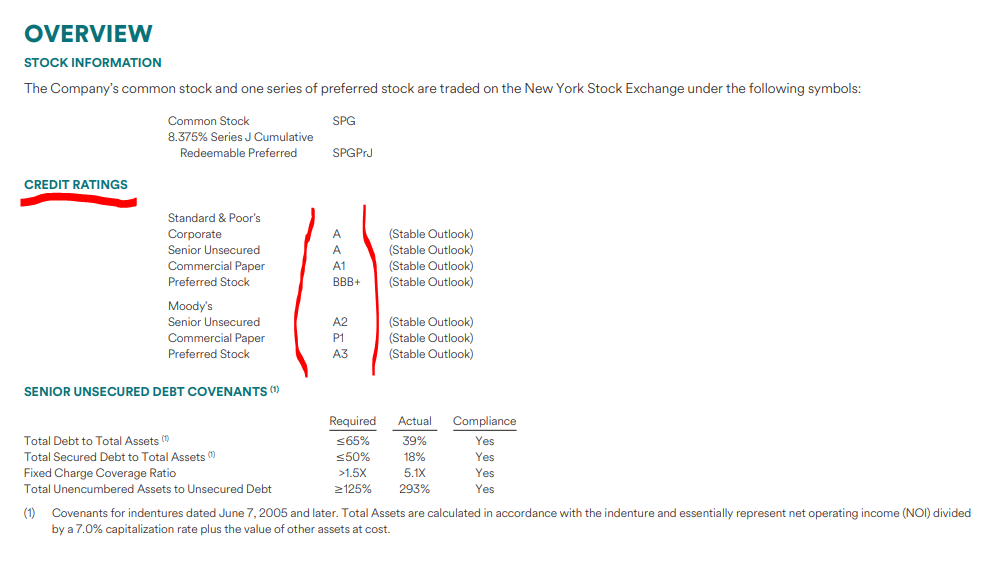

When it comes to debt, SPG is as good as it gets with A credit ratings. This means that whatever hits the economy, SPG should not have trouble to service its debt payments.

Source: Investor Presentation Q1 2019

The only thing that is concerning a bit but it might also be a management decision, is the shorter debt maturity. This is necessary to keep the same interest rates as the cost of debt went up over the past years, but longer fixed interest rates are always nicer.

Source: Investor Presentation Q1 2019

Logically, SPG has most of its debt on fixed interest rates.

Source: Investor Presentation Q1 2019

What is really interesting are the interest rates in Europe. The Noventa di Piave designer outlet close to Venice, where I have been once when returning from a visit to Venice and Padova, has a fixed interest rate of 1.95% maturing only in 2025. This implies SPG might easily grow in Europe as interest rates are ridiculously low.

Perhaps there will be other acquisitions. As long as the net operating income is higher than the cost of capital needed to service the acquisition debt, it pays to growth via acquisitions. This might add another percentage point to the returns over the long term.

However, there is always a catch.

The retail environment in the coming years

This is the main question to answer when it comes to retail REITs, are these outlet centres going to still be interesting to consumers in 5 to 10 years? Or, will we be so entangled into virtual reality that a visit to an outlet or mall will be considered a waste of time?

The answer to the above questions is unknown, some may be more or less convinced but the reality is nobody knows what the future brings. As investors we have to think about what can happen and then put it into an investing perspective.

Things could continue as those are now, thus SPG should continue to pay a 5% yield that should probably grow between 3% and 5% per year, the company should continue to do buybacks and the expected return should be close to 10% per year.

E-commerce might even boost SPG’s growth as omnichannel might lead online sellers to open stocks in high-end locations.

However, if there is less interest for malls and outlets, revenues might stagnate and consequently eliminate the additional 3% yearly return coming from growth. SPG owns class A malls and outlets while market specialists predict closures for class C and D malls. Mall bankruptcies might even increase the number of visitors for SPG.

Another risk is always interest rates, if interest rates go up, SPG’s spreads might decline.

I think the above described uncertainty is what the market is pricing in because if not, you wouldn’t find a high-quality REIT like SPG offering a 10% total yearly long-term return.

I am going to continue to look at REITs and at the end of the sector analysis we are going to compare what is out there and perhaps find something to watch or even invest in. The fact that one of the largest REITs in the U.S. possibly offers 10% is encouraging for further REIT research.