Immofinanz Stock Analysis – Risky Real Estate Business

Immofinanz AG is a European real estate company focused on offices, retail parks and shopping centres. This analysis will comprehend the following:

- Immofinanz stock overview

- Immofinanz AG business overview

- Immofinanz stock fundamentals

- Immofinanz AG dividend and investment thesis

This Immofinanz stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian stock market. Check the list out for more Austrian stock analyses:

The author: Sven Carlin, Ph.D. – I am passionate about stock market research because I believe a bottom up approach leads to finding the best long-term investments out there. My rule is to turn as many stones as I can to find the best ones. If you enjoy this analysis and approach, don’t forget to subscribe to my newsletter at the bottom of this article.

Immofinanz stock and sector overview

Immofinanz stock is traded in Vienna since 1994 with the ticker IIA, consequently also on German exchanges and also in on the Warsaw Stock Exchange since 2013.

The company spun off Buwog in 2015 which was the residential arm of the real estate corporation. Buwog AG was taken over by Vonovia in 2018.

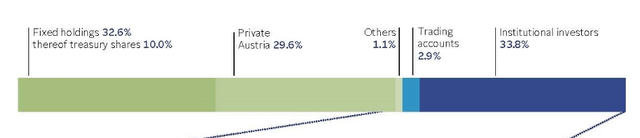

The free float is approximately 72%.

Its stock chart shows the dangers of investing in leveraged real estate vehicles. Immofinanz stock went form a level above 125 EUR in 2007 to just 3 EUR in 2009. It recovered a bit from the 2009 crisis but has been hit hard by COVID and the stock is trading in the mid teen range since.

If things return to normal, the 5.9% dividend Immofinanz has been offering is an attractive yield that will not stay that high for long, if things return to normal, as I said. I’ll make an analysis firstly using the assumption that things will return to normal eventually and then also looking at the risks for Immofinanz if things don’t return to normal that quickly due to COVID.

Don’t get fooled by the price to earnings ratio of just 6.26 because most of the earnings the company declares are from real estate revaluations. When things get rough and interest rates increase, revaluations backfire and can easily erase all the equity of a leveraged real estate business like it was the case in 2009. Something similar is the case with CA Immo where I explained the risks of revaluations.

The market capitalization is 1.75 billion EUR. Keep that number in mind as we will use it later in the valuation part.

Immofinanz AG – real estate outlook

When it comes to real estate, we must also keep in mind that the population in Europe is aging and that demand for offices, retail and shopping centres might be in a downward trend over the coming decades as there is a plethora of factors impacting the sector:

- There has been a big boom in the sector over the past 20 years and is still continuing in Eastern Europe where the company is highly exposed

- There is no population growth to justify further growth

- Online shopping has had a huge impact on how we shop and that impact will be even larger after COVID-19. Online shopping is growing fast in Eastern Europe as it was not possible to have things delivered to your home a few years ago.

- On the other hand, due to huge amount of money printing by the ECB, owning real assets is the only option we as investors have because currencies will be debased, as it has always been the case through history. (Roman coins went from 99% silver to less than 25%)

Let’s take a look at Immofinanz AG.

Immofinanz AG business overview

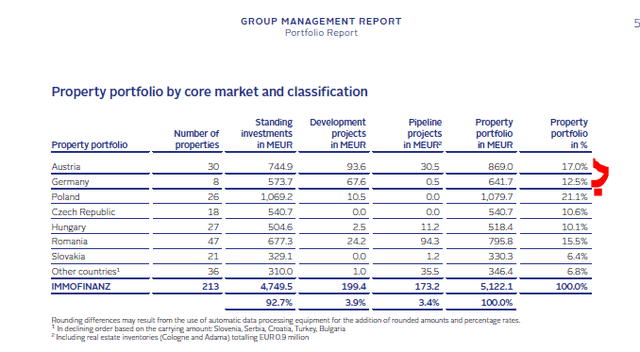

The property portfolio has a carrying amount of EUR 5.1 billion and covers more than 210 properties (December 2019). Seven core markets form the geographical focus of our business activities are Austria, Germany, Poland, Czech Republic, Slovakia, Romania and Hungary. As less than 30% of assets are in Austria and Germany, we could call Immofinanz risky due to currency risks and emerging market risk thanks to the exposure to Poland (21.1%), Romania (15.5%) and other Eastern European countries.

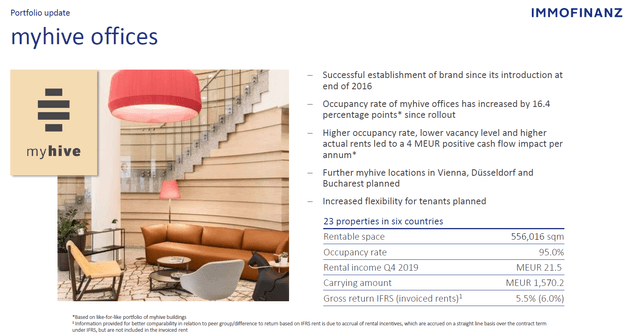

The core of the business is “the hive” real estate brand for offices which they call innovative. Whenever I hear the word innovative when it comes to investing, I become extra careful because those words are usually used by those selling a story without foundations. The carrying value amount is 1.57 billion EUR.

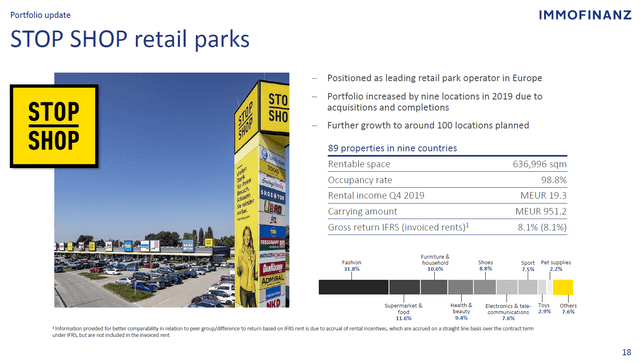

The second segment of the business are retail parks with their “Stop Shop” brand. The question here is about how will future trends look like because if negative trends hit these retail places that don’t have much more to offer than those cheap stores, the situation for the company might get really ugly. The company is already negotiating with retailers due to the COVID issue so we will see how it will turn out.

The gross return from invoiced rents is 8.1% which is much higher than the 5.5% return on the offices, but it also indicates the higher risks related to such a business. The carrying value amount is 0.95 billion EUR.

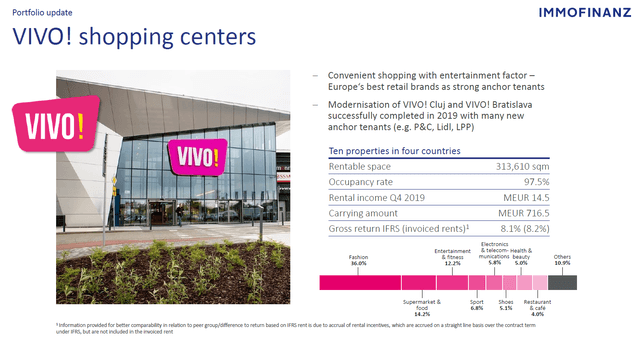

The third pillar of the company are the Vivo shopping centres with a carrying amount of 0.71 billion EUR.

The future of the business will depend on retail traffic and trends in Eastern and Central Europe, the economy there and on interest rates. Let’s discuss that more within the fundamental analysis.

Immofinanz stock fundamentals

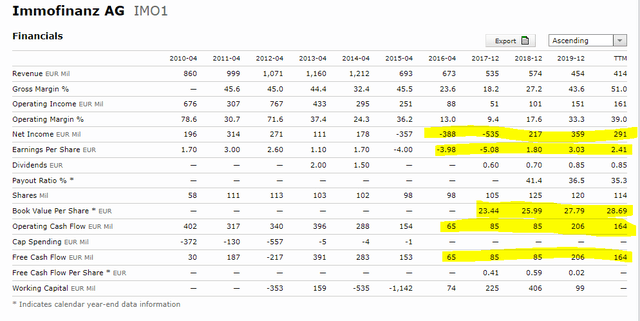

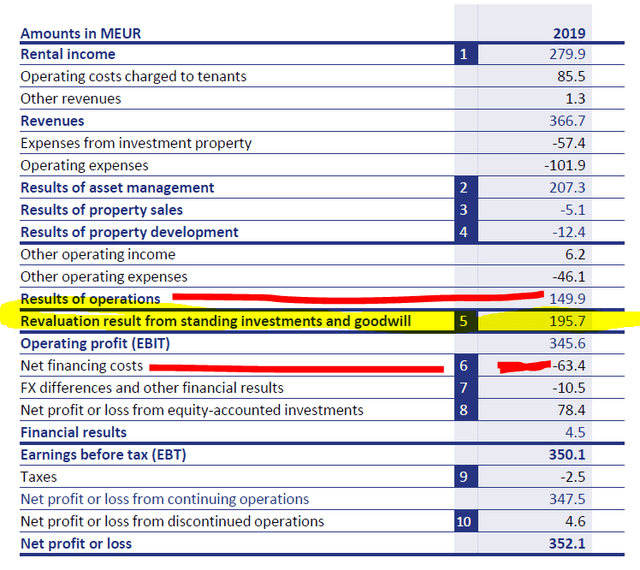

Over the past years, earnings have been very positive and reached 359 million in 2019. But, keep in mind most of those earnings are from revaluations and are not available as free cash flows. Revaluations also push the book value higher and up to 28.60 EUR as of now.

One might wonder how can the book value of real estate be twice as much as the price of the stock? Well, the book value shows the results of valuations based on past metrics, the stock price projects what the market thinks will be the future value.

Net cash flows from operations have been 149 million in 2019, from that we have to deduct 63 million EUR in interest costs and the shareholder value creates is less than 90 million. There is also an equity account but I don’t know if that is from revaluations or real profit. The revaluations account in 2019 was as high as 195 million EUR. As a real investor, I care about cash flows and not so much about fictive values set by accountants.

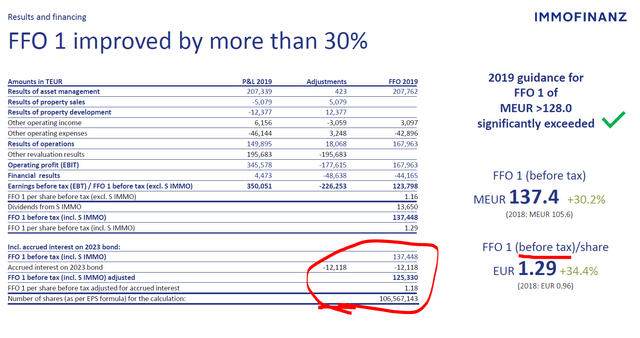

What we have to focus on are funds from operations, something that should be on the first page of every report form the company and not mentioned first on slide 29 of the company’s presentation.

The FFO is at 1.18 per share and this is the real return you can focus on as an owner of the real estate.

So, if we look just at FFO, then the 1.18 EUR per share would give you an 8% investment return which is a pretty good return for real estate. But, things have to return to normal first.

The company has benefited enormously form lower interest rates in Europe over the past years as lower rates increase real estate values and increase the spread between the rental yield and the financing costs.

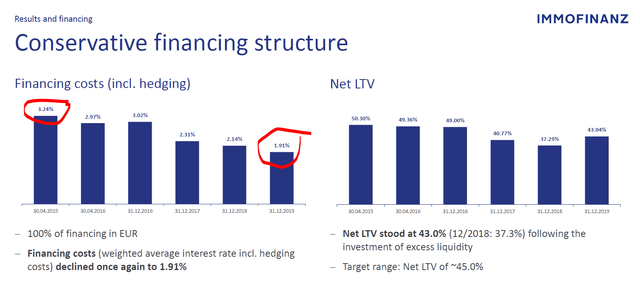

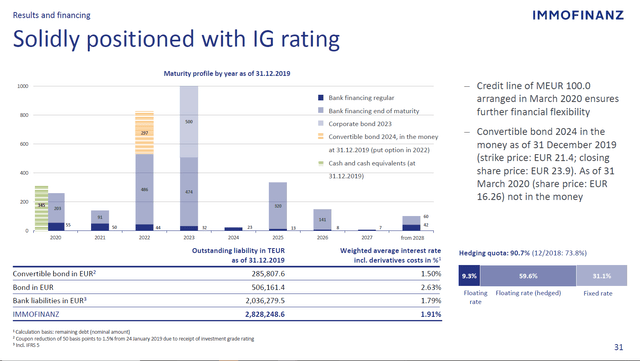

If interest rates increase for the real estate sector, things could get ugly because the company has 2.8 billion EUR in debt.

The debt is not an issue when things go well, but when things get difficult debt quickly backfires. Recently the company had to dilute shareholders by issuing shares at a price of 15.5 EUR and also issuing a convertible bond to improve the capital structure in relation to the COVID-19 impact. Such activities tell me this is a leveraged play on real estate which means you need to know when to buy and when to sell. It is not really a SWAN (sleep well at night) real estate investment.

Also, rents were differed in April and the negotiations with retailers will be tough going forward as their business model will be severely hit, both of the retailers and Immofinanz.

Immofinanz dividend and investment thesis

The company’s goal is to distribute 75% of FFO as dividends which gives you the above mentioned yield of 5.9%. However, the dividend has been delayed until they see the consequences of COVID-19.

The last dividend in 2019 was 0.85 EUR per share and if things stabilize, one could expect a similar payment in the future. But, the longer it takes for things to stabilize, the higher will be the risk for the business related to real estate exposure, economic exposure etc.

Also, with less than 30% of properties in Austria and Germany and 70% in Eastern European countries, the risk is a bit higher because you never know how will things look like there over time. Plus, competition is high, things change fast and there is little stability for retailers. I come from an Eastern European country and these shopping centres grow like mushrooms and have actually a life span because customers quickly turn for the new venue. Something I don’t like when it comes to investing.

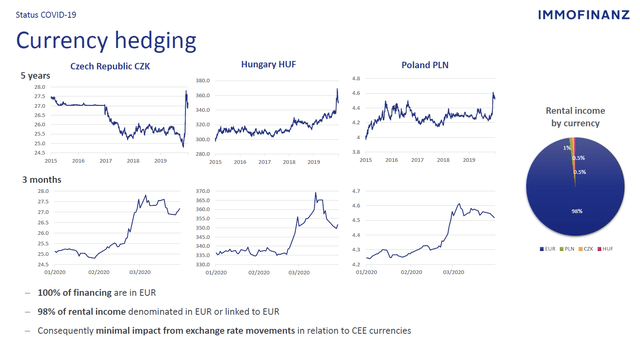

They also say there is limited impact from currencies, but that might be the case for the year you have hedged yourself, but the customer certainly didn’t hedge himself and will have less purchasing power if from countries with weaker currencies.

Immofinanz stock analysis – Source: Immofinanz AG Investor Relations

I’ll stop writing now as it is clear I don’t like Immofinanz stock as an investment because it is too risky. If you are an Immofinanz AG shareholder I hope I have given you some insights that will help you when making a decision on whether to keep the stock or not. Investment results will depend on the negotiations with retailers and on when things will, if ever, return to normal. With real estate, especially in Europe with negative population trends, the situation will remain tricky so expect volatility depending on the economic situation in Eastern Europe, sentiment towards related investments and on the positive side; inflationary impacts and real asset protection values (perhaps better to be looked for with companies that offer everlasting value).

An idea of a simpler European real estate investment stock focused on homes in Linz is Athos Immobilien.

Don’t forget to subscribe to my newsletter to get more such analyses directly in your inbox.