January 24, 2025

How To Calculate Intrinsic Value

(this article is part of the free value investing course by Sven Carlin, check it out) In this crazy world... Continue reading

November 22, 2024

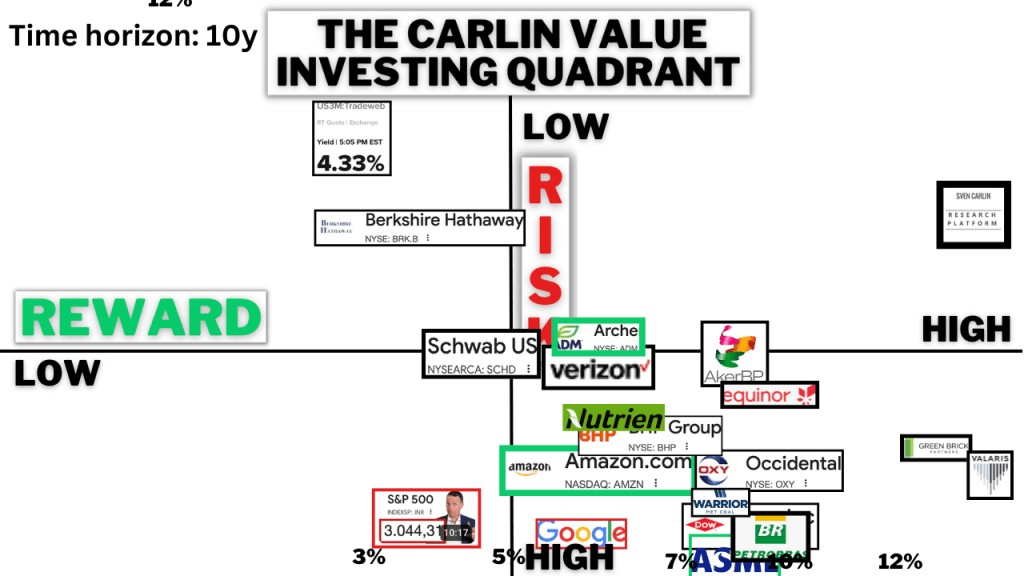

The Value Investing Risk & Reward Quadrant by Sven Carlin

The core of value investing is taking advantage of market irrationalities by finding low risk and high reward investing opportunities.... Continue reading

June 10, 2026

MercadoLibre: Analyzing the “Amazon of Latin America”

MercadoLibre, a leading e-commerce and fintech system in Latin America, has established a formidable presence, effectively functioning as a combined... Continue reading

PDD Holdings: Assessing Potential and Risks in the Competitive E-Commerce Landscape

Understanding the Business Model PDD Holdings is essentially a dual-pronged business, operating as one of China's most prominent discount aggregate... Continue reading

June 9, 2026

Charter Communications: A Deep Dive into an Extreme Asymmetric Opportunity

Charter Communications presents a complex, high-stakes scenario that I have been monitoring closely as the stock has pulled back from... Continue reading

The Paradox of All-Time Highs: Analyzing the Potential for a Market Bubble

In the current financial landscape, the stock market has reached all-time highs, prompting a critical question: is this the greatest... Continue reading

June 3, 2026

Evaluating Your Broker: Why I Consider Interactive Brokers the Standard for Value Investors

After spending over 25 years in the investing landscape and navigating the complexities of various platforms, I have frequently been... Continue reading

September 11, 2025

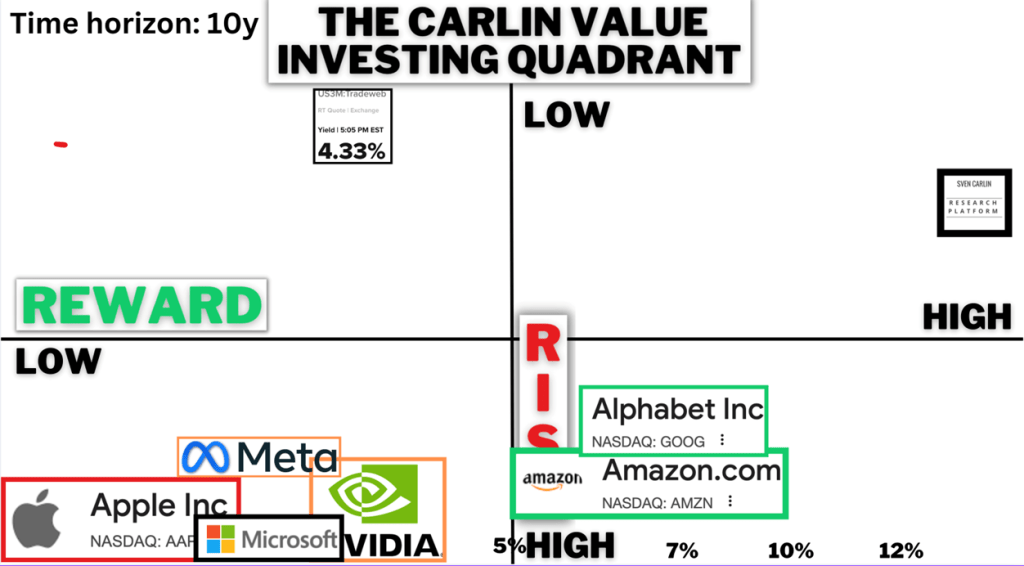

September Value Investing Quadrant: A Deep Dive into Risk and Reward

Check the full Value Quadrant video here: https://youtu.be/2wro11eb3d8 The essence of value investing lies in carefully weighing risk against reward.... Continue reading

Lululemon vs. Nike: Which Stock Offers Better Long-Term Value?

You can watch the full video discussing Lululemon and NIKE here: https://youtu.be/stbXSx0hNKA Investor interest in athletic apparel has surged in... Continue reading

Berkshire Hathaway (BRK) Is Not a Buy at Current Levels

You can watch the full video discussing BRK stock here: https://youtu.be/hmEWuCkqI7c For decades, Berkshire Hathaway has stood as the gold... Continue reading

Aker BP: A Compelling Case for Income Investors Seeking Stability in the Volatile Oil Sector

You can watch the full video discussing Aker BP here: https://youtu.be/7tsUlR4kXLA The global energy landscape remains as unpredictable as ever,... Continue reading

Green Brick Partners: A Compelling Value Investment in Homebuilding

Here is the full video discussing Green Brick Partners if you want a more in depth analysis: https://youtu.be/HIdYkW9vu2Q The search... Continue reading

Reinet Investments: A Value Trap or a Hidden Gem?

If you want to watch an in-depth video discussing Aker BP, you can watch it here: https://youtu.be/p-BRu2qA_n0 Holding companies have... Continue reading

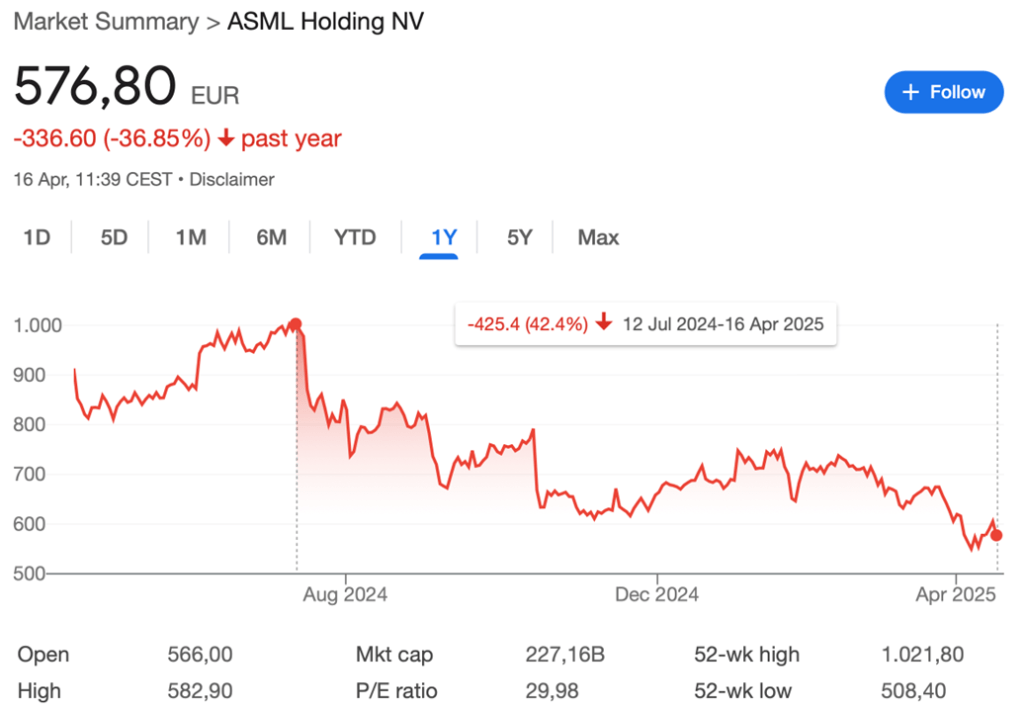

ASML Earnings Analysis: Navigating Short-Term Uncertainty for Long-Term Value

If you want an in depth video explaining ASML, you can watch it here: https://youtu.be/tCKEs68u2bc The recent earnings report from... Continue reading