June 10, 2026

MercadoLibre: Analyzing the “Amazon of Latin America”

MercadoLibre, a leading e-commerce and fintech system in Latin America, has established a formidable presence, effectively functioning as a combined... Continue reading

PDD Holdings: Assessing Potential and Risks in the Competitive E-Commerce Landscape

Understanding the Business Model PDD Holdings is essentially a dual-pronged business, operating as one of China's most prominent discount aggregate... Continue reading

June 9, 2026

Charter Communications: A Deep Dive into an Extreme Asymmetric Opportunity

Charter Communications presents a complex, high-stakes scenario that I have been monitoring closely as the stock has pulled back from... Continue reading

The Paradox of All-Time Highs: Analyzing the Potential for a Market Bubble

In the current financial landscape, the stock market has reached all-time highs, prompting a critical question: is this the greatest... Continue reading

June 3, 2026

Evaluating Your Broker: Why I Consider Interactive Brokers the Standard for Value Investors

After spending over 25 years in the investing landscape and navigating the complexities of various platforms, I have frequently been... Continue reading

September 11, 2025

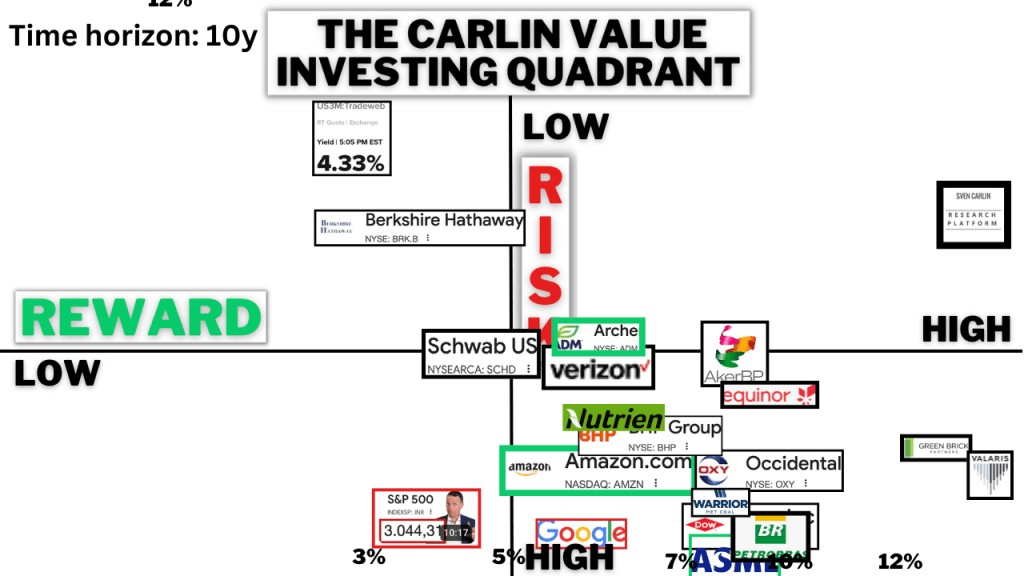

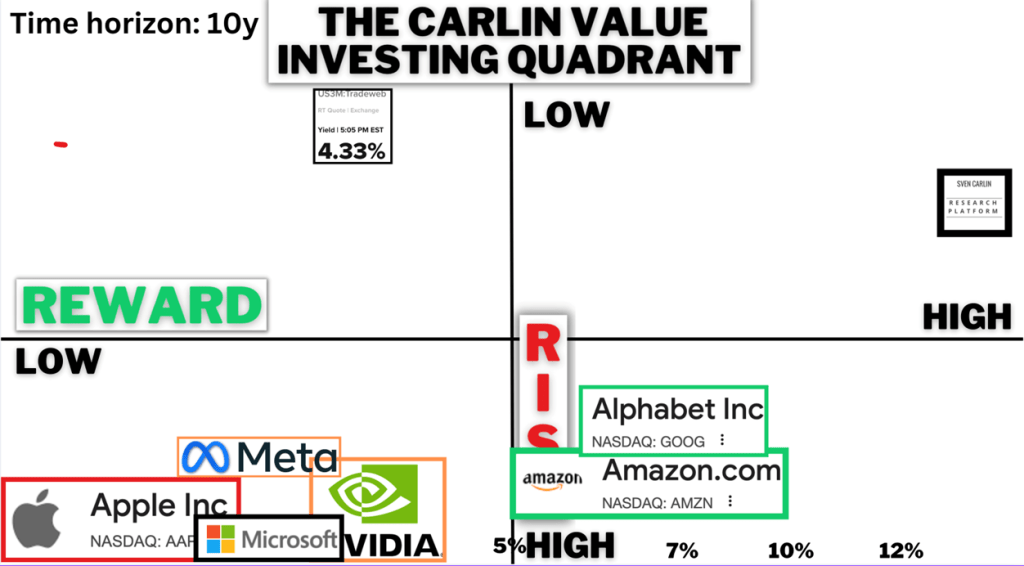

September Value Investing Quadrant: A Deep Dive into Risk and Reward

Check the full Value Quadrant video here: https://youtu.be/2wro11eb3d8 The essence of value investing lies in carefully weighing risk against reward.... Continue reading

Lululemon vs. Nike: Which Stock Offers Better Long-Term Value?

You can watch the full video discussing Lululemon and NIKE here: https://youtu.be/stbXSx0hNKA Investor interest in athletic apparel has surged in... Continue reading

Berkshire Hathaway (BRK) Is Not a Buy at Current Levels

You can watch the full video discussing BRK stock here: https://youtu.be/hmEWuCkqI7c For decades, Berkshire Hathaway has stood as the gold... Continue reading

Aker BP: A Compelling Case for Income Investors Seeking Stability in the Volatile Oil Sector

You can watch the full video discussing Aker BP here: https://youtu.be/7tsUlR4kXLA The global energy landscape remains as unpredictable as ever,... Continue reading

Green Brick Partners: A Compelling Value Investment in Homebuilding

Here is the full video discussing Green Brick Partners if you want a more in depth analysis: https://youtu.be/HIdYkW9vu2Q The search... Continue reading