February 21, 2025

Value Investing: A Strategic Approach to Building a $100,000 Portfolio

What is Value Investing?The Key Drivers of Value Investment ReturnsBuilding a $100,000 Value Portfolio1. U.S. Treasuries (Low Risk)2. Berkshire Hathaway... Continue reading

February 10, 2025

How to Allocate Your Portfolio: A Framework for Investors

ContentsThe Role of Diversification: Knowledge MattersA Practical Framework for Portfolio AllocationKey Drivers of Allocation DecisionsReal-World Examples: What I Own and... Continue reading

July 14, 2021

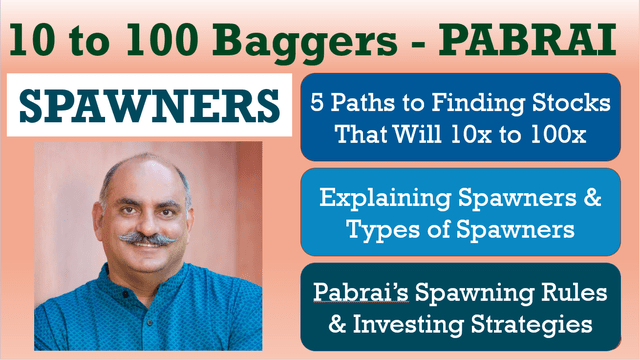

Mohnish Pabrai’s Spawner Stocks Framework – How To Find 10 to 100 Bagger Stocks

This is a deep dive into the Spawning Investing Strategy recently discussed by Mohnish Pabrai. As investing is always a... Continue reading

November 14, 2020

Is Value Investing, Dead Or Alive, Something For You?

There is a plethora of articles and videos attacking value investing, discussing whether it is dead, detrimental, whether people like... Continue reading

November 7, 2020

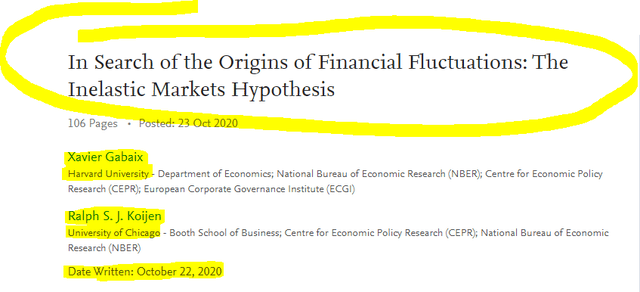

Inelastic Market Hypothesis – You Crash Markets

Who Moves Stock Prices? You Do! Inelastic Market Hypothesis Explains Market Volatility. Here is the less technical video, article explaining... Continue reading

October 22, 2020

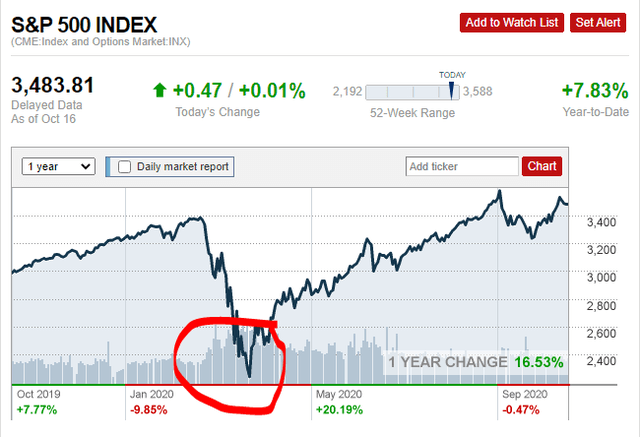

Don’t Fear A Market Crash, Fear An Investing Tragedy (4 Strategies to Avoid it)

One of the biggest fears investors have is a stock market crash (SPY). Nobody likes to see the value of... Continue reading

October 14, 2020

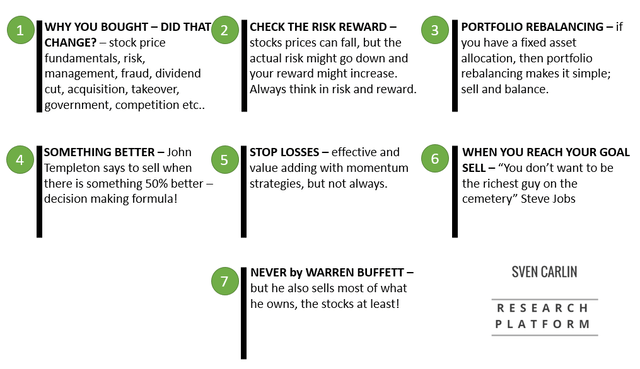

When To Sell A Stock – 7 Strategies (20% Portfolio Stock Sale Practical Example)

When to sell a stock – the hardest part of investing I’ve recently sold a stock that made 20% of... Continue reading

May 16, 2020

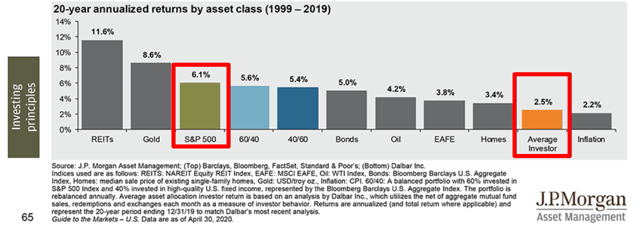

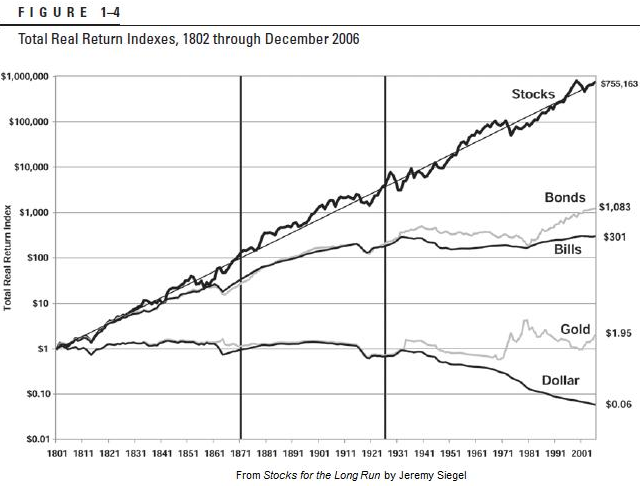

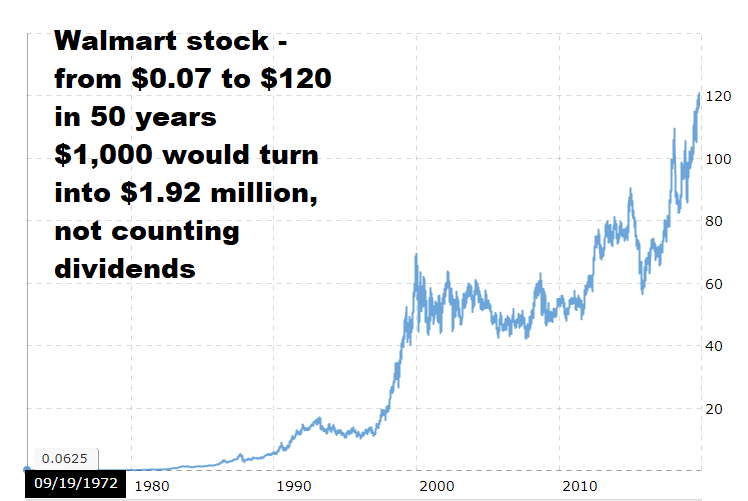

Stocks Crash 70% And 76% Will Underperform – Can You Handle That?

Stocks crash and stock markets too Before investing, you must know that stocks can crash 70% anytime and 50% of... Continue reading

January 22, 2020

“Cash is trash” – You Shouldn’t Own Cash For Long

At the recent World Economic Forum in Davos, Ray Dalio, manager at the largest hedge fund in the world, Bridgewater... Continue reading

December 6, 2019

Small Cap Stocks Explained – Index/ETFs, Risk/Reward and Best Small Cap Investing Strategy (hint – Peter Lynch)

Small Cap Stocks Investing - Introduction I have recently analysed the complete FTSE Small Cap Stock Index. The FTSE SmallCap... Continue reading