April 4, 2025

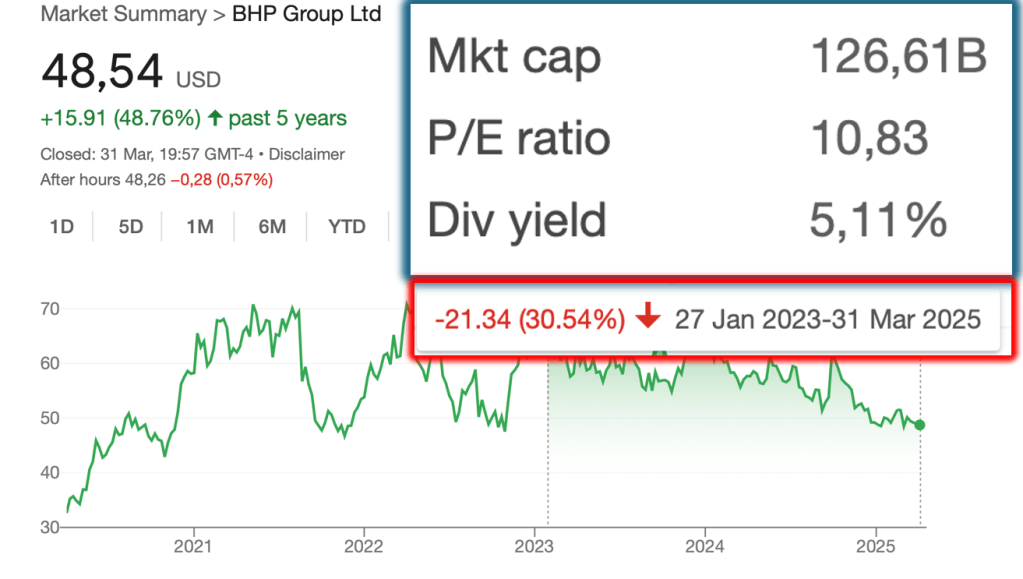

BHP Group: A High-Quality Cyclical Play in the Commodities Sector

If you want an in-depth video about BHP, you can watch it here: https://youtu.be/9Y7LbEoYWp0 BHP Group (ASX: BHP, NYSE: BHP),... Continue reading

April 1, 2025

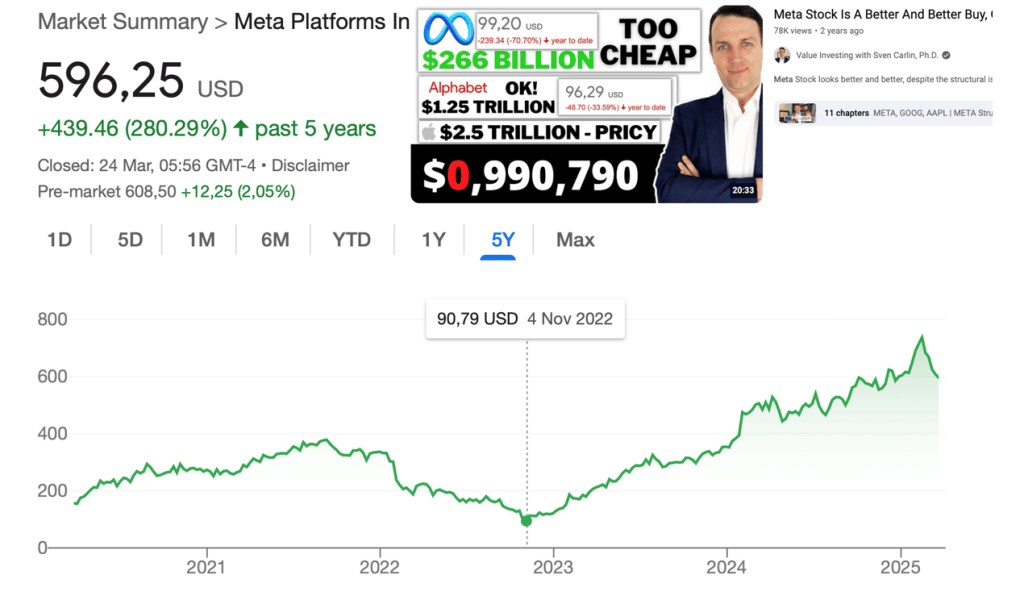

Meta Platforms: A Comprehensive Analysis of a Tech Titan at a Crossroads

If you want a deep dive into Meta stock, watch the full video about the Magnificent 7 Stocks: https://youtu.be/AgnNJUoXqdU Meta... Continue reading

Amazon Stock: A Comprehensive Analysis of Growth Trajectory and Investment Considerations

If you want a deep dive into Amazon stock, watch the full video about the Magnificent 7 Stocks: https://youtu.be/AgnNJUoXqdU As... Continue reading

NVIDIA: A Deep Dive into the AI Juggernaut’s Valuation and Future Prospects

If you want a deep dive into Nvidia stock, watch the full video about the Magnificent 7 Stocks: https://youtu.be/AgnNJUoXqdU The... Continue reading

Apple Stock: A Comprehensive Look at Its Valuation and Future Prospects

If you want a deep dive into Apple stock, watch the full video about the Magnificent 7 Stocks: https://youtu.be/AgnNJUoXqdU Apple... Continue reading

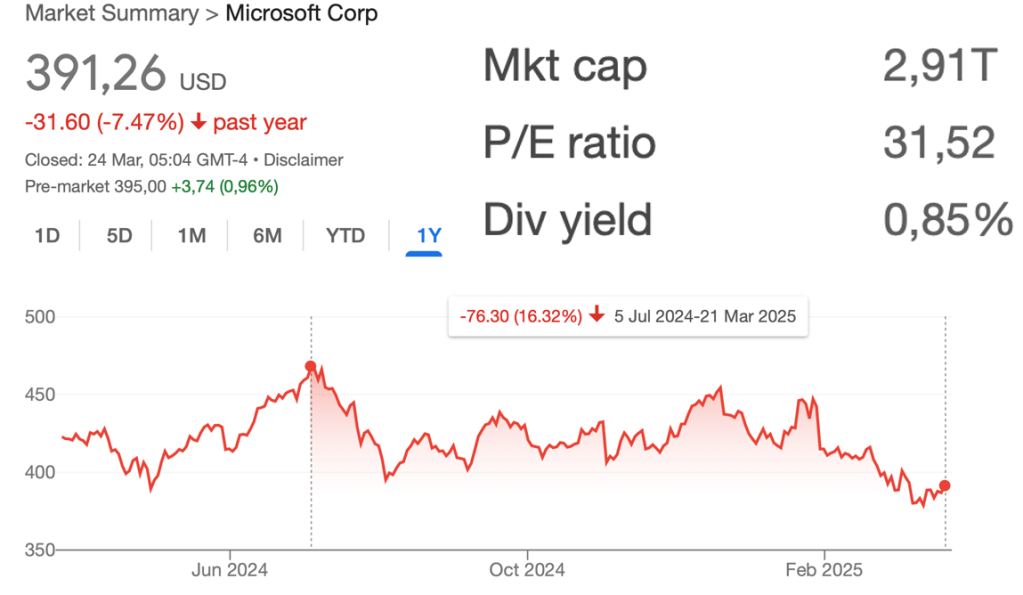

Microsoft Stock: A Comprehensive Analysis of Growth Prospects and Valuation Concerns

If you want a deep dive into Microsoft stock, watch the full video about the Magnificent 7 Stocks: https://youtu.be/AgnNJUoXqdU As... Continue reading

March 20, 2025

HP Inc. (HPQ) and Hewlett Packard Enterprise (HPE): A Comprehensive Analysis of Challenges, Opportunities, and Investment Prospects

In the ever-evolving technology sector, Hewlett Packard Enterprise (HPE) and HP Inc. (HPQ) have long been stalwarts, but recent market... Continue reading

Interactive Brokers: A Strong Broker and Stock, but What’s Next After a 31% Decline?

Interactive Brokers (IBKR) has long been regarded as one of the most innovative and cost-effective brokerage platforms in the financial... Continue reading

March 7, 2025

High-Yield Dividend Chemical Stocks: Are Dow, BASF, and LyondellBasell Worth the Risk?

Check out the full video on YouTube, if you prefer reading however, keep scrolling. https://youtu.be/EeKhMJyO20k The chemical industry has long... Continue reading

The Enduring Appeal of S&P Global: A Deep Dive into a “Wonderful Business”

In the world of investing, few businesses stand out as consistently exceptional. S&P Global (SPG) is one such company, a... Continue reading