February 10, 2025

Understanding the Intrinsic Value of the S&P 500: A Guide for Investors

Contents:What is Intrinsic Value?Key Inputs for Calculating Intrinsic ValueAnalyzing S&P 500 Earnings and DividendsEstimating Earnings GrowthValuation and Expected ReturnsRisk and... Continue reading

May 23, 2021

FAQ – Stock Market Research Platform

I’ll try to summarize the most common questions I get about the Research Platform here, so, let’s start. Here is... Continue reading

November 7, 2020

Inelastic Market Hypothesis – You Crash Markets

Who Moves Stock Prices? You Do! Inelastic Market Hypothesis Explains Market Volatility. Here is the less technical video, article explaining... Continue reading

October 22, 2020

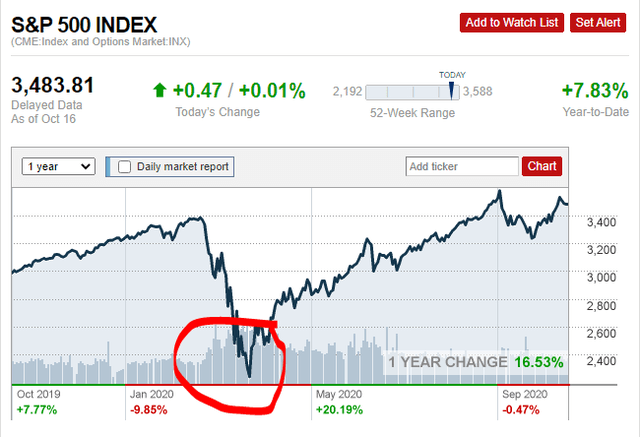

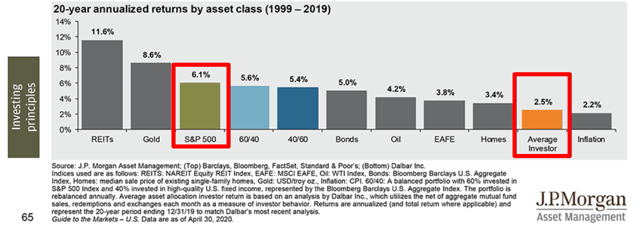

Don’t Fear A Market Crash, Fear An Investing Tragedy (4 Strategies to Avoid it)

One of the biggest fears investors have is a stock market crash (SPY). Nobody likes to see the value of... Continue reading

May 16, 2020

Stocks Crash 70% And 76% Will Underperform – Can You Handle That?

Stocks crash and stock markets too Before investing, you must know that stocks can crash 70% anytime and 50% of... Continue reading

November 28, 2019

Next Recession – Stocks Will Likely Go UP!

The Next Recession This article is an excerpt from a comprehensive economic report for investors that can be found here: Comprehensive... Continue reading

Economic Crisis – The $246.5 Trillion Global Debt Mountain Will Not Lead To A Economic Crisis (Just A Currency Crisis)

The Global Economy is Full of DEBT This article is an excerpt from a comprehensive economic report for investors that... Continue reading

September 27, 2019

Stock Market Crash And Recession Strategy That Always Works

“Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.” Peter Lynch There is so... Continue reading

September 15, 2019

INDEX FUNDS Investing – NEXT Market CRASH WILL BE UGLY

Mortgage crisis Dr. Burry - Compares Index funds to subprime bubble! Dr. Michael Burry, famous for predicting the subprime mortgage... Continue reading

June 18, 2019

How To Invest $1000 – 6 Rules For Investing Your First 1000 Dollars

Before discussing the 7 rules to follow when investing $1000 and an example of where I am investing my $1000s,... Continue reading