Fagron Stock Analysis (Balance Sheet Risks)

This Fagron stock analysis (AMS: FAGR) is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As.

Fagron Stock Price Overview

Fagron stock, FAGR stock, hasn’t done much over the last 15 years. There has been a boom in the 2014 to 2016 period but it was followed by a big drop. Such big drops have to be investigated because those tell you a lot about the value creation and the management – was it a spinoff or it was just a bad business decision? In Fagron’s case it was a business issue with an impairment of € 225.6 million related to Bellevue Pharmacy and Freedom with consequently having financing issues.

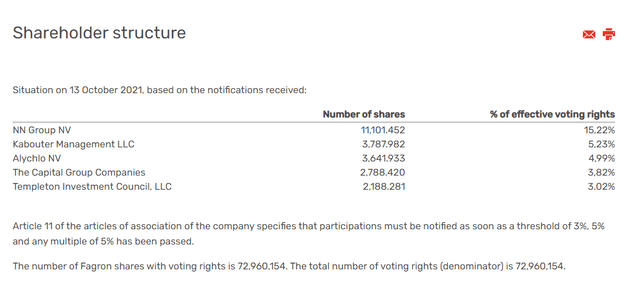

The market cap is currently 1.09 billion EUR and FAGR stock is available on Euronext exchanges. The owners are diversified and NN Group NV is the largest owner with 15.22%.

Fagron Stock Analysis – Business Overview

Fagron NV (name: FArmaceutische GRONdstoffen – eng. Pharmaceutical commodities) is multinational group of companies founded in 1990, governed by Belgian law registered in Belgium, and its headquarters are located at Rotterdam, the Netherlands.

Its business is pharmaceutical compounding where it brings customized pharmaceutical care to hospitals, pharmacies, clinics and patients in 35 countries worldwide. It supplies pharmaceutical care to hospitals, pharmacies, clinics, and patients also producing pharmaceutical raw materials, equipment, and supplies needed to prepare medications.

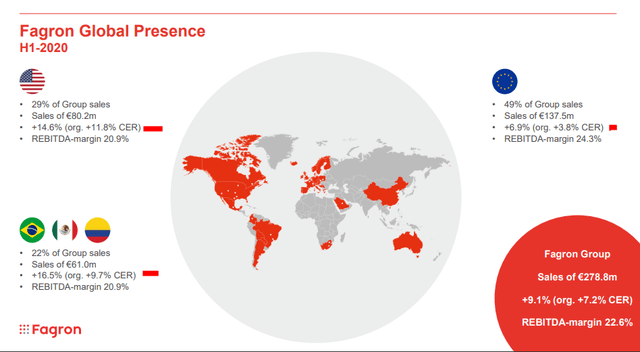

Half of the sales come from Europe but global sales are growing significantly.

Fagron business strategy:

Fagron Stock Analysis – Financials

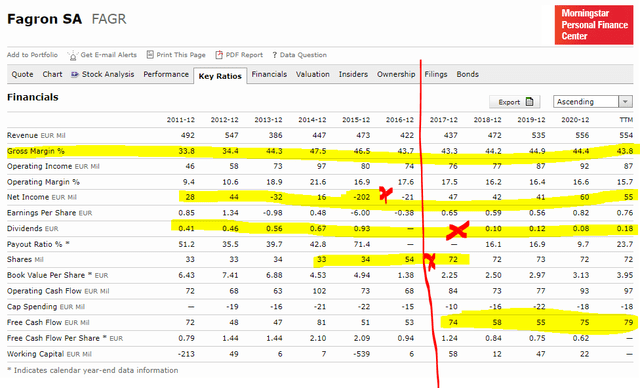

Apart from the 2015 fiasco that almost sent the company bust where it needed to double the number of shares issued to cover for capital needs and survive, all other metrics look ok.

Revenue growth has been slow and steady over the last few years, margins have been stable albeit operating margins have declined a bit. The dividend had been cut in 2015 but reintroduced and slowly increased since. The free cash flow is around 75 million EUR per year leading to a 7% FCF yield.

Thus, from a profitability perspective there is nothing wrong with the business. However, the balance sheet doesn’t look as good.

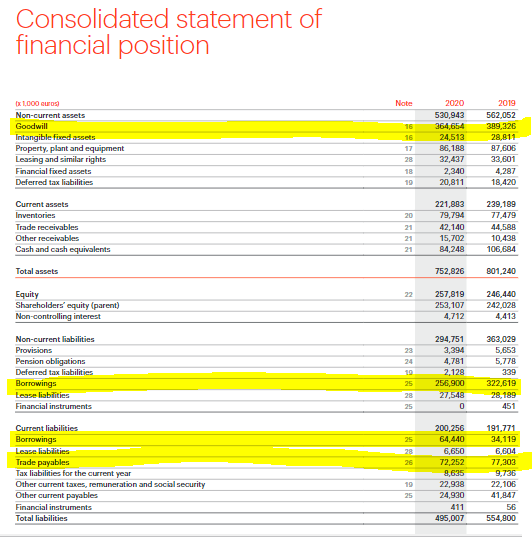

Shareholder equity is 60% of goodwill. This means that there is absolutely no tangible shareholder’s equity and all the equity is present on the balance sheet just because the company considered it ok to pay a certain amount for other companies. Equity is 246 million EUR on 364 of goodwill. You never know if there will be another impairment ahead that wipes out shareholder’s value.

Borrowings are also pretty high, 320 million EUR on 75 million in FCF is a bit risky for my taste. Given the company doesn’t have anything special that will allow for quick debt servicing or higher FCF, I would consider Fagron stock relatively risky from a balance sheet perspective. Also, trade payables are higher than trade receivables, so the company is practically financing customers which is again not really a positive.

Fagron Stock Analysis – Investment Conclusion

Fagron stock is trading at a 14.75 free cash flow valuation while carrying significant balance sheet and business risk. Given the current financial environment, it might not be extremely risky but we as value investors can find better.