Akzo Nobel Stock Analysis – Stock Price Going Up Thanks To Buybacks

This Akzo Nobel stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As.

Akzo Nobel stock price overview – AMS: AKZA – OTC: AKZOY

A look at the Akzo Nobel stock price chart tells us how the stock is a steady growth stock exposed to cyclical trends. This means that there might be cyclical situations creating interesting buying opportunities because the underlying growth trend gives you a margin of safety over the cyclical concerns.

The market capitalization is 19,48 billion EUR, the PE ratio is high at 26.57 from an absolute perspective and consequently the dividend yield is low at 1.91%. But it is always good to take a look at such businesses even if maybe it isn’t a great investment at current levels, it is certainly good to have the analysis done to catch those opportunities that come every few years as we see in the chart above.

But, let me tell you immediately, all things equal, Akzo Nobel’s stock price will go up 25% over the coming 12 months.

Let’s make a quick business overview, analyse the financials, make a comparative stock valuation and conclude with the investment thesis and then you will see whether the situation fits your investment requirements.

Akzo Nobel stock analysis – business overview

Akzo Nobel is in the business of paint and coatings. If you ever painted your home, you should be familiar with some of the brands below which are just part of the whole brand list owned by Akzo Nobel. (when refurbishing my first home years ago, I used Flexa and it was worth it from an investment perspective)

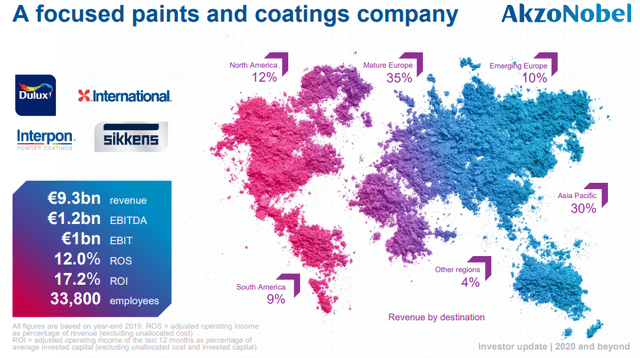

Sales mostly come from Europe but the business is well diversified across the globe with a strong Asia Pacific focus.

They have approximately 9% of the market.

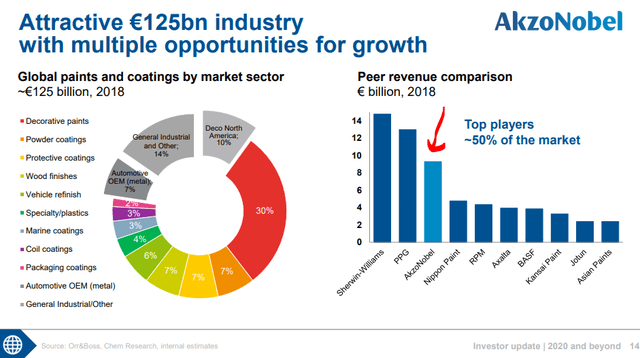

As we can see above, the market is pretty segmented which offers opportunities for growth through consolidation and scale advantages. The growth of the market is not that fast and we can assume it will be in line with global economic growth.

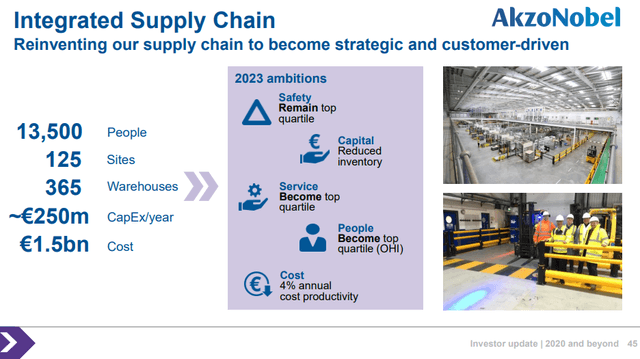

Within a slow growth business environment, it is all about increasing profitability over time and one way is to integrate the supply chain if that is cheaper and actually increases margins.

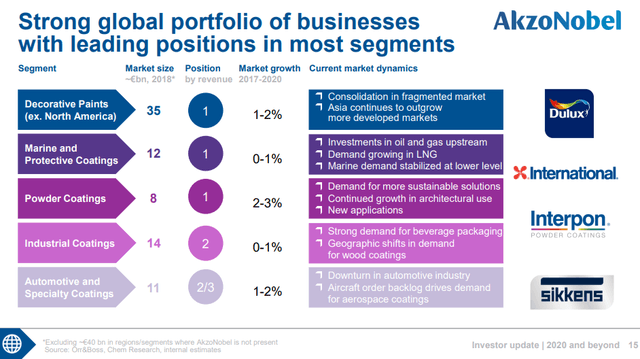

The following chart summarizes things from both a strategic and financial perspective and is a great introduction into the next chapter – financials.

Let’s take a look at the financials before taking a look at dividends and making a valuation.

Akzo Nobel stock analysis – financials

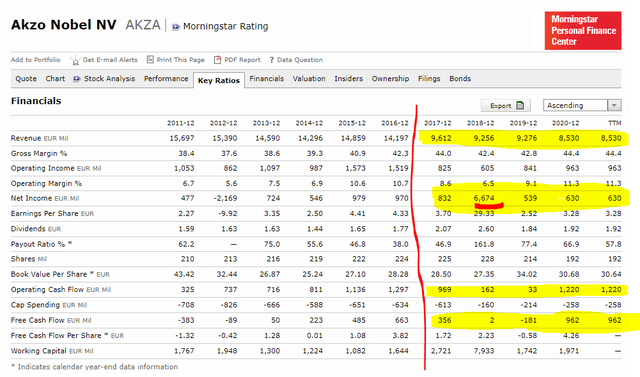

Akzo sold its chemical segment in 2017 for 12 billion EUR so the financials below have to be adjusted. Despite that, revenues have slowly been declining but gross margins have been improving and at 44% lately while operating margins went up to 11.3%.

It is key to understand the fluctuation in those margins across cycles. When business is slow margins fall and so do earnings. Earnings per share fluctuated between 2.5 EUR to 4.41 EUR over the last 10 years.

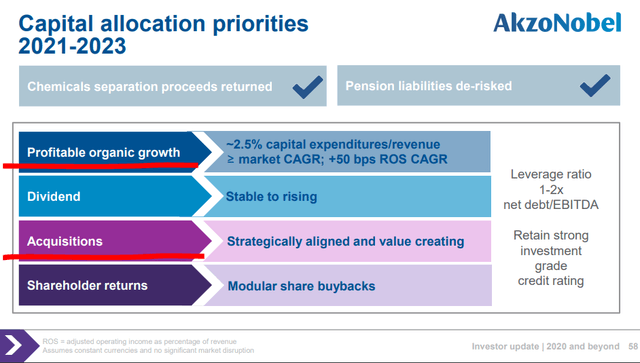

Their target is to keep investment grade status with debt to EBITDA between 1 and 2.

What often happens is that the company makes an acquisition, pushes the ratio up to 2, then the cycle turns and you have financing issues which explain the few, but big, declines in the stock price we have seen over the last 25 years. That might be the time to buy.

Akzo Nobel dividend and buybacks

As seen above, Akzo’s goal is to have a steady or rising dividend alongside doing buybacks. I usually disagree with a pre-set buyback strategy because the reward for shareholders is much different if you do buybacks at a price of 50 EUR where the stock was in March of 2020 or above 100 where the stock is now. But, ok, their choice, and their choice is to spend 1 billion EUR on buybacks over the coming 12 months, no matter the stock price.

Just look above for the number of shares outstanding and below at the stock price. When the stock price was around 80 over 2019, they lowered the number of shares by 50 million or 20%. When the stock price crashed in March 2020, creating an amazing buyback opportunity, they bought back just 5 million shares. A perfect example of how management is idiotic about buybacks.

But ok, it is what it is and we can only accept it and actually it will be beneficial to those that wish to see the price of the stock go up. It is so hard to argue with that, but that they could do better in rewarding shareholders, yes.

Spending 1 billion EUR on buybacks implies a 5% buyback yield alongside likely pushing the stock price higher given they are buying back a lot. If we apply the inelastic market hypothesis developed by professors Gabaix from Harvard and Koijen from Chicago Booth, the 1 billion EUR buyback should increase the market capitalization by 5 billion EUR at least. So, the stock price is most likely to go up over the next 12 months if there are no surprises. We have already seen the stock jumping on the announcement, but buybacks might push it higher.

Less shares outstanding, also push the dividend per share up.

While you wait for the stock price to increase, you also get a dividend of around 2 EUR per share that is expected to grow in line with the lower number of shares outstanding.

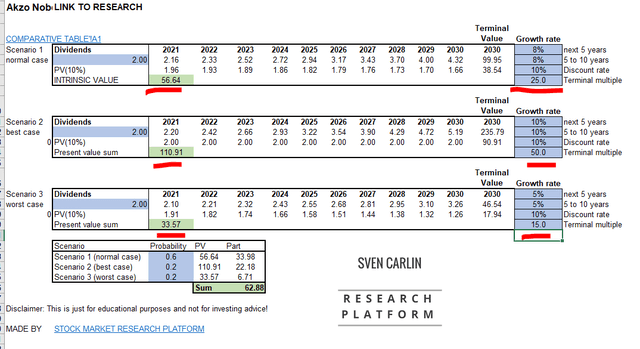

Akzo Nobel stock valuation

I have used the dividend to make a valuation of Akzo Nobel stock. Assuming a dividend growth rate of 8%, that includes the organic business growth and buyback effect, a 10% required return rate and a 4% terminal dividend yield, the intrinsic value of Akzo Nobel stock is 56 EUR.

Akzo Nobel stock valuation – Source: Sven Carlin Research Platform – free template download alongside comparative list

In an exuberant scenario, where the dividend yield grows 10% per year and the market is still happy with a dividend yield of just 2% in 2030, then the stock is fairly priced now.

In a negative scenario, which can happen especially if interest rates go up, where the market expects a dividend yield of 6.66% in 10 years, the intrinsic value would be just 33 EUR.

Akzo Nobel stock investment discussion

The question now is what do you invest for? If you are looking for the stock to go up over the coming 6 to 12 months thanks to the buybacks, it might be interesting to own Akzo Nobel or to play with options.

However, from an investing perspective, a dividend yield of 2% is not attractive when you know what can happen when things turn bad and we have seen that sooner or later things do turn negative.

On the other hand, when the cycle downturn passes, we are looking at a good, slow growth cyclical business that should be purchased in cycle downturns. I am going to put Akzo Nobel stock on my comparative stock list and then see whether the stock will ever come to a level when the risk is low and the return the highest. For me personally holding a cyclical with a 2% yield with the possibility of seeing it go up another 20% is too much risk because I don’t want to be on the other side of things when things turn bad.

If you like a value oriented, business focused investing approach, please consider subscribing.

About the author: Sven Carlin Ph.D. is a dedicated investing educator and stock market researcher focused on finding investment opportunities with a value investing perspective. His research is summarized on the Sven Carlin Research Platform where he covers many stocks and shows his portfolios. The educational part is shared on YouTube and the Free Stock Market Investing Course.