Accell Stock Analysis – Good Business But Difficult Sector

This Accell stock analysis is part of my full analysis of the stocks traded on the Amsterdam stock exchange. I am looking for future 10-baggers or more so the best way to find those is to look at smaller companies that have room to run. If you like to get updates on my research, please subscribe to my newsletter.

Accell’s market capitalization is 1,13 billion EUR which puts it into the small to medium cap range. (years ago, it was certainly medium cap, these days with all the crazy market capitalizations one might categorize it as small cap – how things change)

Accell Stock Price Overview – AMS: ACCEL

After the initial boom in the 2000s, Accell stock (AMS: ACCEL) showed characteristics of a slow growth business where the stock actually did nothing over 13 years.

Accell’s stock boomed after Covid when revenues were boosted by huge demand for bicycles which is what Accell does.

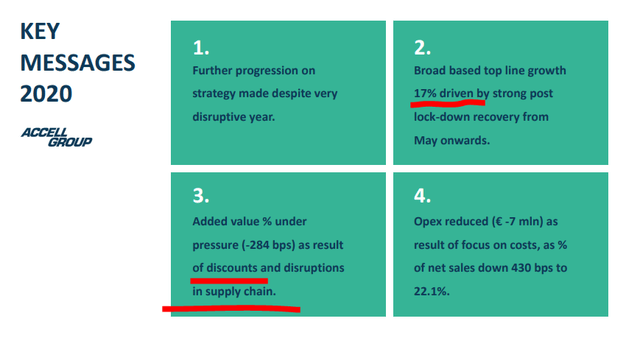

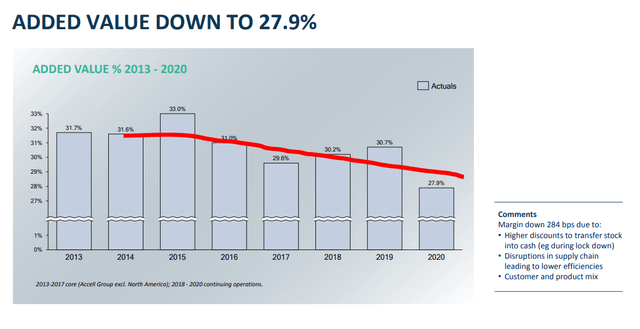

Top line growth was significant but not the added value.

Let’s take a quick look at the business and at the fundamentals to see whether there is investing value.

Accell Stock Analysis – Business Overview

Accell is a group owning various bicycle brands alongside producing parts and accessories for bikes.

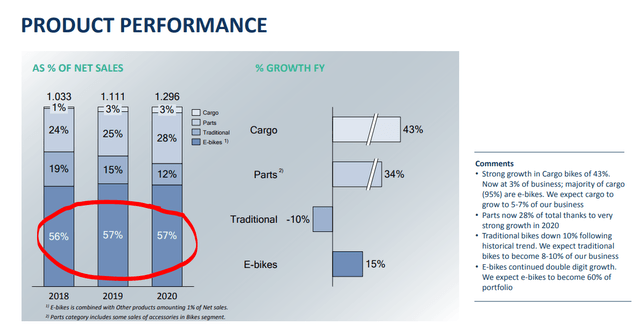

The group is focused on selling e-bikes and parts. 57% of revenues are from e-bike sales, 28% from parts, 12% from traditional bikes.

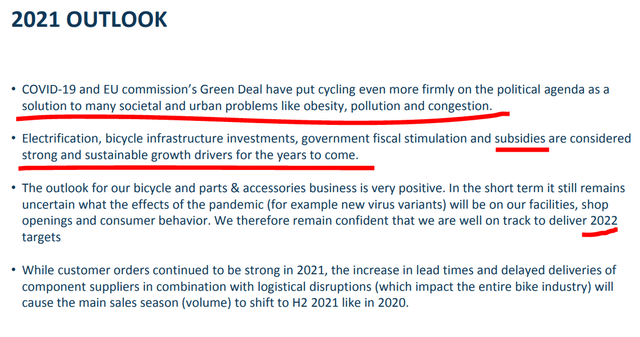

The business is exposed to current trends of e-mobility where there is also a political positive coming from subsidies.

Their strategy is rationalisation for more profitability and continuous growth.

Let’s take a look how the above reflects the financials.

Accell Stock Analysis – Financials

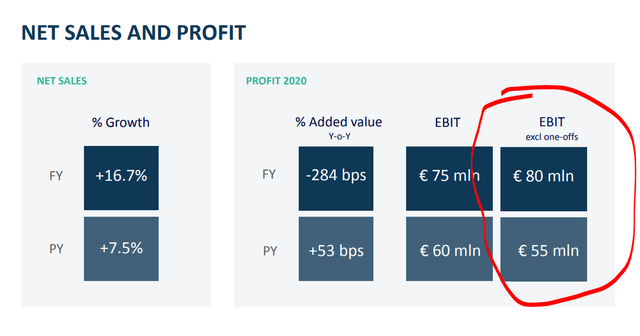

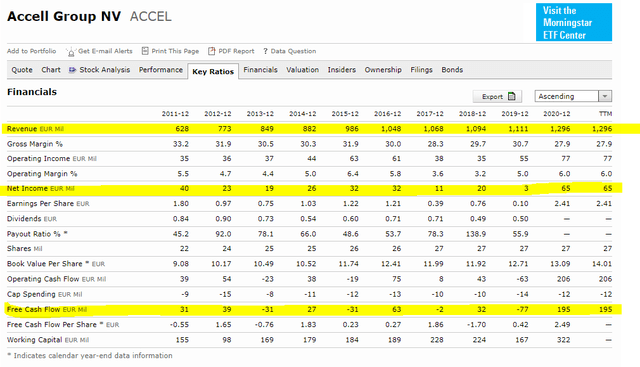

In a great year for bike makers like 2020, their EBIT has reached 80 million EUR. The question is what is next?

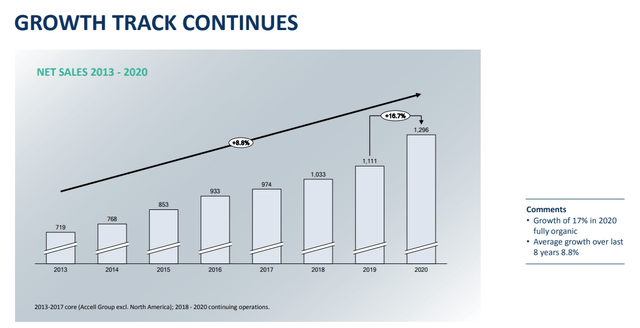

Over the past years, the company achieved a remarkable growth rate of 8%.

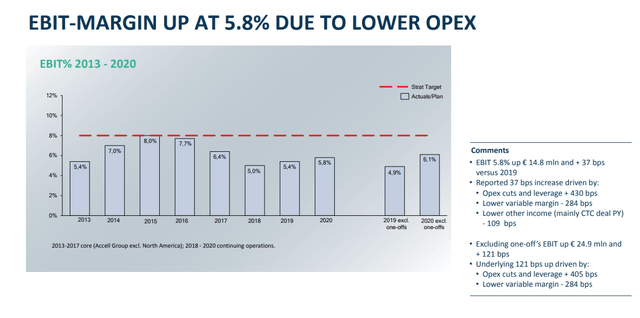

However, when it comes to margins, given that you don’t really have a moat within the bicycle industry, those have been declining.

Their actual margin target has been achieved only once in the last decade.

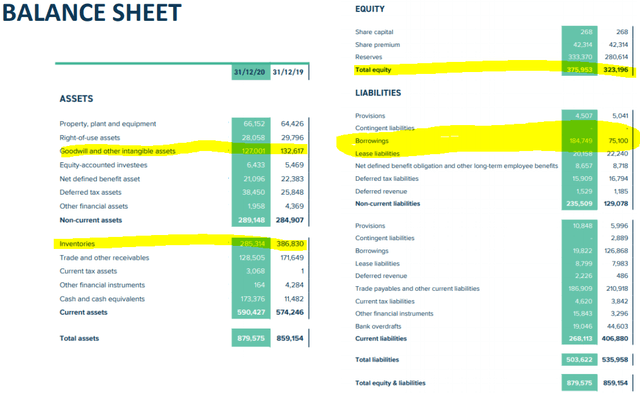

A look at the balance sheet tells us there are significant borrowings, also that the company is working on M&A to scale its business and goodwill is at 127 million EUR.

Net debt is just 72 million EUR and has been decreased in 2020 as they decreased working capital (inventories went down from 386 million EUR to 285 million EUR).

If I take a look at Accell’s long-term financials, except for the positive situation in 2020, I don’t really see much earnings power, certainly not enough to pay 1.13 billion EUR for which is the market capitalization. Actually, even the dividend has been declining in the past, despite the growth in sales.

Accell stock analysis – investing conclusion

If I think of the bicycle business, on one hand it is logical to grow through brand acquisitions, but on the other hand it is also risky given that it is very hard to get to a moat. I don’t fell the company can sustain its 15% required return on capital due to the simple high competitiveness of the business alongside clear market cycles as seen in the above long-term financial overview. Also, the key markets are Europe, where the demographics aren’t positive.

However, the current e-bike trend is certainly a tailwind, so they might do good for a while, but sooner or later it is going to get ugly. This is not a business nor a business sector I like from a fundamental long-term business investing perspective so I am not going to make a stock valuation like I usually do.

The stock might get hot thanks to the e-mobility trend, but I don’t invest in stocks, I like to consider myself as a business owner and Accell doesn’t fit those criteria.