ArcelorMittal Stock Analysis – Business Is Improving, Cash Flows Up

This ArcelorMittal stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger long-term investing potential, so as would Buffett say; I start with the As.

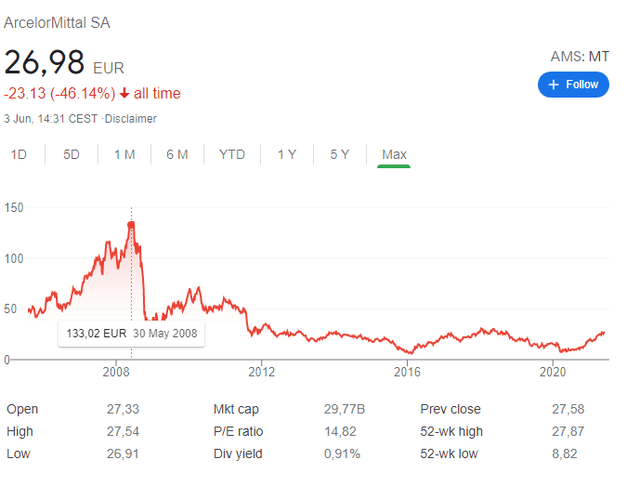

ArcelorMittal Stock Price Overview – NYSE:MT, AMS:MT

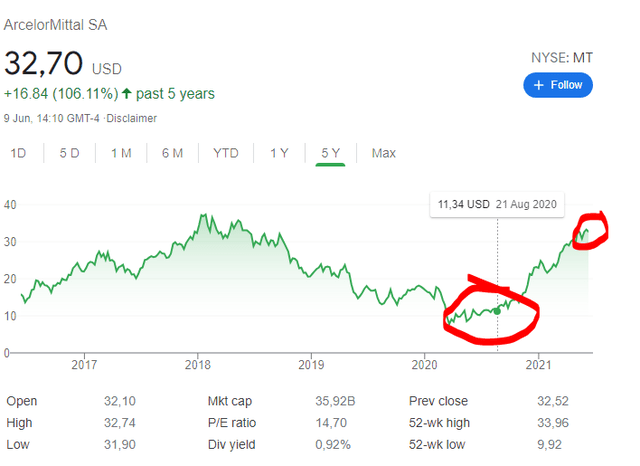

ArcelorMittal stock is a typical example of a cyclical stock. When things are good in the steel sector, the company makes a lot of money while when things turn bad, it gets very ugly for the sector and especially for shareholders.

Given that it is practically impossible to have a durable competitive advantage when it comes to steel, when prices are high, or better to say when spreads are high, as what matters is how much the company makes compared to the cost of inputs to make steel, companies have cash or expect good times to last forever, so they invest, which usually leads to oversupply, lower prices, i.e. lower spreads, and debt issues in the next economic downturn.

All of that is perfectly explained by the above MT stock chart. In the 2000s everything was booming on Chinese demand growth while after 2009 it was all downhill for the sector with some ups in 2010 and 2018 but it took more than a decade to digest all the investments made back then in exuberant times. However, after a decade of negative sentiment and low prices, the sun might shine again for steel producers, especially as governments push on infrastructure deals to keep their economies going forward.

MT’s market capitalization is 29 billion EUR, dividend yield 0.91% while the 52-week low was 8.82 EUR and we are currently trading around the high. I find ArcelorMittal stock an interesting one to follow the steel cycle and perhaps get an investing opportunity here or there over a decade. Steel is needed to make the world go round, so the demand will be there but it is key to buy cyclicals when things look bad or are starting to improve as Peter Lynch tells us.

ArcelorMittal Stock Analysis – Business Overview

ArcelorMittal is the largest steel producer in the world.

If you are the largest global producer, you are simply a price taker, if steel prices globally go up, MT will do good, if not, things will not be as good.

Steel prices are always volatile so you can expect the same with ArcelorMittal. Currently prices haven’t been this high for a decade and that is extremely beneficial for MT’s financials, however the question is how long can this last?

Steel prices have already declined a bit so we should not expect miracles, but still 2021 will be extremely good for ArcelorMittal.

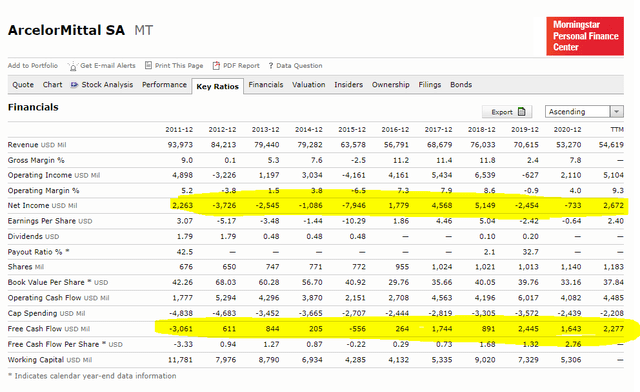

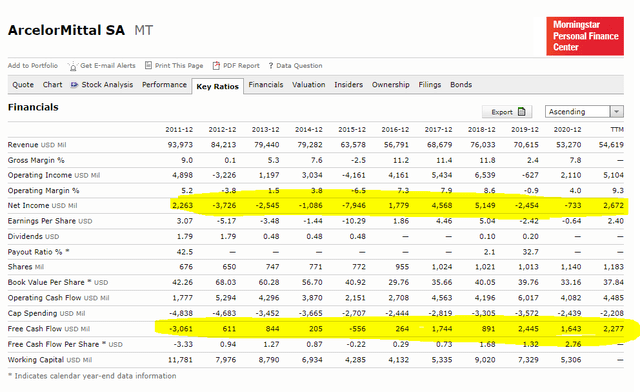

ArcelorMittal Stock Analysis Financials

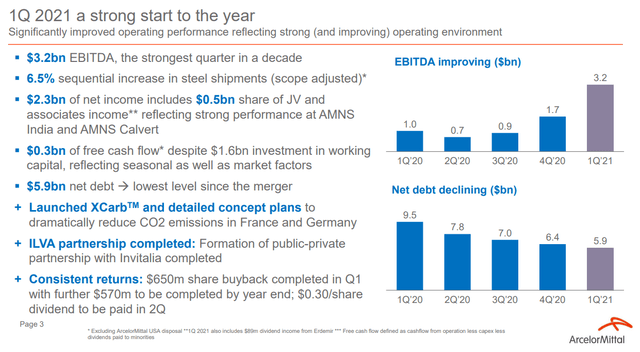

If we look at Q1 2021 and extrapolate for the whole year, the financials will look amazing.

EBITDA might reach $10 billion for 2021 but nobody knows how will the future look like after 2021. If prices go down, Auch, if not, MT will be printing cash. I wish I knew the future but the fact is nobody knows.

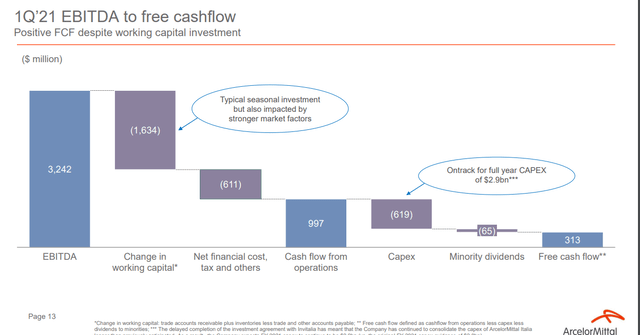

With cyclicals we have to keep in mind that when a business is going good, they need to up their working capital so you don’t see immediate improvements in the free cash flows as we see below. Q1 FCF is just $0.3 billion but working capital increased $1.6 billion.

On the other hand, when things get bad, companies can release their working capital and manage their cash flows.

Anyway, over the last decade the results have been extremely volatile but we have seen an improvement with the company over the last few years as they are lowering their costs and going away from the ‘scale at all costs’ strategy to a better, more conservative, let’s call it ‘higher quality/ higher margin strategy alongside more safety in cycle downturns’ strategy. Consequently, revenues have been declining as the company got rid of high costs assets and restructured but free cash flows went up and remained in the positive for the past years. This year things should look even better.

Better finances lead to better dividends and stronger buybacks.

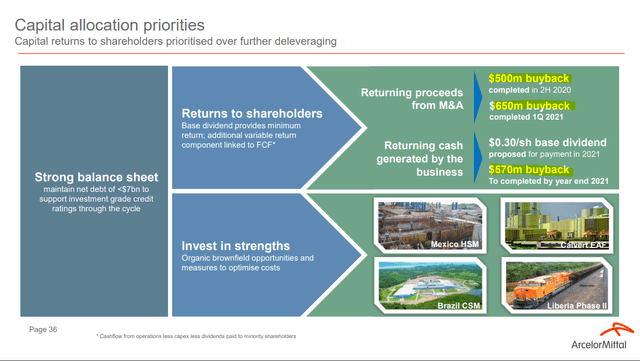

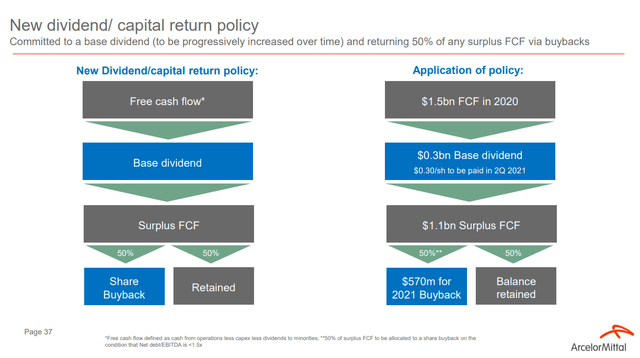

ArcelorMittal Dividend & Buybacks

With EBITDA of $10 billion and a stabilization in working capital, the company could achieve free cash flows of around $5 billion. That gives a price to free cash flow of around 7 which is relatively high considering the natural cycle in the sector. Nevertheless, high cash flows will allow for lower debt levels, likely also zero net debt, alongside $2 billion on buybacks and a strong dividend.

The dividend policy is a stable one where the dividend is just $0.3 billion while they will use 50% of the remaining free cash flow to do buybacks.

I must say I don’t like buybacks done is such a way because they are now doing buybacks with steel prices at record highs and consequently the stock too at record highs.

But, that is their strategy and who am I to argue with their capital allocation. Actually, if they do $2 billion of buybacks on a $36 billion market cap, that should push the market cap up another $10 billion according to the inelastic market hypothesis where $1 of inflows into a stock increases the market capitalization by $5 on average. Given Mittal’s stake being fixed, buybacks could have an even bigger effect.

As an investor I don’t like investing in such swing trades as I prefer to own businesses for the long-term. What often happens in these cyclical situations is that when the trend of high commodity prices turns, companies have little cash forcing them to cut their buybacks and dividends which crashes the stock, like it was the case above from 2018 to 2020, even prior to covid.

Nevertheless, as a cyclical, one has to take the conservative average cash flows and then make a valuation based on that. Demand for steel always be there and the cycles will also always be there. So, buy low and sell high is the mantra. You just need to know the business well and have the guts to buy when everybody is panicking and sell when everybody is euphoric. Despite the myriad historical examples of how cyclicals work, still 99% of the people do the opposite, including ArcelorMittal with their buybacks and asset sales in the worst possible period (Arcelor sold US steel assets in September of 2020, just a month before things started exploding for steel).

Arcelor Mittal Stock Valuation

If we take cash flows as a basis for our valuation, I would say that on average, with a conservative perspective offering a margin of safety, ArcelorMittal could make $2.5 billion in cash flows over cycles per year.

With $2.5 billion of value creation per year where only 10% of that is used for dividends and the rest for buybacks, with a growth estimation rate of 5% thanks to global economic growth and buybacks, I see a conservative intrinsic value for the company of $16 billion.

ArcelorMittal stock valuation – Source: Sven Carlin – Free template download

When I compare the above to Aperam (Aperam stock analysis), which is another steel stock I analyzed in this overview of stocks traded on the Amsterdam Stock Exchange, Aperam seems cheaper and carries less risk given the no debt position already there.

ArcelorMittal stock valuation – Source: Sven Carlin – Free template download (check it for full overview of analyzed stocks)

Anyway, both steel stocks are overvalued if you expect a 10% long term investing return from a conservative perspective. Of course, anything can happen but value investing how we do it, isn’t about ‘anything can happen’, value investing is about finding investments that offer low risk for high returns.

ArcelorMittal stock offers medium return for medium to high risk now which isn’t something I am attracted to. However, if the stock falls 50% as it usually happens in a cycle downturn, it could become a low-risk high reward investment given the improved quality of the business, lower debt and more sustainable focus. Therefore I have put MT stock on my followed stock list and I will be rechecking things when and if the above ratio that is now 0.47 reaches 1 where one could expect long-term business returns of 10% per year which are a good basis to play these steel cycles and perhaps even get 100% or more in a year like we did with Ternium (NYSE:TX) last year.

About the author: Sven Carlin Ph.D. is a dedicated investing educator and stock market researcher focused on finding investment opportunities with a value investing perspective. His research is summarized on the Sven Carlin Research Platform where he covers many stocks and shows his portfolios. The educational part is shared on YouTube and the Free Stock Market Investing Course.