OMAB stock price analysis – higher upside potential than PAC or ASR

This OMAB stock price analysis is part of my global airports stocks list with detailed stock by stock analyses. OMAB is one of the lowest risk airport stocks out there with high potential upside, but get to know it well because at some point you need to sell it due to the concessions ending in 2048.

You can also read more about the Latin American airport stocks traded on the NYSE here: CAAP stock, PAC stock, ASR stock. Here is a video that summarises it all:

OMAB stock price analysis and overview

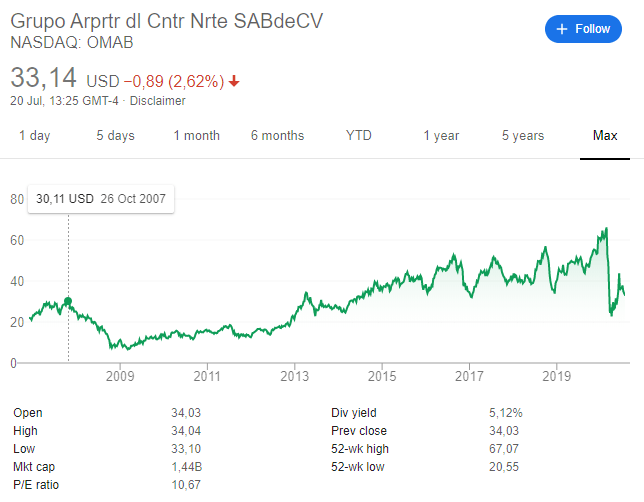

Grupo Aeroportuario del Centro Norte stock – NASDAQ: OMAB

OMAB stock, apart from the dividend, hasn’t really rewarded shareholders over the past 13 years. Of course, those that bought at single digit levels and sold when the stock reached its high of $67.07 in January 2020, did really well. The goal of this OMAB stock price analysis is to see whether at the current level, after a decline of more than 50%, the stock represents an opportunity and what is the return investors can expect from buying OMAB stock.

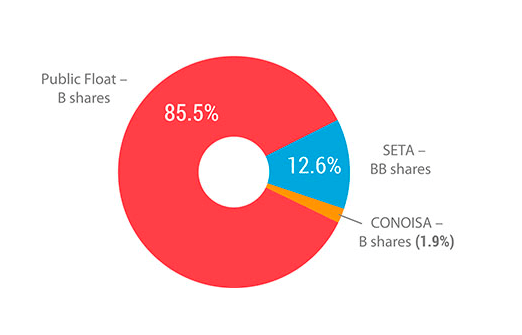

OMAB has 390,111,556 common shares, American Depositary Shares (ADSs) are listed on the NASDAQ Stock Market in the U.S.; each ADS represents 8 Series B shares. The company has been doing repurchases over time and has allocated another 1.5 billion pesos for repurchases in 2020.

Most of the ownership is in free float, same as with all the other Mexican Airport stocks.

This Grupo Aeroportuario del Centro Norte stock analysis comprehends:

- OMAB stock price analysis – business overview

- OMAB stock fundamentals

- OMAB dividend analysis

- OMAB stock price – investment thesis

- OMAB stock comparison with PAC and ASR

The key to keep in mind is that Mexico is an emerging market and that air traffic growth is expected to be significant in the future.

OMAB stock analysis – business overview

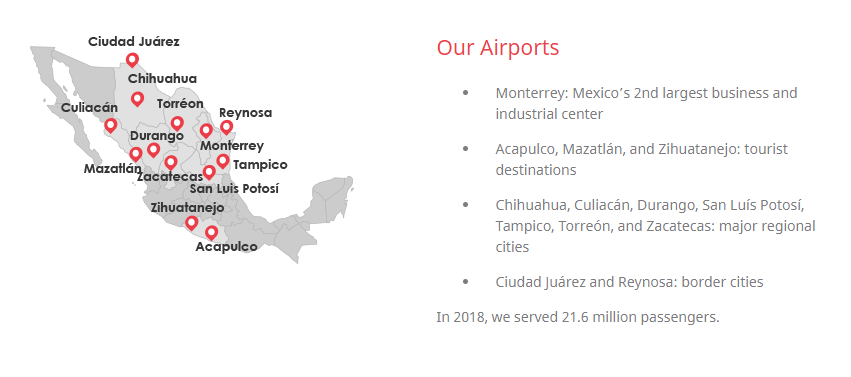

OMAB stock gives you ownership of Grupo Aeroportuario del Centro Norte that owns 13 airports in Mexico with the crown jewel being Monterrey.

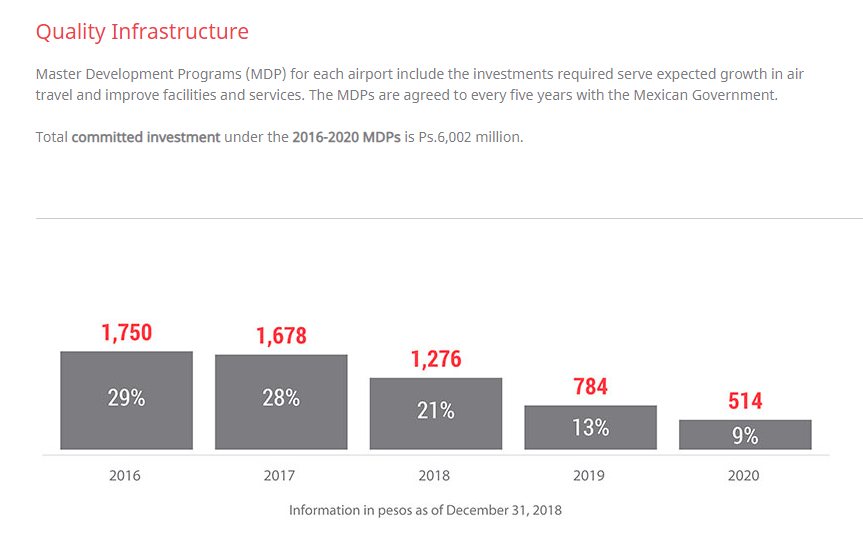

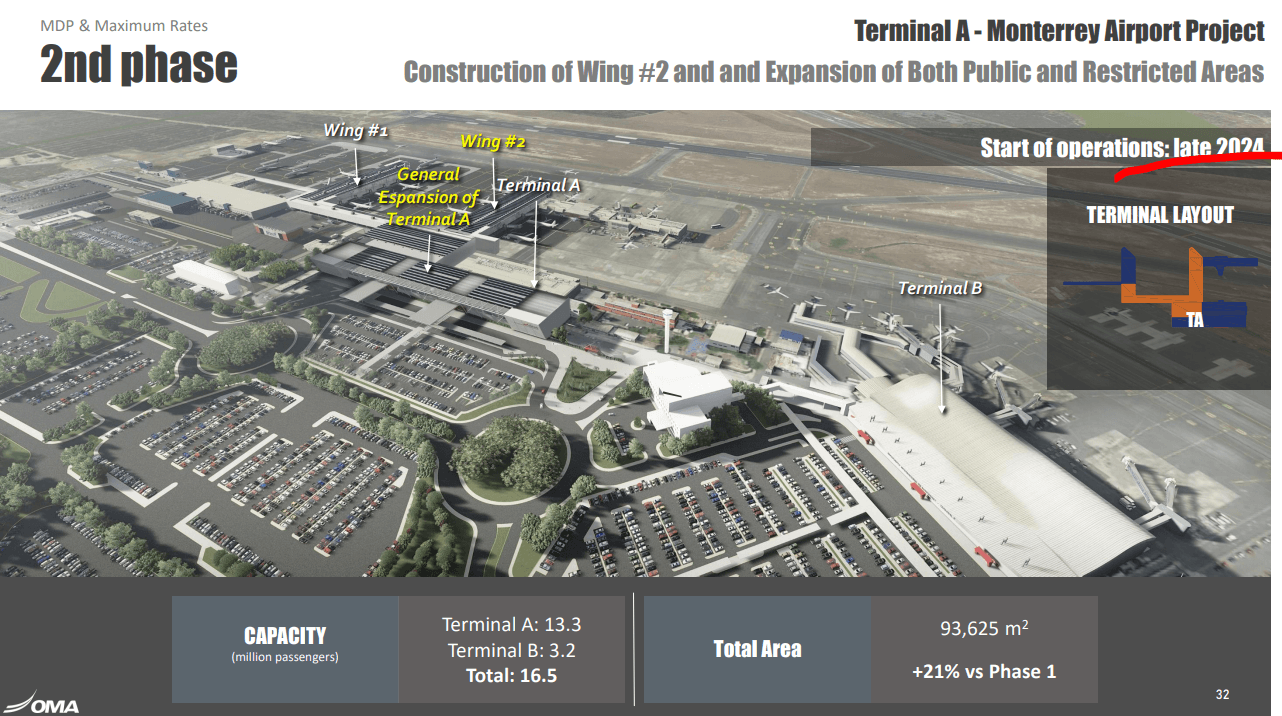

Their major projects underway include the expansion Monterrey terminals A and C, expansion of the Tampico terminal building, modernization of the Zihuatanejo terminal building, a new passenger terminal building in Reynosa and work on runways, taxiways and aviation platforms in several airports. They still have to negotiate their master development plan with the government for the coming years, but they expect capex to be around 15 billion pesos which is significantly more than what has been the case over the last few years. Thus, we have to account for 3 billion pesos of capital expenditures per year. Something that will weigh on the balance sheet, free cash flows and dividends.

They will invest significantly into the expansion of the Monterrey airport that should allow for capacity growth from the current 11 million to 16 million passengers per year when the second phase is completed in 2024.

The above investments should also lead to a 50% increase in traffic over the next 10 years that should also increase profits.

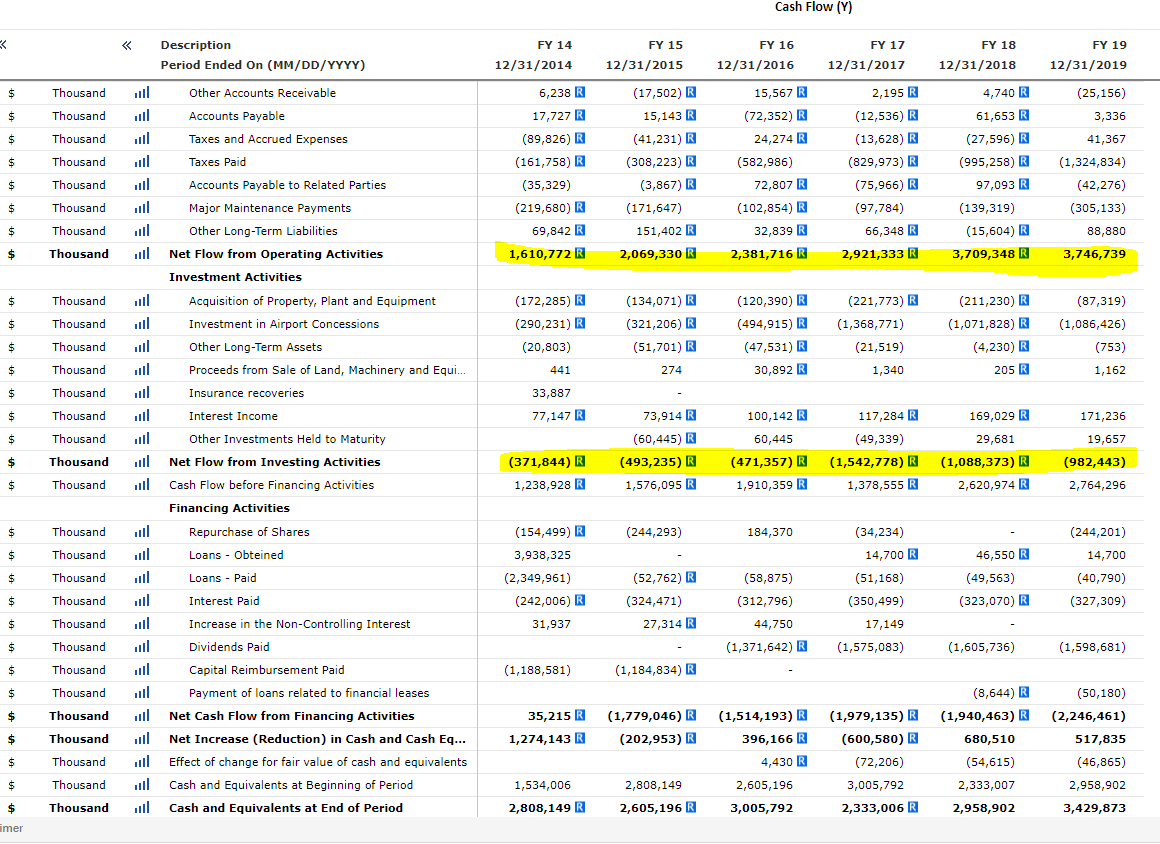

OMAB stock fundamentals

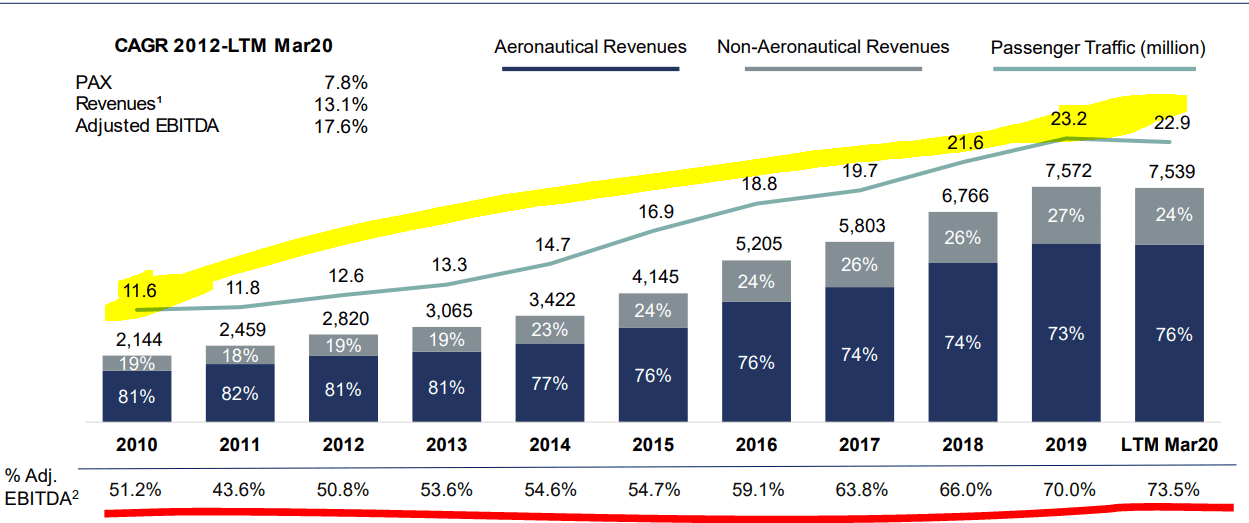

Over the last 10 years, the company has more than doubled revenues and significantly expanded EBITDA margins. That is the beauty of airports; the more traffic, there is more revenue growth but costs don’t grow as fast. EBITDA margins went up from 51% in 2010 to 73.5% in 2019.

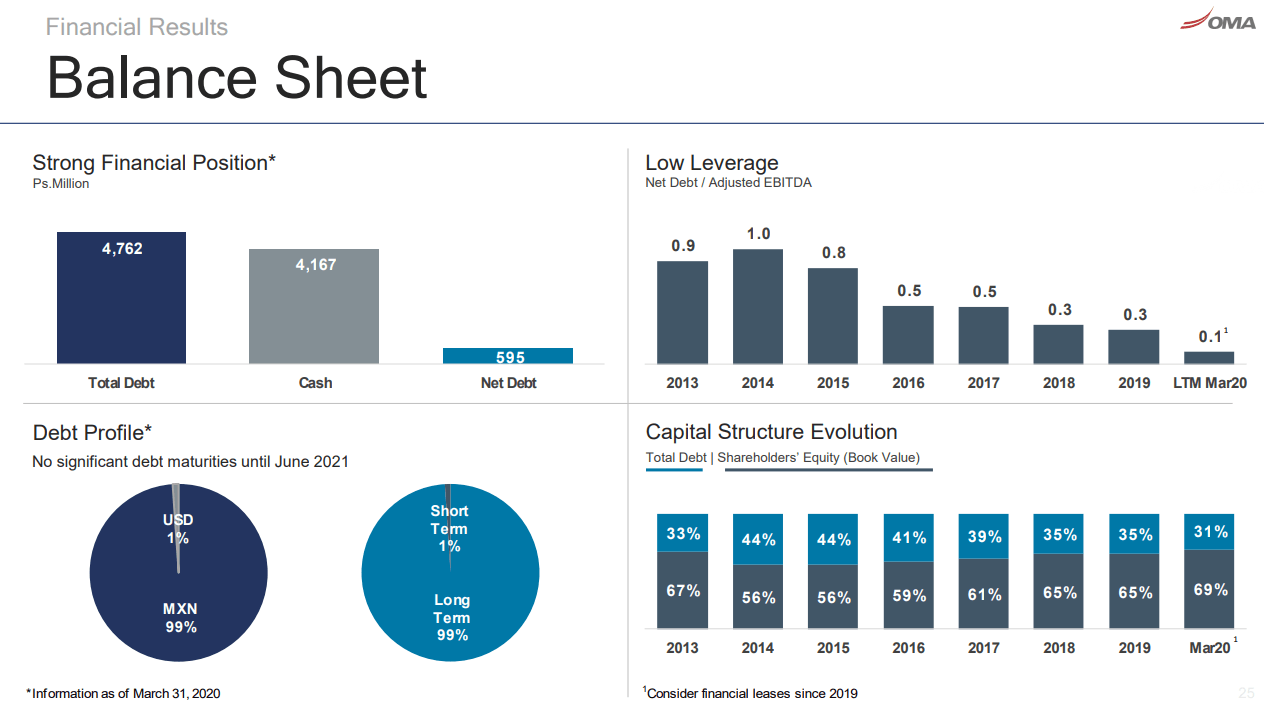

Of the 3 Mexican airport stocks, OMAB has the lowest leverage levels. If we take into account the cash, it practically has no debt. This is good because it will surely survive the COVID-19 crisis and it will have flexibility when it comes to growth capital requirements over the next few years.

While other airports have debt to equity ratios around 1, OMAB’s ratio is at 0.45.

Perhaps the reason for OMAB’s low leverage is the knowledge that the next CAPEX cycle will be significant and they will have to take some debt to finance the developments and still pay a dividend.

From the above, we have to take into account potential growth of around 5% going forward, the high capex requirements over the coming years and the low leverage ratios. I am using a 5% growth rate as a conservative average over cycles. In a good economy, the growth rate in passenger traffic will likely be closer to 10%, but there will always be bad years when growth will be negative 5, 10% or more, so a conservative average of 5% is my estimation that offers a margin of safety.

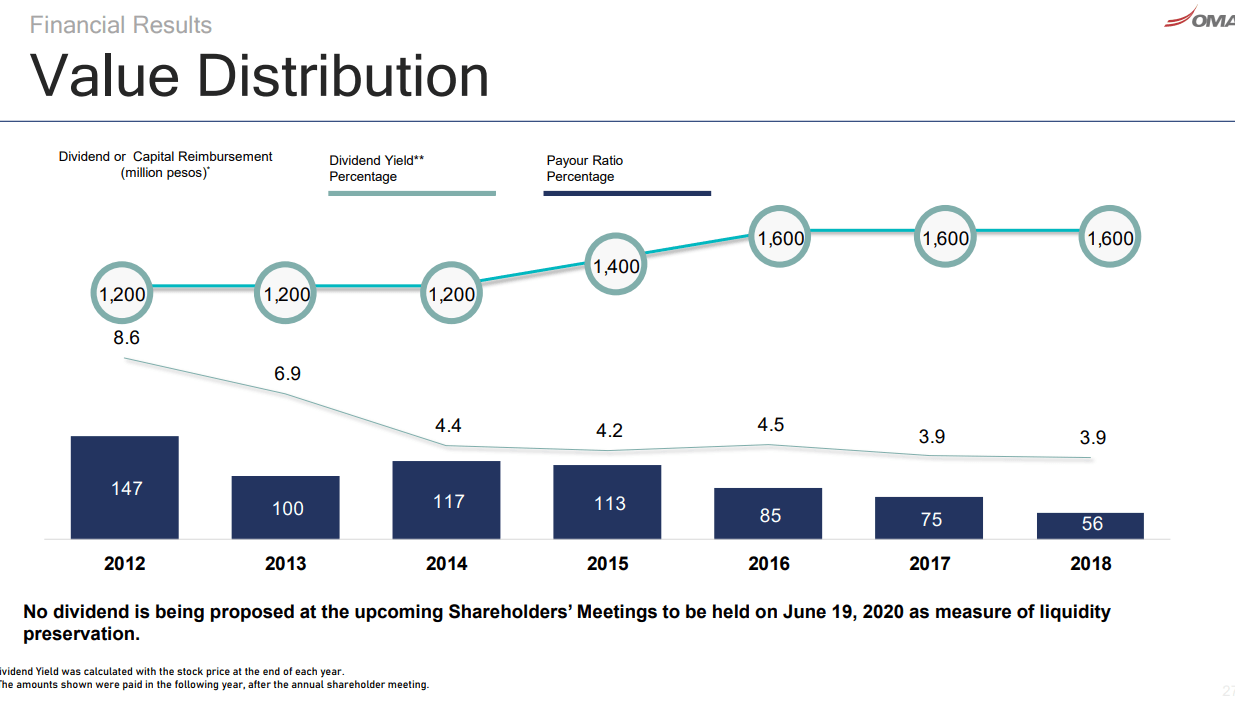

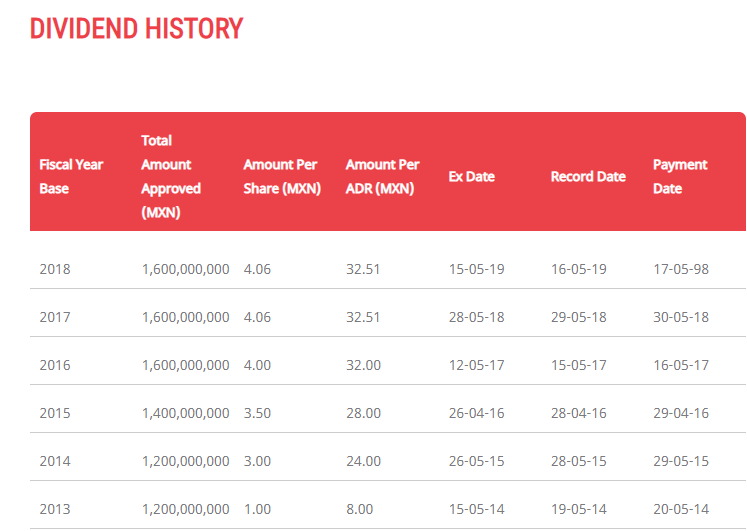

OMAB dividend analysis

Over the past years, OMAB has been paying stable dividends of 1.6 billion pesos or $70 million USD. On the current market capitalization of $1.6 billion the yield would be 4.3%. Before the COVID crash, the dividend yield was somewhere around 2% which I considered extremely expensive. However, investing is about the price now and the future potential.

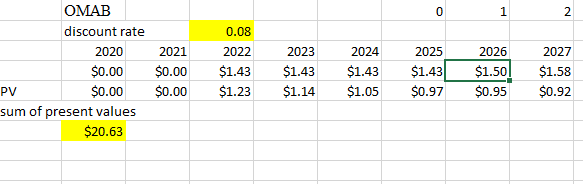

If things return to normal, and the company pays $70 million in dividends again, the dividend per OMAB ADR share would be $1.43.

Let’s assume there is no dividend in 2020 but that they pay a dividend in 2021 of $1.43 and take on debt to pay for the investment requirements.

Those investment requirements should ease by 2025 when the company could pay much higher dividends, especially if revenues grow at high single digit rates or even faster.

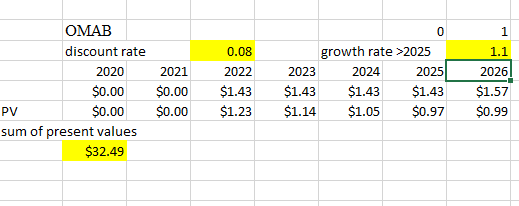

I have created a small model where the dividend is $1.43 from 2022 onward and then grows by 5% per year until 2048 which is the concession ending year.

You can download my excel valuation model here:

With an 8% discount rate and a 5% growth rate after 2025, my sum of present values is $20 which tells me how the stock is expensive even at the current subdued levels.

My valuation is much different than other valuations I have seen but that is because my growth rate is 5% and not 10% and I give no value after 2048 while others don’t count in the concessions ending factor.

However, as the market isn’t looking at Mexican airport stocks by discounting the possible dividends but by applying market airport valuations to the current dividend or EBITDA, there is significant investment potential with OMAB.

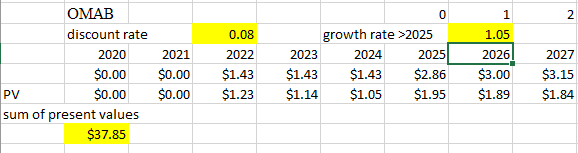

Further, if the company reaches a 100% improvement in free cash flow by 2025 after the investment cycle is over, free cash flows could go from the current 1.6 billion available for dividends to 3.2 billion by 2025, especially if the capital investments lead to better profits. If I double the dividend in 2025, and apply a 5% growth rate afterward, OMAB’s dividend valuation model gives us a current value of $37.85.

From a dividend perspective, OMAB stock price doesn’t really represent a great opportunity, but let’s see what could be the investment thesis from a market’s perspective when you have to sell the stock when exuberantly priced.

OMAB stock price – investment thesis

If the company reinstates its dividend, and actually doubles it by 2025, with a dividend of $2.86, the dividend yield of 8.6% based on current prices would soon become a low single digit yield and thus the stock would at least double. If there is consequently also high single digit traffic growth for a year or two, the stock might even trade at a dividend yield of around 2% like it did before the COVID-19 crisis. This means that the upside is between 300 and 400% if the market focuses on the dividend, the growth and not on the concessions ending in 2048. That is just this conservative author that talks about things that will happen in 28 years.

On the risk side, if things don’t recover in a year or two, then it might get ugly, but if things don’t recover, then it will be ugly everywhere so see how OMAB stock or other Mexican airport stocks fit your portfolio where those give you exposure to emerging markets, a rebounding economy and all of that with a moat.

OMAB stock comparison with PAC and ASR

When making a comparison between OMAB stock, PAC stock (Grupo Aeroportuario del Pacifico) and Grupo Aeroportuario del Sureste stock (ASR), OMAB is the most domestic/industry focused play while PAC and especially ASR with Cancun are more leisure focused.

Further OMAB has the lowest leverage and the highest potential when it comes to growth because it seems that what has happened for PAC and ASR, still has to happen for OMAB. Cancun’s growth is not likely to continue at previous rates while the leverage is there already and the dividend standards are set high already. There is a similar situation for PAC.

Thus, OMAB offers the highest potential for dividend growth as there is a chance for the dividend to double by 2025 while ASR and PAC offer ‘only’ steady single digit growth potential. Consequently, from a stock price perspective, if PAC and ASR have 100% upside potential, OMAB offers 200% and higher upside potential with less risk due to lower leverage ratios.

The OMAB stock price analysis is part of my Airport stocks analysis made by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundred of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: