CAAP Stock Price Analysis – Corporacion America Airports Stock Is An Ugly Buy But Offers Potential

This CAAP stock analysis is part of my global airports stocks list with detailed stock by stock analyses. CAAP stock is a risky bet when compared to other airport stocks out there. So, check the list to find something suitable for you – the time to buy airports is now when those are down.

Here is a video discussing NYSE listed airport stocks, written CAAP article continues below:

Summary:

- CAAP can’t go bankrupt as the debt is on a subsidiary level.

- The sum of parts, even without the Argentine airports, is higher than the current market capitalization.

- But, the concessions on the owned airports expire relatively soon for airport investments and the debt taken by the subsidiaries has high yields.

- All in all, an ugly value investment that is risky but if things improve one can expect returns between 400% and 600%.

CAAP Stock Overview – NYSE: CAAP

Corporacion America Airports went public in 2018 but since the IPO, the stock performance has been disastrous as the stock is down 85%.

The reason for the above tragedy is COVID-19 but mostly CAAP’s exposure to Argentina that we’ll analyse in this article.

CAAP stock market capitalization is at $411,26 million.

This Corporacion America Airports stock analysis will comprehend:

- CAAP’s business overview,

- CAAP’s fundamental analysis,

- CAAP stock fundamental value – debt is with subsidiaries and,

- CAAP’s investment risk and reward thesis.

CAAP Stock Analysis – Business overview

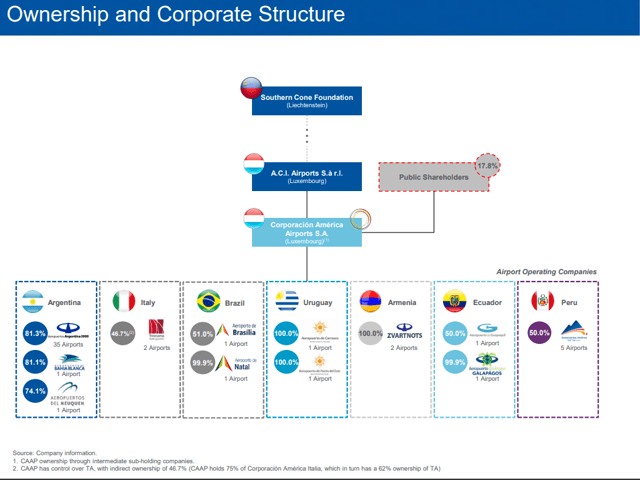

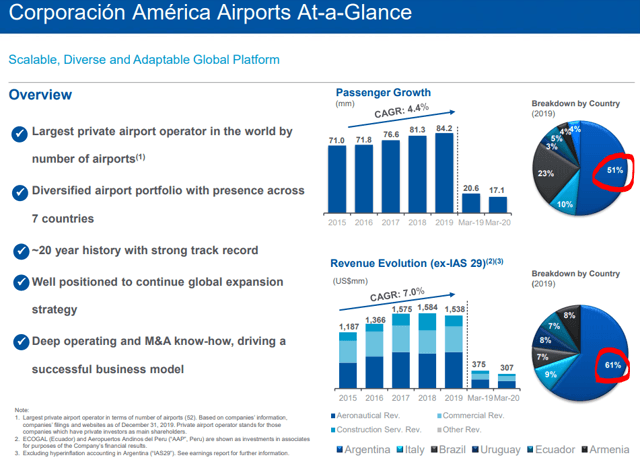

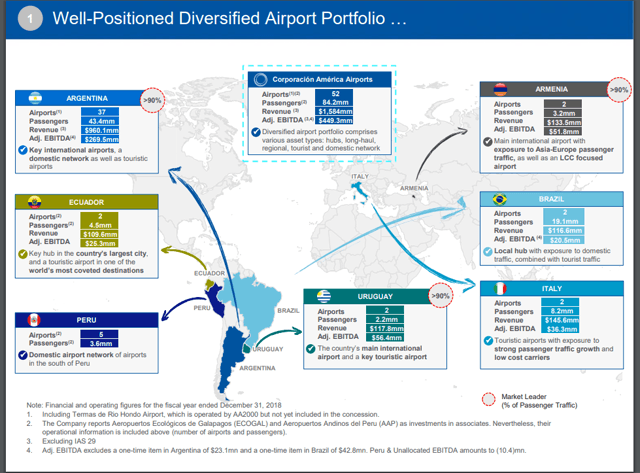

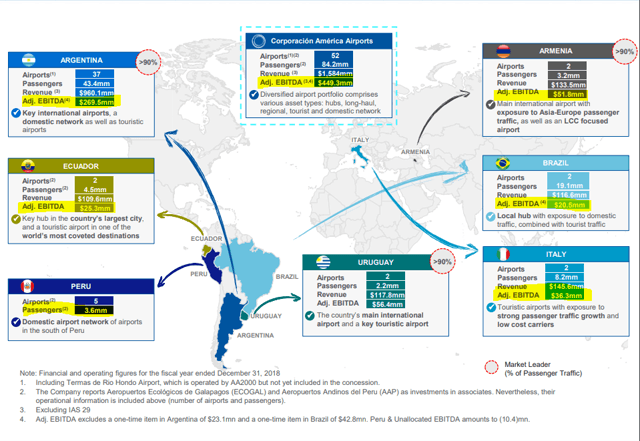

The company is a global airport operator but mostly focused on Argentina where it operates 36 airports with a weighted ownership of 81.3%. It also owns 62% of Toscana Aeroporti, listed in Italy and funnily, with a market capitalization of 259 million EUR, or more than half of the parent’s market capitalization.

61% of revenues come from Argentina, 9% from Italy and similar revenue splits come from Brazil, Uruguay, Ecuador and Armenia. These, except Italy, are emerging or even frontier markets. This means that any investment in a stock there will be extremely volatile due to the market’s sentiment and shallow markets.

When things are bad, nobody wants to own frontier market stocks, especially those traded in developed markets like the NYSE, and the consequences are often declines similar to the 85% decline described above because, in bad times, the pressure to sell is high and demand is little. However, the opposite is also possible because the shallow market, low float, can lead to high spikes if things start to improve.

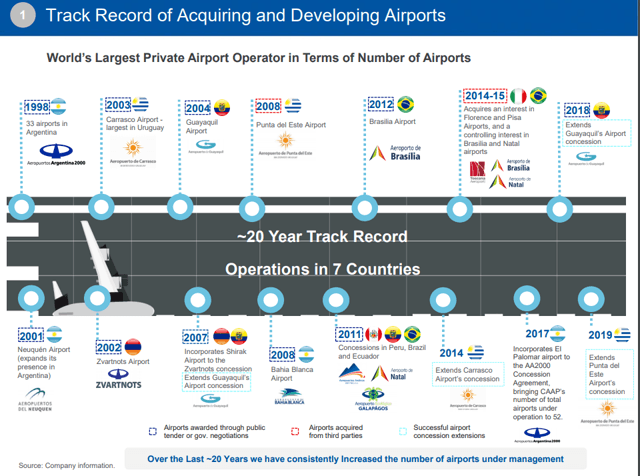

The company’s strategy is to acquire airports and develop them.

I must say I am amazed by their performance since the acquisition of Toscana Aeroporti in 2014 because they significantly improved all metrics and even increased the dividend from 10 EUR cents to 70 EUR cents. This might be an indication the management is very capable in what they are doing.

However, something I don’t like are the concession expirations that will happen relatively soon when compared to other airport stocks. Also, the industry is highly competitive, so a smaller player like CAAP is forced to take what other bigger airports, with much more financing power, are not willing to invest in.

CAAP’s airports success and their performance will depend on the situation in the respective country in the long-term and on the capacity to survive COVID-19 in the short-term. Currently, due to COVID-19, things are bad everywhere and the company announced traffic declines of more than 98% for May and 97% for June.

The main question is whether this company can survive the COVID-19 hit? To find the answer we have to look at the fundamentals.

CAAP stock fundamental analysis

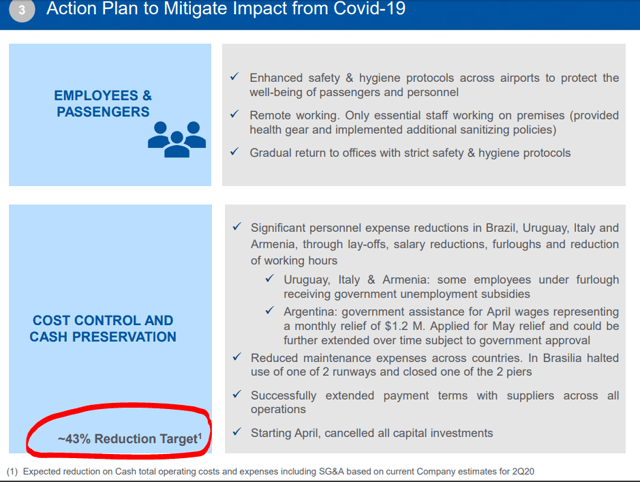

Their first target is to reduce costs by 43%.

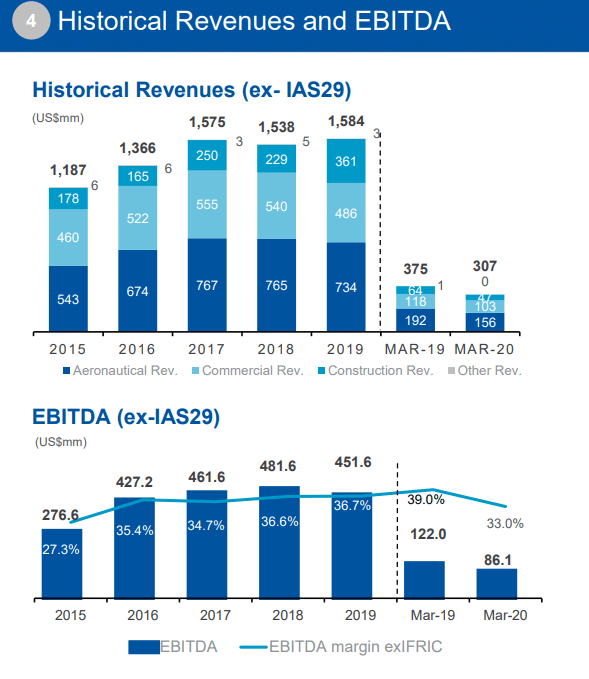

With costs of $1.05 billion in 2019, a 43% saving rate will bring yearly costs down to $430 million or $107 million per quarter. (Revenues at $1.5 billion, EBITDA at $451 million in 2019, thus costs were $1.05 billion)

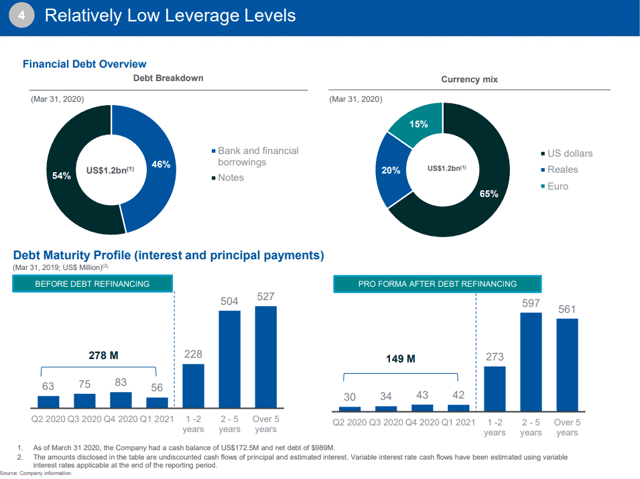

The company’s debt level is at $1.2 billion and thus 3 times the market capitalization. Something the market and finance institutions don’t really like when it comes to emerging or frontier market stocks.

Over the past months, CAAP has managed to refinance some debt, has $172 million in cash, but that might, if we deduct the debt repayments, last only 1 quarter. If the company’s financing institutions refuse to refinance the debt, this business could be bankrupt by the end of the year.

CAAP stock fundamental value – debt is with subsidiaries

The easy thing to say when analysing CAAP stock would be how it is highly risky due to the debt and how it can go bankrupt. However, despite the debt level of $1.2 billion, that is not correct.

CAAP’s debt is held at subsidiary level where those companies guarantee it with their assets. Some capital has gone out form the Luxembourg holding company towards the subsidiaries as required by concessions agreements, but CAAP can’t really go bust on subsidiary debt because it is non recourse debt.

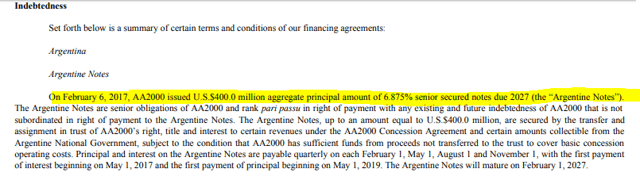

For example, $400 million of the above $1.2 billion in debt falls under the AA2000 group of airports.

There are other two credit facilities of $85 million and $35 million under AA2000 issued in 2019 so in total the Argentine debt is $520 million.

CAAP’s debt structure is as following:

- Argentina $520 million

- Italy 112.5 million EUR

- Brazil – R$329.3, R$558 million, R$300.0 – approximately $220 million

- Uruguay – $200.0

- Ecuador $9 million

- Armenia $160 million

- Peru $10.5 million

For a total of $1,2 billion. So, when it comes to COVID survival, the question is which airports will go bust and which will not? So, bankruptcy is probably not the only thing the market is discounting. Subsidiaries can go bust and can be taken over by governments or banks, not the company.

Now, let’s say they lose the Argentinian airports and the government takes over. The other airports might still offer value if you would give them a valuation similar to acquisition valuations over the last years which is around 12 times EBITDA. The Italian airport has a market capitalization of 262 million EUR where 62% of that is already 162 million EUR or $184 million.

If we attach a similar valuation to Armenia and Brazil, that have similar revenue levels and equal weighted EBITDA, we are already at $552 million which is more than the current market capitalization. Ecuador and Uruguay should also be valuable based on an EBITDA valuation.

CAAP stock price outlook and investment thesis

The CAAP stock investment thesis depends on the will banks and financial institutions for refinancing a company mostly owning airports in Argentina and other countries. They are doing whatever they can to defer loan payments and refinance but whether it will be enough, depends on when will this COVID-19 situation return to normal.

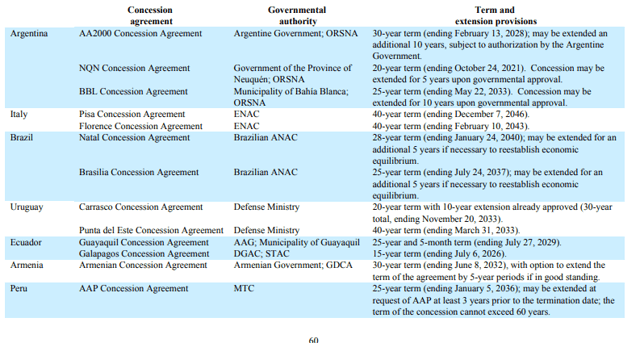

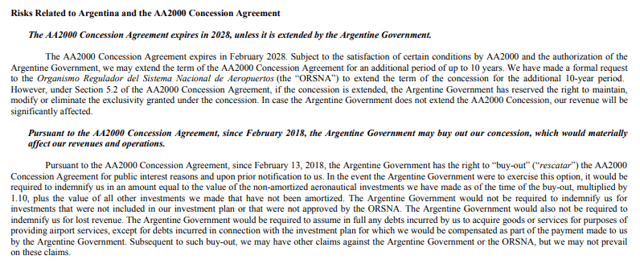

Apart from the risk of bankruptcy per country, their Argentinian concessions expire in 2028 and with Argentina, you never know what will happen. Also, the government can buy out their concession whenever they want.

To conclude, the owners of the company did well to launch an IPO when Argentina was a hot market in 2018. At the IPO, the company sold over 11.9 million shares, while a shareholder sold 16.7 million to raise a total of over $485 million what is now more than the market capitalization.

Another risk might be that the owner, Argentine billionaire Eurnekian, decides to take the company private at current low prices. He can easily do that with the money from the IPO.

CAAP’s stock price and investment will depend on:

- Available financing to survive the COVID-19 crisis

- The Argentine government

- The 2028 concession expirations

- The longer-term economic growth in Latin America and consequently the impact on airport traffic

- The owner’s intentions and financial availability – will small shareholders be screwed?

So, the market is taking a holistic view of the company and not a segmented view of it. However, the market might be right as the situation in those countries is not good and the interest rate on the debt is also high, above 5% in all cases except Italy.

So, we can categorize CAAP stock as an ugly value investment where the sum of parts is more valuable than the market capitalization. What usually happens to ugly investments where there is no catalyst, is that the stock keeps going down which increases the negative market’s perception and puts even more pressure on the stock price.

So, from the risk side there is definitely value, but it is not a great business that I would like to patiently own and wait for the situation to improve. The main reason for my negativity are the concessions that expire relatively soon. This means that for a good return things must improve as soon as possible. Also, when there is a time limit on an investment, it isn’t really an investment but more of a bet and I don’t like betting.

But, if you like betting, on the reward side, a normalization of the situation could push CAAP’s stock price back to IPO levels of $16, or at least $10 and give you a 6x or 4x return. But, other things can happen too, like; bankruptcies, governmental issues, concession losses etc. that could push the stock even lower. It is unlikely there will be dividends soon and my main issue with CAAP remains the concessions expiration date which doesn’t make it a great long-term investment for me.

The CAAP Stock Analysis is part of my Airport stocks analysis made by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundred of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: