PAC Stock Price Analysis – 8% Dividend Return And 100% Capital Gain Possible

This PAC stock analysis is part of my global airports stocks list with detailed stock by stock analyses. You can also read more about the Latin American airport stocks traded on the NYSE here: CAAP stock, OMAB stock, ASR stock. Here is a video that summarises it all, article continues below:

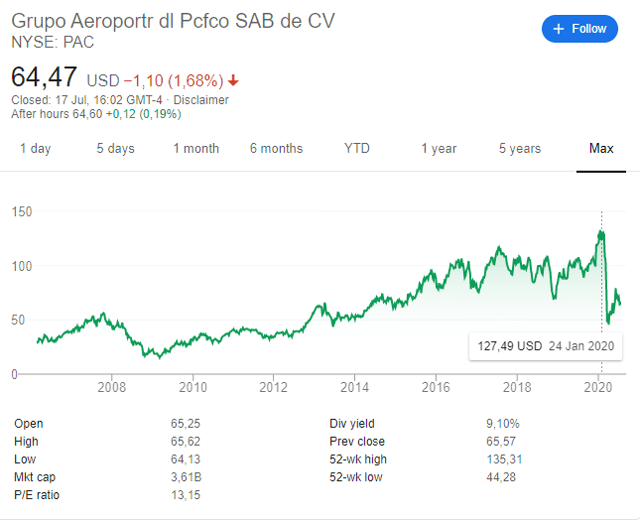

PAC stock overview – NYSE: PAC

I have looked at Grupo Aeroportuario del Pacífico Stock stock a few times over the last years and it always seemed too expensive to me.

However, the expensiveness didn’t stop it to reach a high of $135 just prior to the COVID-19 crisis. The investing thesis has always been based on the high single digit Mexican market growth, backed up by revenue and dividend growth, so it is time to see whether this interruption and stock price decline of 50% gives an opportunity for long-term investors.

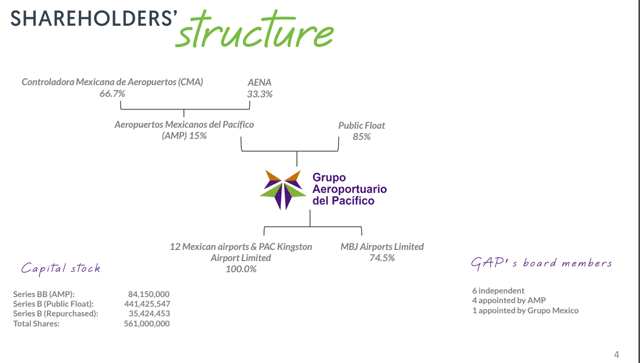

Grupo Aeroportuario del Pacífico stock owners are mostly free float. Even AENA, analysis here: Aena stock analysis, owns 5% of the company.

Weighted average number of shares outstanding according to last 20-F is 525,575,547. One PAC stock ADR traded in NYSE represents 10 shares.

This PAC stock analysis will consist of the following:

- PAC business overview

- PAC stock fundamental analysis

- PAC dividend stock valuation

- PAC stock investment thesis

PAC stock analysis – business overview

PAC operates 12 airports in Mexico and two in Jamaica.

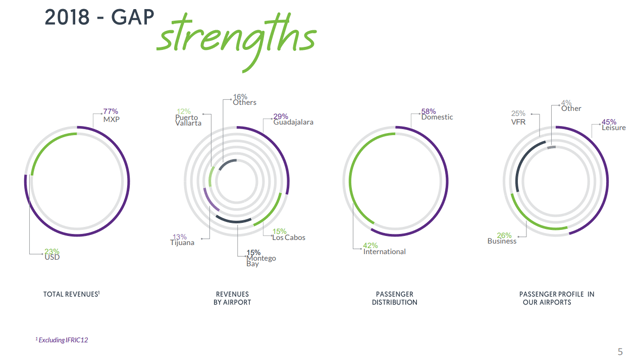

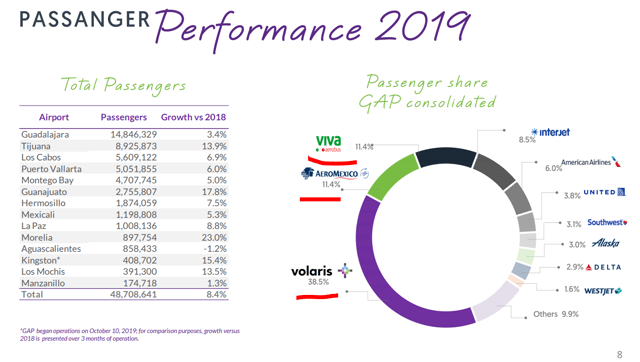

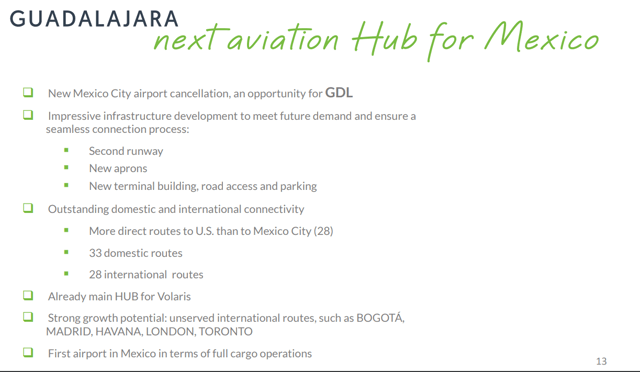

Guadalajara is the main airport contributing to 29% of revenues. 58% of traffic is from domestic sources and 45% of travellers are travelling for leisure.

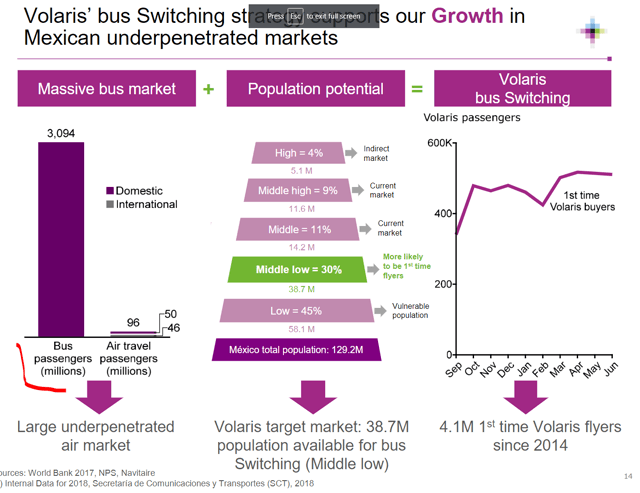

So, revenues will depend on tourism in Mexico but also on domestic flying because still few people in Mexico take the plane compared to busses.

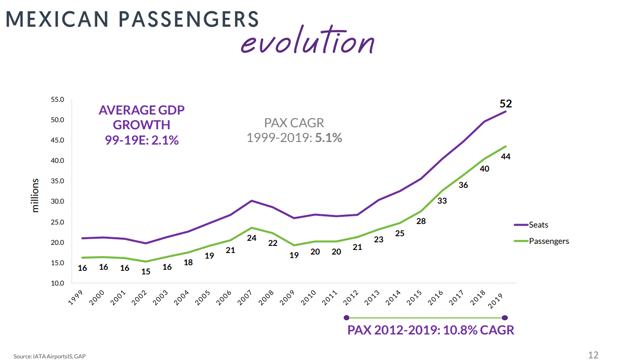

The fact is that Mexicans are taking the plane more and more and given the geography, the trend will likely continue, especially if there is economic growth. On the other hand, we have seen a 25% decline during the 2009 crisis and then it took 6 years to get back to the previous level. Something to keep in mind before investing and expecting the trend will just continue as it was the case up till 2020.

Of course, due to COVID-19, there will be a significant interruption in traffic and it will take a few years for things to return to 2019 levels, but we as investors look for long-term cash flows and that is what we are going to focus on here.

Most traffic comes from Mexican airlines, especially Volaris, and North American airlines.

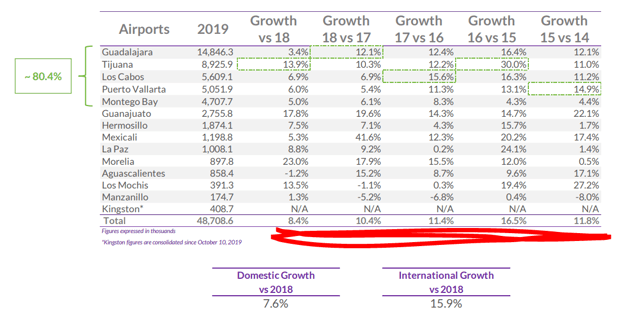

Traffic growth over the past years has been staggering and often in double digits.

It is likely that the same positive growth trend continues after COVID-19 and further fuels PAC stock growth, profits and dividends but when will growth resume is the main uncertainty.

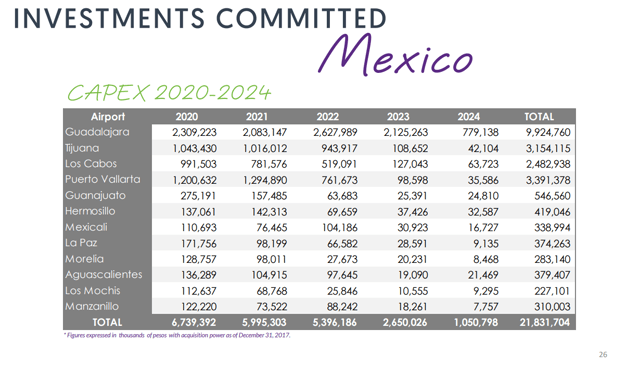

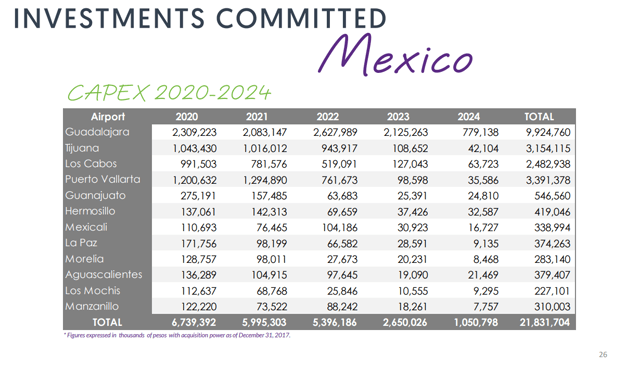

PAC growth plan includes a second runway for Guadalajara, new terminal building. A new processing building in Tijuana so that it can become a hub and transit passengers don’t have to deal with Mexican authorities.

To grow, the company will have to invest significant amounts and the total expected investments are 21.8 billion pesos under the Master Development plan where the number had been set in 2017. Given the inflation rate in Mexico, the usual additional costs, I would assume the CAPEX to go to 25 billion pesos or $1 billion USD over the coming 5 years. They will try to delay some things over 2020 but the CAPEX is a requirement both from the concession and from the growth perspective and can’t be delayed much. The high CAPEX will have an impact on dividends, but more about that in the dividend discussion. Another $213 million will be spent for the two Jamaican airports.

Let’s take a look at the fundamentals.

PAC stock fundamental analysis

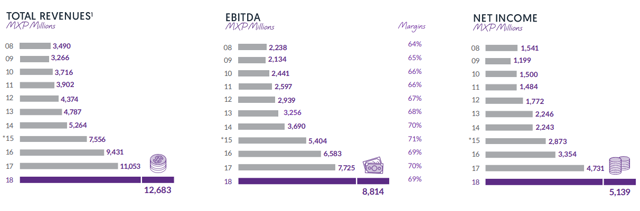

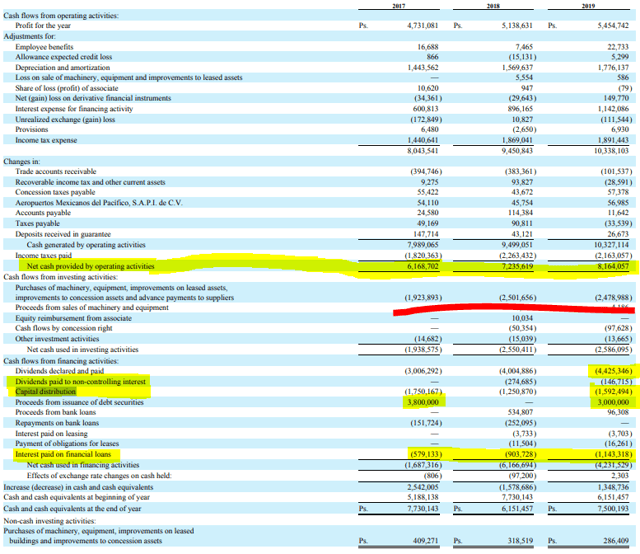

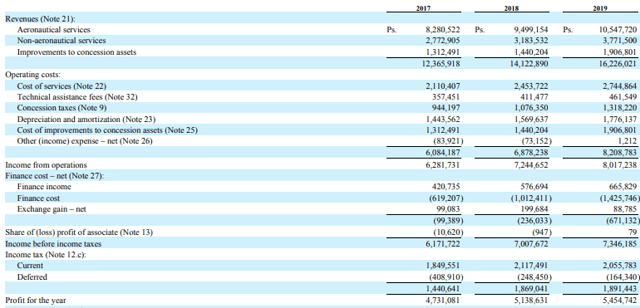

PAC’s performance has been outstanding over the past decade with a quadrupling of revenues, EBITDA and net income.

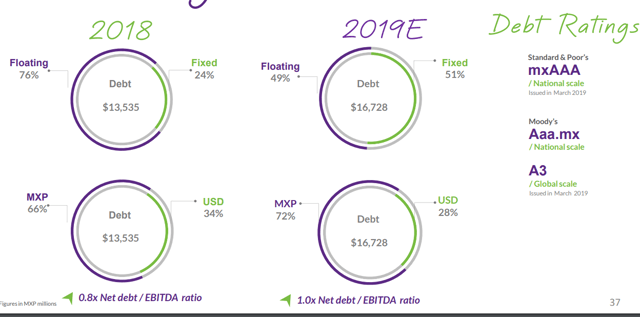

Unfortunately, debt increased in line with the above, but is still pretty manageable with good credit ratings and debt to EBITA ratio below 2.5 which is also the company’s target.

Shareholder equity is growing slowly while the largest jump in debt has happened in 2015 and in 2019. Still, debt to equity is 1.

A look at the cash flows tells us how their operating cash flows grew approximately 1 billion pesos per year and in 2019 those were 8.1 billion pesos or $361 million USD ($1 = 22.58 MXN). During 2019, they invested 2.4 billion pesos, paid 4.4 billion in dividends and another 1.5 billion as a capital distribution.

Thus, they paid out practically all the cash made and also took debt to pay for it all. I don’t know about you, but I never like it when a company takes on debt to pay out dividends. For me it is a short-term benefit against long-term constant pain. Of course, PAC’s structure allows for such things as still little indebted, but debt should be only used for growth or in crisis situations like COVID-19 and others that will surely come. We can see how the cost of debt doubled over 3 years and is now more than 10% of operating cash flows.

As the company is one where the focus is on dividends, we can call it a dividend growth stock, a PAC stock valuation has to come from a dividend perspective.

PAC dividend growth stock valuation

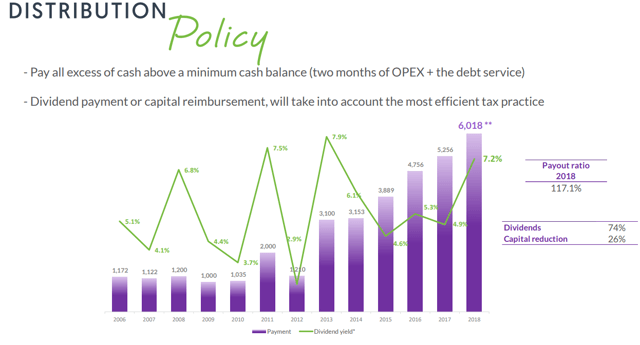

PAC’s dividend distribution policy.

PAC’s dividends have been very generous over the last years and we have seen above that they paid out 6 billion in 2019 which is 27.2% of equity. The dividend pay-out in 2019 was around $265 million or $0.5 per share ($5 per ADR). This gives a dividend yield of around 7.6% on the current price.

It is important to keep in mind that the dividend yield was half of that before the recent stock price drop because a 3.8% yield will likely be what the market will be requiring and pricing PAC’s stock at, if and when things return to normal.

One issue that might keep the dividend lower for a while are the capital requirements over the coming 5 years. This is a requirement under the Master Development Plan and concession agreement so can’t really be postponed much.

Over the coming 3 years, or at least whenever the circumstances will allow it, capital expenditures will be around 6 billion over the next 3 years and will make it very unlikely there will be dividends over the coming 3 years. We can expect a reintroduction of dividends alongside traffic growth somewhere in the next 5 years.

PAC’s dividend valuation model

I have created a small model for PAC’s stock dividend valuation where I assume the following dividend up to 2025 with consequent growth of 5% per year. I have used a 5% growth rate because it is likely there will be other crises in the future and therefore it is conservative to take half of the average.

Calculating the present value in my excel file and attaching an 8% discount rate to the future cash flows in the form of dividends, excluding taxation, the sum of present values for PAC’s stock is $64.85. So, if we see a recovery up to 2025, investors can expect a long-term investment return of 8% at current stock levels.

I don’t know what is your required investment return, but you can change the discount rate in my excel file and see at what price PAC stock fits your investment requirements.

PAC stock investment thesis

In addition to the dividend coming from 2024 to 2048, there is a stock price recovery potential of 100% if and when things return to normal because the market will require a 3.8% dividend yield as it was the case in 2019. Additionally, traffic and consequently revenue growth should be another bonus for shareholders.

I don’t think the market will start thinking about the concessions ending in 2048 prior to 2035. The market is always myopic.

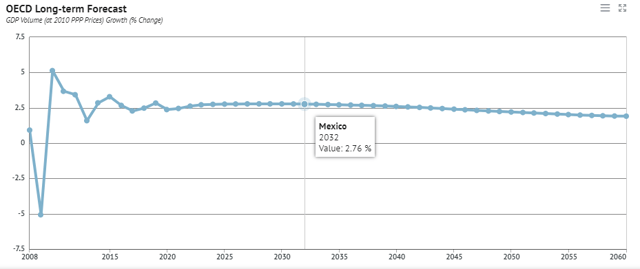

In the past, traffic growth was in the high single digits on low single digit GDP growth. The long-term forecast for Mexican GDP growth is expected to be somewhere around 2.5% and thus we can expect traffic growth to be in the mid to high single digits going forward. If this translates into dividend growth too, that will push the stock price higher too.

Of course, the 5% GDP decline in 2009 resulted in a 25% traffic drop and a 6 years struggle to return to 2008 levels. Thus, if we assume things to return to 2019 levels by 2025, one can expect a double in the stock price by then and a dividend yield on cost of 7.6% alongside a potential for further 5% yearly growth.

To sum up, by investing in PAC stock now you can get:

- 100% return over 5 years if and when things return to normal

- 7.6% dividend yield on cost if and when things return to normal after CAPEX cycle ends, thus around 2025.

- Growth ahead in the mid to high single digit range.

- An 8% returns based on the discounted dividend cash flows before taxation.

From a risk perspective, the Mexican airport concessions last till 2048 while the Jamaican last till 2033 for MBJ and 2044 for Kingston. So, the risks are mainly in the form of COVID-19. How long it is going to last and how much will the capital structure be burdened with it is the main question.

Over the past years, we can say that cash flows have been close to 50% of revenues, thus with some savings, the stillstand costs for PAC could be around 6 billion pesos per year and thus comparable to just one good year of dividends. So, there shouldn’t be a big risk to the going concern.

The biggest risk from an investment perspective is the timing of the recovery which is an uncertainty at the moment and a thing to be watched. Given PAC’s stock is an emerging market stock you can expect high volatility and a delay in recovery compared to developed markets. But, when the recovery starts, you can expect too be significantly rewarded as an investor.

The PAC Stock Analysis is part of my Airport stocks analysis made by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundred of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: