Berkshire Hathaway Stock Valuation – Just Burlington is Worth $200 billion

Berkshire Hathaway stock valuation – sum of parts

I recently did a full sector analysis of railroad stocks and to do a proper comparative analysis I also looked at the numbers from Berkshire’s Burlington Northern Santa Fe railroad.

Two things stunned me;

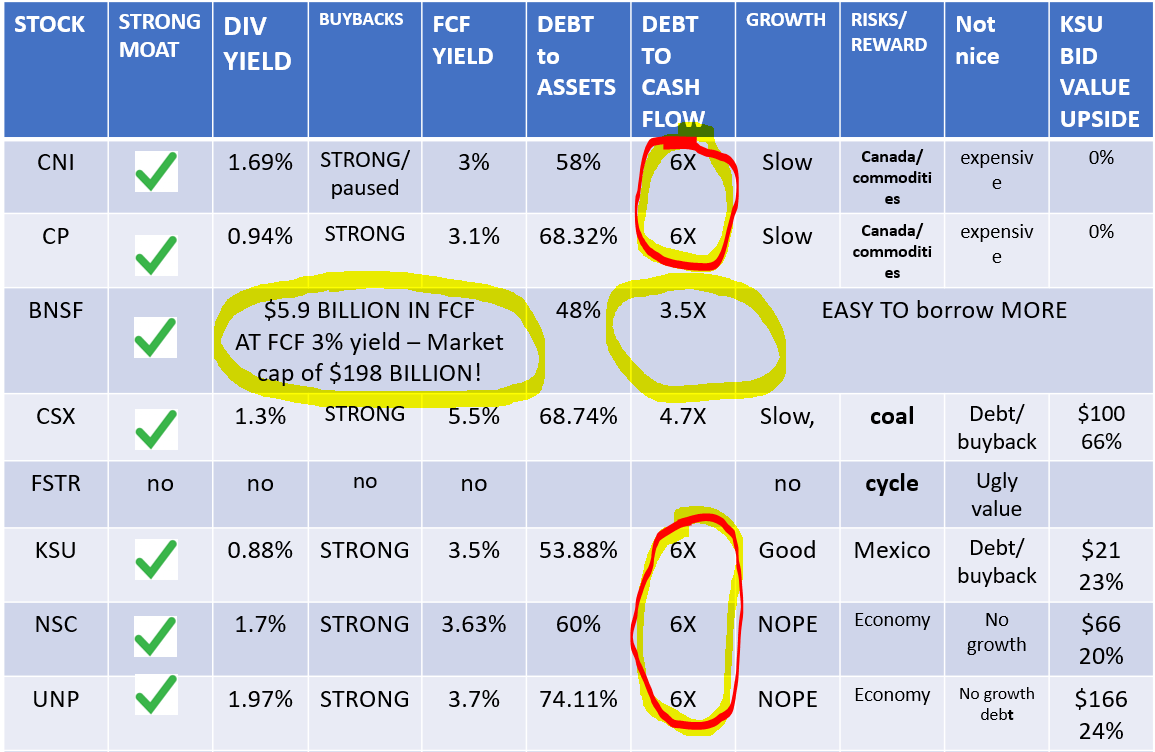

- The fact that BNSF has a debt to assets ratio of 48% and debt to free cash flow is 3.5. Both much lower than the sector average debt to assets ratio of 60% and debt to free cash flow of 6.

- The fact that given BNSF’s quality and low debt, the market would likely price it, similar to other quality railroad stocks, with a 3% free cash flow yield, if not lower. Thus, BNSF’s market capitalization could easily be $200 billion if it were a public standalone company. Just BNSF would make 40% of Berkshire’s market capitalization. Buffett really did make a great investment when buying BNSF in 2009.

The debt structure is typical for Buffett where by being the lowest indebted in the sector, he is sure he will be the survivor in case of a crisis. This allows him to compound for eternity which is what made him one of the best, if not the best investor over the last 7 decades. The low debt levels are likely a headwind in the short term for BRK stock because he is not following the Wall Street mania of chasing short-term benefits like all other railroads are doing by forcing buybacks and pushing their stock prices higher like there is no tomorrow. As history has thought us over and over again, Buffett’s way is the only way for long-term investing success.

In this article I make a sum of parts valuation of Berkshire Hathaway that shows what would be the likely market value of Berkshire Hathaway’s holdings as standalone businesses.

Berkshire Hathaway sum of parts valuation content:

- Burlington Northern Santa FE – $200 billion at least

- Berkshire Hathaway Energy – $70 billion at least

- Manufacturing, service and retailing – $180 billion

- Stock market – $227 billion

- Insurance – $25 billion

- Cash – $143.5 billion

Here is the Berkshire Hathaway stock valuation video version for those who prefer watching:

TOTAL $845 BILLION

The goal of this article is showing how undervalued Berkshire Hathaway is compared to the market and corporate America’s focus on financial engineering to push stock prices higher, not on creating businesses that will pay dividends forever which is BRK’s focus. In summary, by buying Berkshire Hathaway stock, you buy a great business at a discount to everything else.

I will compare the Berkshire Hathaway’s holdings, their earnings and cash flows with what would be a good market proxy.

Burlington Northern Santa Fe – $200 billion at least

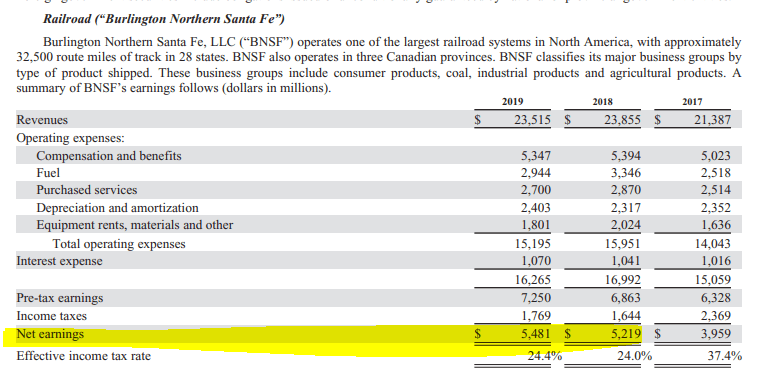

Net earnings for BNSF were $5.4 billion in 2019 but I prefer to value a business from a cash flow perspective because net income can vary depending on the accounting situation.

The free cash flows, that with BNSF are a bit higher than net income, is what I have used to value all railroads. I used 2019 free cash flows on the assumption that things will normalize sooner or later and that 2019 metrics give a good proxy to make long-term valuations.

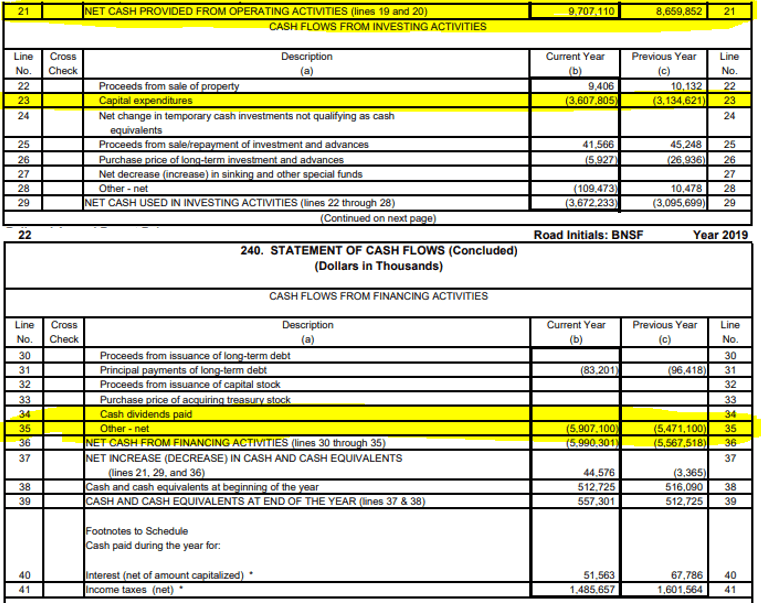

BNSF’s 2019 operating cash flows were $9.7 billion, capital expenditures $3.6 billion that leads to free cash flows of $6.1 billion. Buffett got $5.9 billion in cash as the company paid that out so best to use $6 billion as free cash flows.

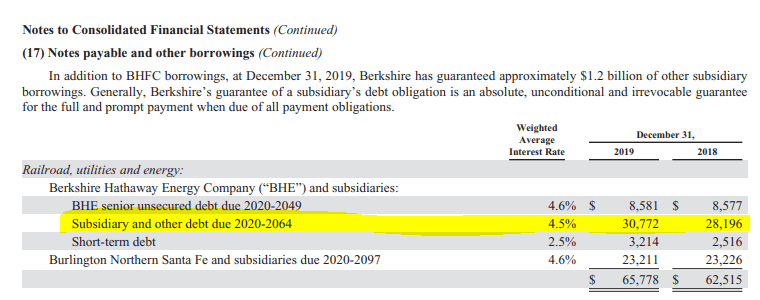

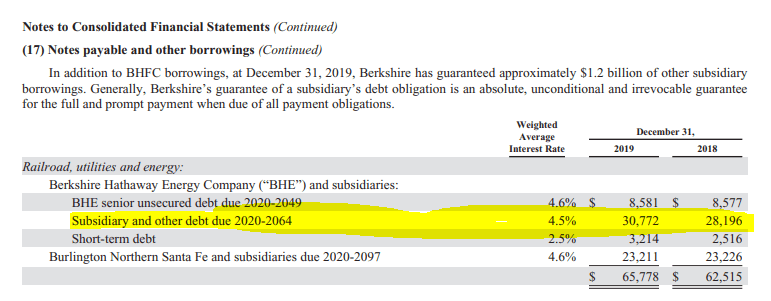

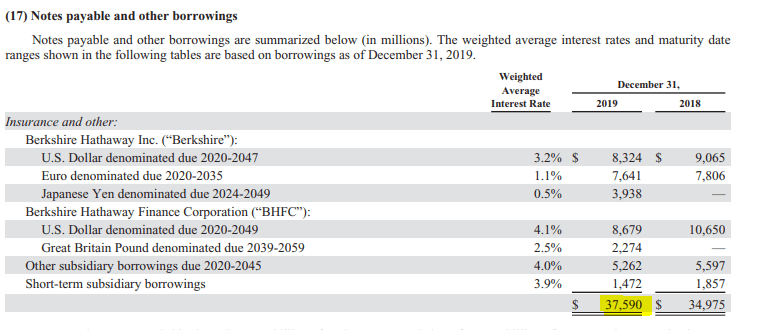

Another important thing is that BNSF has low debt making it the railroad stock with the lowest risk. BNSF’s long-term debt is just $23 billion putting its debt to free cash flow ratio at 3.5 which is much lower than the average for other railroads of 6. Buffett could easily leverage BNSF and get another $15 billion or more if necessary for acquisitions.

Burlington Northern Santa Fe debt, not included in BNSF’s balance sheet – Source: Source: Berkshire Hathaway 2019 Annual Report

Buffett and Munger often mention how their biggest advantage is that they don’t have to worry about catering to Wall Street and their complete focus can be on running Berkshire as a business. I assume that in the next railroad sector crisis, Burlington will simply takeover a competitor on the cheap in typical Buffett style because it will have the leverage room to do so. It might not happen soon, but Buffett thinks in centuries, not years.

Burlington Northern Santa Fe as a standalone company would likely have a market capitalization of $200 billion and the capacity to take on approximately another $15 billion of debt very easily.

Berkshire Hathaway Energy – $70 billion

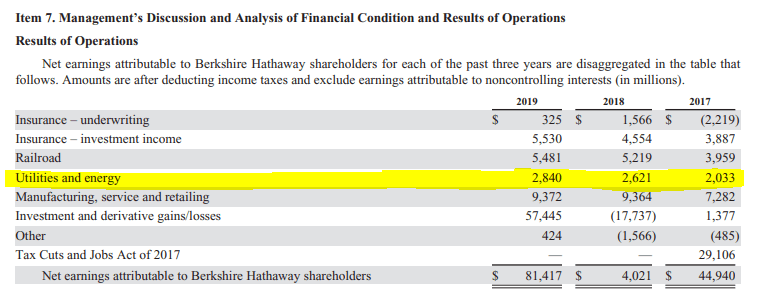

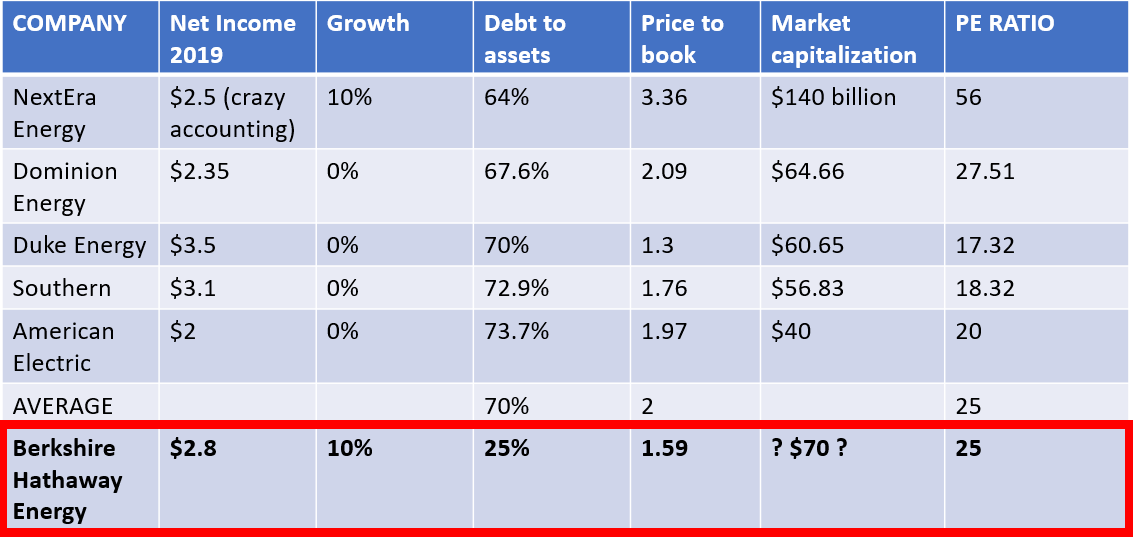

Berkshire Hathaway Energy 2019’s net income was $2.8 billion.

Berkshire Hathaway Energy is specific because it doesn’t pay out any kind of dividends as it reinvests all the profits in order to increase growth. They can still find investments that lead to 8% to 10% returns in the sector and therefore they keep reinvesting. Consequently, net income grew from $2 billion to $2.8 billion since 2017. Therefore, when pricing BHE we have to also include the 10% growth rate into a valuation.

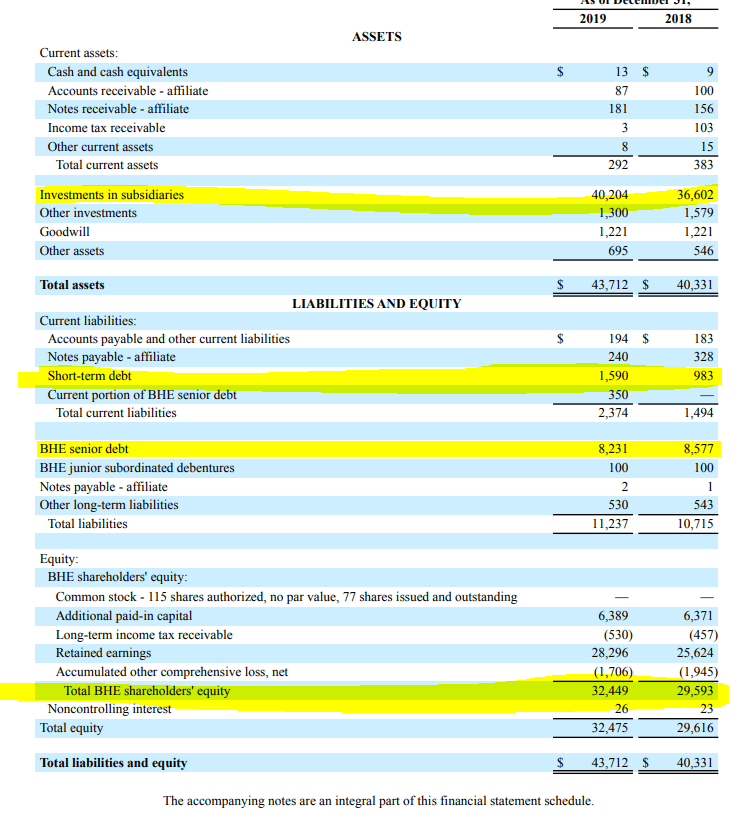

A look at Berkshire Hathaway Energy’s 2019 balance sheet confirms how Buffett likes to manage his companies conservatively. No dividends are paid out so the net income increases shareholder equity, the number of shares outstanding is just 77 of which Berkshire owns 70. The long-term debt is $8.23 billion where total debt to assets is only 25.7%.

The above, unlike the case with BSNF, is in line with what reported in BRK’s annual report.

Let’s see what would Berkshire Energy be worth as a standalone company. Perhaps the best proxy is the U.S. Utilities ETF (IDU).

The top 5 holdings for IDU are NextEra Energy (NEE), Dominion Energy (D), Duke Energy (DUK), The Southern Company (SO) and American Electric Power (AEP).

I have taken a look at net income for the above energy companies where I tried to adjust it for all the crazy accounting that goes on there by simply taking into account operating earnings and deduct interest and taxes as other related accounts are volatile. I apologize for any mistakes, the goal is not an analysis of the specific energy company but to get an idea of what BHE might be worth. Other metrics that I compared are total debt to assets, price to book and the price earnings ratio.

I think BHE deserves a valuation of 25 given its debt levels are extremely low and it is still growing at 10%. NextEra Energy is a special situation where I got dizzy just trying to grasp the accounting to get to a plausible net income.

With a PE ratio of 25, BHE’s market capitalization would be $70 billion. From a debt perspective, to reach the average energy sector debt to assets ratio of 70%, BHE would need to borrow an incredible amount of $60 billion. By borrowing another $60 billion, total debt would be $71 billion while assets would be $101 billion. This shows how much fire power is Buffett still having that goes way beyond the huge cash pile Berkshire has.

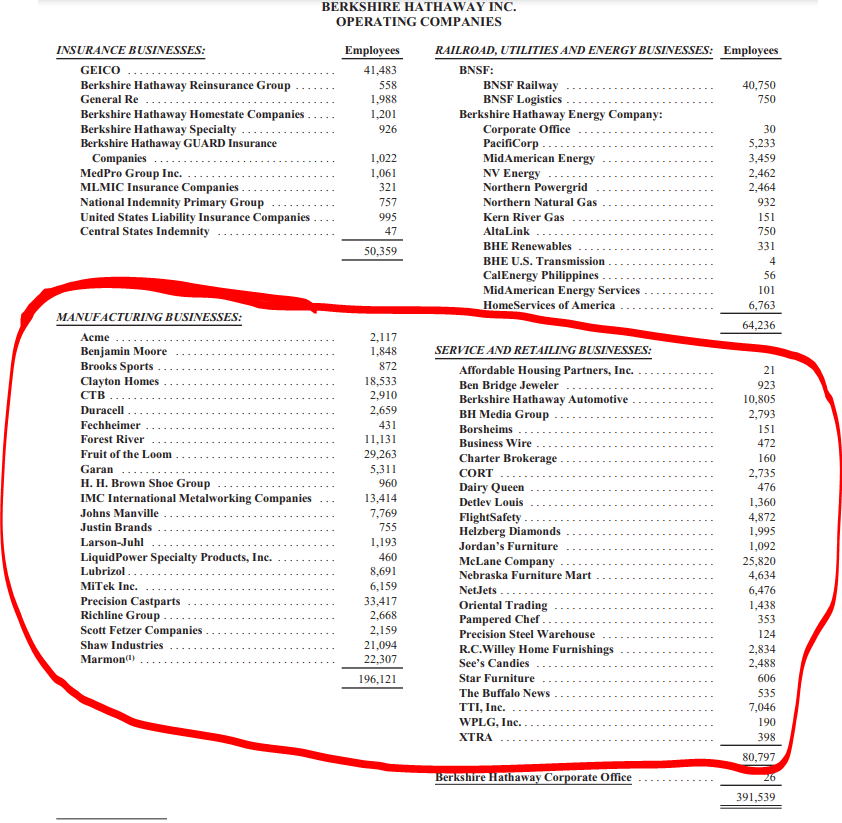

Manufacturing, service and retailing – $180 billion

Manufacturing, service and retailing includes various companies of which I am sure you have some products in your home.

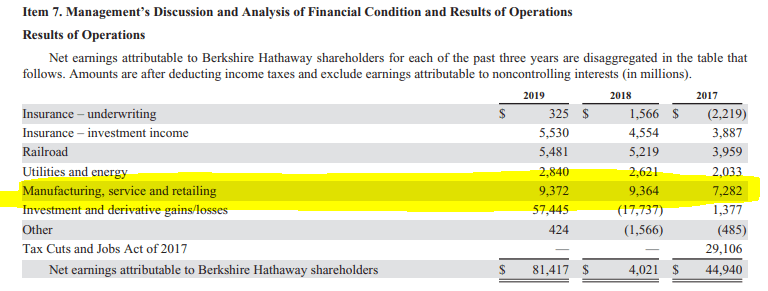

Net income from those companies in 2019 was $9.3 billion. If we attach a valuation of 20, the value of those companies would be $180 billion.

These subsidiaries have long-term debt of $30 billion with an average 4.5% interest rate. Given the $9 billion net income level and the $1.37 billion of interest costs, BRK’s subsidiaries have also much room to leverage up if needed.

This is a good place to add BRK’s other debt to the picture, $37 billion isn’t much.

Other liabilities are all under the insurance part of the company.

The value of the manufacturing, services and retail companies should be at least $180 billion.

Berkshire’s stock market portfolio value – $227 billion

This is the easiest part of the calculation. As of writing, the Berkshire portfolio tracker gives a value of $227 billion.

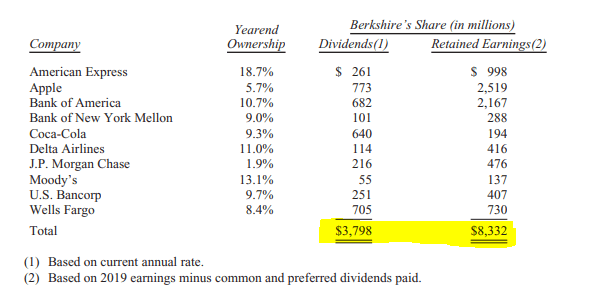

The earnings of the top 10 positions are $12 billion when considering the $3.79 billion BRK gets through dividends and the $8.3 billion in retained earnings. The market is valuing this basket of stocks with a price earnings ratio of 19. Thus, the price earnings ratio of 20 that I applied to BRK’s other holdings seems fair.

The above $8.3 billion are hidden earnings because not reported withing BRK’s financial statements. Something to consider when valuing BRK and you can read more about that here: Berkshire intrinsic value calculation.

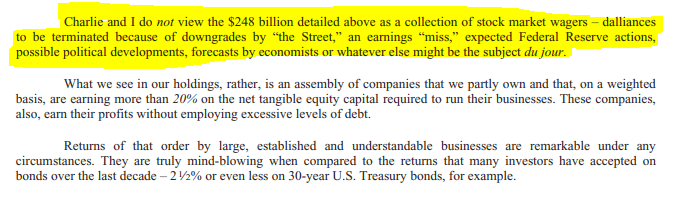

Another important note is that Buffett and Munger don’t see the stock market portfolio as stocks that go up and down but as stakes in businesses that deliver good returns on capital.

What is left to value is BRK insurance and the cash position.

Berkshire insurance – $25 billion

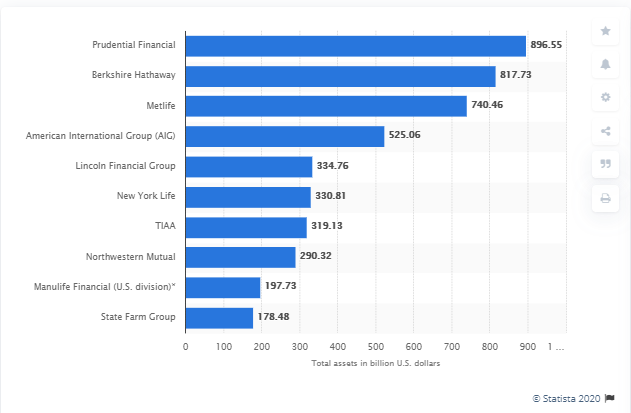

If I compare BRK’s insurance business to other insurance companies, Prudential’s market capitalization is $24.5 billion while Metlife’s is $33 billion.

The actual value, especially for Berkshire, is not in the insurance business, but in the accumulated float invested into stocks and other businesses that we already discussed. Insurance underwriting income was just $325 million in 2019 and Buffett often comments how he expects insurance income to be around zero over the long-term. The key with insurance is the growing float that allows for investment income. By renouncing insurance income, Buffett can get more business and thus a bigger and bigger float.

I would say BRK’s insurance operations could be valued like the other insurers at $25 billion. This excludes the stock market portfolio that we valued above.

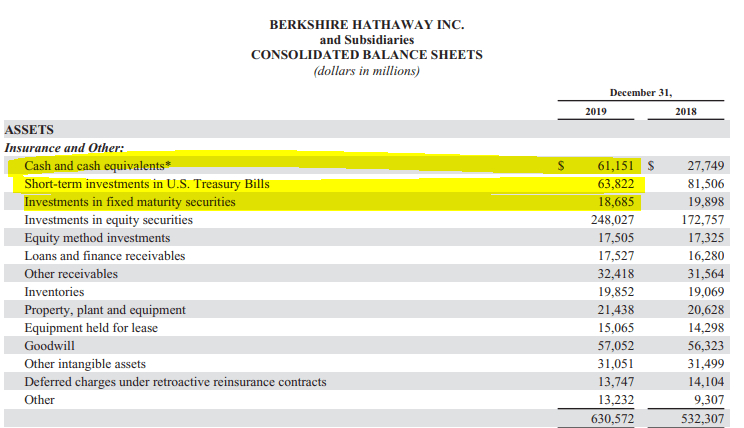

The final thing left to do is to value BRK’s cash. One might say that is easy but the question is how much of it is really free cash to be used at will and how much is it needed for insurance operations.

Berkshire’s cash position – $143.5 billion

Total assets on the balance sheet are $817 billion.

If I deduct all the insurance liabilities of $234 billion, the total $87 billion debt and tax liabilities of $65 billion I get to equity of $428 billion. If I deduct the $248 billion in stocks from that, I am down to $180 billion of value that should be free of any kind of liabilities and not represented by the stock market portfolio value. Thus, the $143.5 in cash and cash equivalents can be consider as value as Buffett can do whatever he pleases with that, even pay a dividend.

Berkshire Hathaway stock sum of parts valuation

In total, BRK’s sum of parts valuation from a market valuation perspective amounts to $845 billion.

- Burlington Northern Santa FE – $200 billion at least

- Berkshire Hathaway Energy – $70 billion at least

- Manufacturing, service and retailing – $180 billion

- Stock market – $227 billion

- Insurance – $25 billion

- Cash – $143.5 billion

This would make BRK undervalued by 40% when compared average market values.

If Buffett would leverage up to do buybacks like others are doing in corporate America, I would say the stock price could easily triple over the next 12 months! That something he will never do, but it gives you an impression on what you are buying and at what price when investing in today’s market and in Berkshire Hathway. As would Buffett say:

“Price is what you pay and value is what you get”.

The main question you have to answer is whether you want to buy value through BRK or buy something else that might be cooler because the stock price can go higher and higher due to buybacks and market exuberance, like it is the case with BRK’s competitors stock prices in the railroad and energy sector.