Berkshire Stock When Buffett Dies (Management Outlook)

I’ve recently made a Berkshire stock sum of parts valuation and, like it is always the case when I talk about Berkshire, the overwhelming number of comments were about what happens to Berkshire when Buffett dies or retires. Retires sounds better.

Given that Buffett built Berkshire over the past 50 years and recently turned 90, it is a genuine concern. In this article, I wish to share my perspective on the issue. I believe the 3 key factors to address in this matter are:

- What is Berkshire without Buffett?

- What is the expected business return Berkshire offers, is there a Buffett stock premium?

- Will Berkshire continue to be the opposite of Wall Street after Buffett?

Here is the video discussing BRK stock when Buffett retires, article continues below.

Berkshire after Buffett

I don’t think that when Buffett retires, people are going to stop transporting grain with railways, insuring their cars, enjoying Apple products, eating ketchup, drinking Coke or buying sweets at See’s Candies while paying with their American Express card.

I think this is an easy and simple answer to the first concern.

Berkshire expected return and BRK stock Buffett premium

As the businesses mentioned above will keep doing business, it is likely that Berkshire will keep making money. In order to see whether there is a Buffett premium related to BRK stock, we have to compare Berkshire’s earnings and valuation to the market’s valuation.

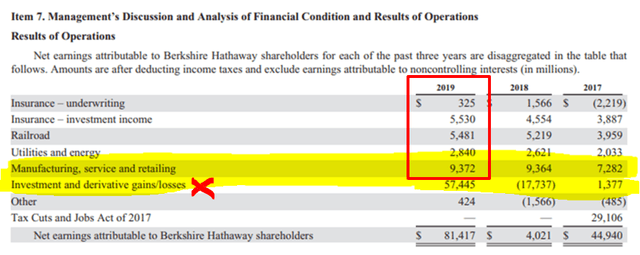

If I take 2019 as an example of a normal year and what we can expect from Berkshire long-term, business earnings were $23.1 billion.

I am not including the ‘investment and derivative gains/losses’ account because that is not a factor when it comes to business earnings. Buffett also said how we should disregard that account because it will be always extremely volatile as it depends on stock price fluctuations. What Buffett prefers is to look at the earnings of his stock market holdings, not the stock prices going up and down.

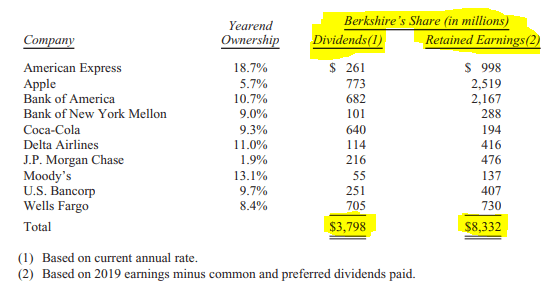

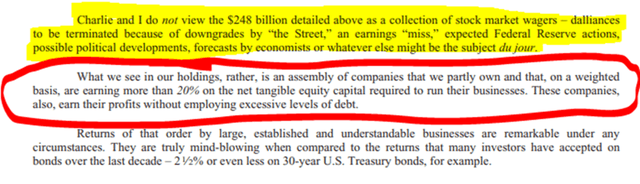

From its stock market portfolio, only the $3.79 billion paid in the form of dividends are included in Berkshires reported accounts, the other $8.33 billion that is Berkshire’s share in the respective holding’s earnings, are not reported anywhere but are extremely important. Those earnings are important because the companies can reinvest that money at an average return of 20% on net tangible equity, which means there is much more growth ahead.

I think the influence Buffett has on the above holdings and their returns on capital is minimal, so BRK’s stock market holdings will too continue to do business as usual.

Berkshire stock Buffett premium

As for the Berkshire stock Buffett premium, summing up the above $23.1 billion and the $8.3 billion of hidden earnings I get to earnings of $31.4 billion (the $3.7 billion of dividends are already included in the $23.1 billion under insurance investment income).

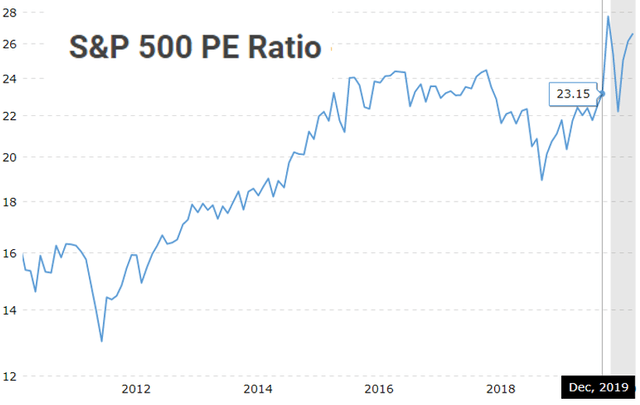

At a market capitalization of $501.6 billion, the price to earnings ratio for Berkshire in a normal business year would be 16. If I compare BRK’s 2019 PE ratio with the S&P 500 2019 PE ratio of 23.15, BRK is actually trading at a discount to the market, not at a premium.

Therefore, I would exclude a Buffett premium on Berkshire as there is actually a Buffett discount when it comes to BRK, probably because Buffett is about getting rich slow. Something that attracts only few these days.

The final question we have to answer is whether Berkshire will continue being a getting rich slow vehicle after Buffett?

Berkshire investing mindset after Buffett

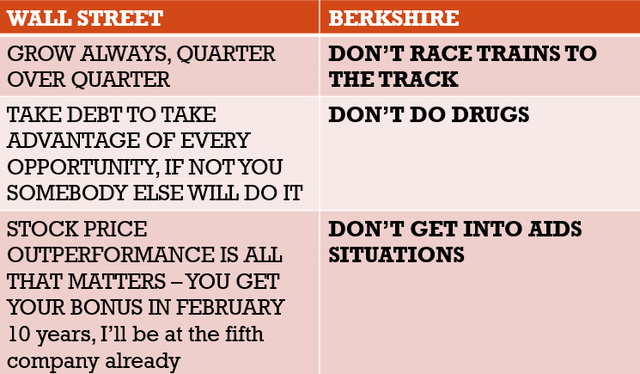

Berkshire will remain with the same mindset at least over the next few decades while Ajit Jain and Greg Abel are there. Berkshire’s mindset is simple, but its simplicity and contrast to Wall Street makes it hard to understand for many. I think Munger’s 3 advice on how to live a great life also perfectly explain what Berkshire does in confront to Wall Street.

Berkshire’s business and investing style can be summarized by saying that it goes forward by avoiding failure. Wall Street goes forward by taking on leverage, doing crazy acquisitions and buybacks just to grow at all costs.

Ajit Jain has been managing Berkshire’s insurance arm in a growing, but conservative way for long now and Greg Abel is doing the same with Berkshire Hathaway Energy. BHE is managed with low debt, earnings are carefully reinvested and the company is slowly but surely becoming bigger and bigger.

I am sure that those two, even when Buffett isn’t there anymore, will be able to keep doing deals in Berkshire’s style. Abel might take over an energy company in trouble while Jain will look at insurance companies when there is trouble in the sector. For Berkshire to strike, there needs to be trouble in a sector. In the mean-time, they will patiently wait despite the fact that Wall Street will call them names because of too much cash on the balance sheet.

Berkshire after Buffett investing summary

To sum up, I think one can expect a long-term investing return between 6% and 10% from BRK, depending on what happens in the economy and the opportunities they get to grow slowly.

That is a good return, especially given the fact Berkshire is made to last forever, made to be a financial fortress as Buffett likes to call it. I think Buffett has prepared everything that things continue to work in the future as those have worked in the past.

If you enjoyed this approach to investing, please consider subscribing to my newsletter for more analyses.