Shipping Investors Have Capitulated – Time to Invest – SEA ETF

Contents

Shipping’s terrible past investment performance – is it time to invest now?

Shipping investing thesis – without shipping there is no life!

Shipping investing thesis – high short-term upside

Risks when it comes to investing in shipping

My shipping investment strategy

Shipping’s terrible past investment performance – is it time to invest now?

Over the past decade, shipping stocks have probably been the worst investment out there. Many stocks went bust, some are down more than 90% and the Shipping ETF (SEA) is down 70% since its 2010 peak. Given that shipping stocks were even higher in 2007, the carnage is even worse.

Source: Yahoo Finance SEA

Here is the video for those who prefer watching videos.

There has been a rebound up to 2014, but then there was a sharp drop in prices up to January 2016 followed by a slow, but sure, capitulation where the SEA ETF has been steadily losing ground since 2017. Is it time to invest now?

Adding to the pain of the sector is the sector abandonment by investment banks. Six investment banks have closed their coverage on shipping stocks. This means that there very low interest from investors, not even to justify paying a few analysts to do research.

Source: Trade Winds

So, most investors have lost money over the last decade. Such a performance creates an environment where everybody has had enough, capitulated on all the bullish theses and there is absolutely no interest from institutional investors whatsoever. Only the die-hard investors, those that have been in shipping since ever, have remained. Is it time to invest now, at a point of total pessimism? Will pessimism lead to great opportunities? Is it time to be greedy when all others are not even fearful anymore, but simply crossed shipping forever? Well, let’s dig deeper, after all, without shipping, there is no oil, steel, grain, and consequently 99% of the things we enjoy!

Shipping investing thesis – without shipping there is no life!

Investments like Amazon, Google, Facebook, Apple have all done great over the past decade. But you can live without all of them and you probably did live without them just 10 years ago. Well, you can’t live without shipping as it transports the food you eat, the oil you consume, the metals we use, fertilizers, cars, and many other things that we can’t even think of. The following is an illustration of where do smaller vessels navigate across the globe.

So, without shipping, the world would stop. Let’s see whether we can make any money on it.

It is normal that the shipping industry works in cycles. When shipping rates are low, there is not much interest and the number of ships built is smaller. This should lead to a ship supply crunch that should lead to higher prices. Consequently, higher prices lead to more ships being build, more supply and again, lower prices. Thus, shipping is a typical cyclic industry.

The main problem when it comes to investing is that there is absolutely no competitive advantage. If you make money, somebody else will see it, built a new ship, probably a better one than you have, and try to eat into your profits. Low interest rates allow for easy financing and therefore the competition is fierce.

A company like Maersk, that is the global leader in the business, has had a return on invested capital of just 2.2% in over the first half of 2019.

Source: Maersk Investor Relations.

A bad environment leads to low dividends that further pushes investors away. But, as smart investors, we have to look forward not backwards, this gives us an advantage over others.

The following presentation chart from Golden Ocean (GOGL) shows what are the risks and rewards when it comes to shipping. Companies could do well if there is more stimulus and continued growth in China, if the new fuel regulation (IMO 2020) increases costs and if more older vessels are scrapped (happens only if fares are low which is again a negative). On the risk side, a global recession would create an oversupply situation and put most shipping companies into negative earnings territory. Further, the world might also be changing, it is expected that we will need less coal (depending on China and India), less oil in the future and less of those things that made shipping strong over the past cycle.

Source: Golden Ocean

Shipping companies have a positive view and invest consequently. Therefore, the increase in shipping supply is always close or higher than demand. In such a situation it is hard to make money.

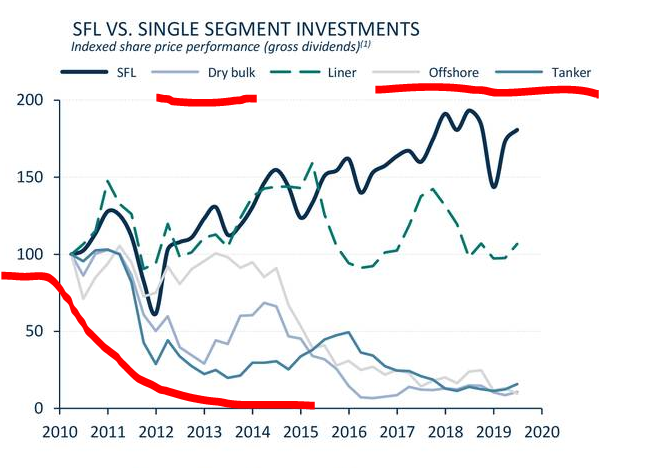

Some sectors are hit more than others, and dry bulk (transporting commodities), offshore oil drilling and tankers have fared the terribly since 2010, also thanks to the oversupply in the late 2000s. Only liners did ok but that is still a terrible performance compared to the S&P 500.

Source: SFL investor relations

And the negative returns happened despite the fact that global trade volume grew over the past 10 years alongside GDP growth.

Source: Clarkson PLC

A positive thing to keep in mind is that if emerging markets continue to grow and reach developed country levels, demand for commodities etc. will grow extremely high and shipping should do well if they stop building that many ships.

Source: Clarkson

But this is the long-term environment, the short-term shipping investing thesis is interesting. Plus, when it comes to shipping, you make your money in one year and make up for the 4 years you broke even or lost money. All you need to do is to get into the sector before the good years start as those will not last long.

Shipping investing thesis – high short-term upside

There is a convergence of positive factors the industry is promoting; less ships coming into the market, new fuel regulations, slower speed for environmental reasons and longer shipping routes. I’ll use the oil sector example but it applies to other sectors too.

Everybody in shipping would love to see regulation about lower speed. This would suddenly create the need for many more ships and the actual effect on the environment would actually be the same. In the mean-time, those owning ships now would make a lot of money.

Source: Splash

Due to the negative sentiment, there are fewer ships entering the market as there is no regulation about speed yet.

Source: Clarkson Tankers Presentation

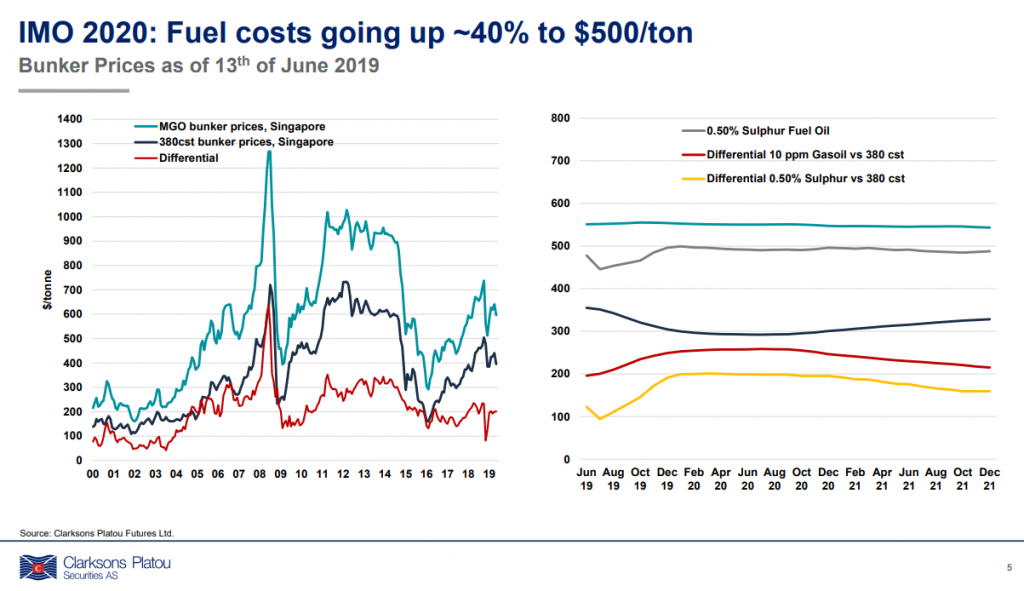

The level of sulphur in fuel has to be below 0.5% from 2020, instead of the current 3.5%. Companies can either buy more expensive clean fuel or install expensive scrubbers that cost between $2 and $5 million per ship. So, cost of doing business should go up but also many ships should be offline while the scrubbers are being installed. Those with new, fuel efficient, ships should have an advantage.

Source: Clarkson Tankers Presentation

Plus, as the US is producing and exporting more and more oil and related products, ships have to travel longer to brink the product where it needs to be.

Source: Clarkson Tankers Presentation

If there is more demand for ships than supply, prices spike and that is why you want to invest in shipping, because when prices spike, the shipping sector makes a lot, a LOT of MONEY. For example, if charter prices increase from the current lows, to the 15-year average, a company like International Seaways (INSW) that is currently trading at $19 per share, would make $4.46 in earnings in a year. That is a PE ratio of just 5 for a historical average. If prices jump to the 2008 peak, the company could make its current share price in one year of earnings. That is the promise that shipping stocks are selling today.

Source: International Seaways

However, we also know that the above doesn’t have to happen.

Risks when it comes to investing in shipping

DryShips is an excellent example of how shipping works. The business didn’t do well over the past years and now, when most is lost, the CEO will simply take the company private and tell you good bye at a miserable price compared to past levels. So, if you invested in the company, averaged down, the CEO just took all your possible upside. Knowing shipping, there is always huge possible upside.

Further, investors in Frontline (FRO) didn’t do really well over the past decade. But the majority owner, Friedriksen, still holds a big chunk (42%) of the company and the market capitalization didn’t change much. It was $2.3 billion in 2006 and now it is $1.8 billion.

Source: Frontline Market Cap

The stock price did terribly.

Source: Frontline Stock Price

A good thing to watch is the corporate governance ranking. Be sure to assess the management’s intentions properly.

Source: Ardmore Shipping

Another problem with shipping is that ship owners understand the risks of the business and they know they should never have all their eggs in one basket. So, they always diversify and they always keep a lot of cash aside so that they can buy on the cheap when possible. Further, they prefer to play with other people’s money than with theirs, if possible. The thing is that when things turn bad, it quickly becomes a very negative spiral. If you have debt, you probably have debt covenants. You usually breach them only when you don’t have money and exactly at that point, your creditors usually ask you for more money. Usually also the best time to dilute existing minority shareholders and own more for less.

Source: FLEX LNG Anuual report

So, before investing in shipping, keep in mind that the environment is and will always be crazy.

My shipping investment strategy

As a value investor, it is hard for me not to look at shipping currently. So, I have now gotten an overview of the sector, I will now look at 7 stocks that I picked from my list of stocks that I researched. Then, I’ll cover the 3 most interesting and when there is a real great opportunity for 1000% upside with, as always, 100% downside or hopefully less, I might invest.

For now, there is a little bit too much optimism in the industry so I’ll wait for IMO 2020 to pass, for a global slowdown, and then look for my picks.

Nevertheless, tomorrow I’ll give you an analysis of FLEX LNG, that is in a positive sector with LNG and well positioned to take advantage of long-term trends.

Before you even start thinking about investing in shipping, I strongly suggest reading two short novels, by author Matthew McCleery, an expert on shipping. ‘The Shipping Man’ and ‘Viking Raid’, in that order. Aside from being funny and enjoyable they will tell you, everything you need to know about the industry.

In short, the following is what we need to look at:

Moving parts when analysing the shipping industry:

- Overcapacity, depending on global economic growth, can make prices go down.

- Shipyards backlogs

- Fuel costs (IMO 2020 implementation)

- The shipping war – competition and lower costs

- Technology and development – automatization

- Age of ship and cost advantage

- Amazon shipping (sea vessels, not prime)

- Blockchain technology

- Climate change, new versus old routes – Panama, Arctic

Factors to consider when analysing a shipping business:

- Market cycles for the specific shipping sector

- Liquidity of the company, debt levels

- Ownership and owner’s interest – limited partnerships are often horrible

- Freight and charter rates (spot or long-term contract)

- Ship size and location

- Daily running costs

- Fuel (bunker) costs

- Cost of building ships, selling price of ships, designing ships

- Scrappage value of ships

- Debt covenants

- Competition

If you enjoyed this shipping overview, please subscribe as I’ll publish a few of my shipping stock analyses.

Disclaimer:

The opinions expressed – imperfect and often subject to change – are not intended nor should be taken as advice or guidance. The Sven Carlin Stock Market Research Platform is not an investment advisor or financial advisor. The Sven Carlin Stock Market Research Platform provides research, it does not advise. The information enclosed in this article is deemed to be accurate and reliable, but is not guaranteed by the author.