Copper Stocks Investment Thesis (Risk & Reward = When To Buy!)

Investing in copper

Investing in copper is done through investing in copper mining stocks or a copper ETF. With copper miners it all depends on copper prices. But, each copper mining business is different and the key is to understand the sensitivity the stock has in relation to copper prices and other issues related to the specific business.

This article will discuss the main demand and supply forces driving copper prices, the current situation and outlook which translates into a risk and reward investment thesis to conclude with the key factors to watch when considering investing in copper miners.

Here is the video discussing the copper thesis that also includes, as and copper stock analysis and example, the FCX stock investment thesis. Copper article continues below.

I am bullish on copper for the long-term

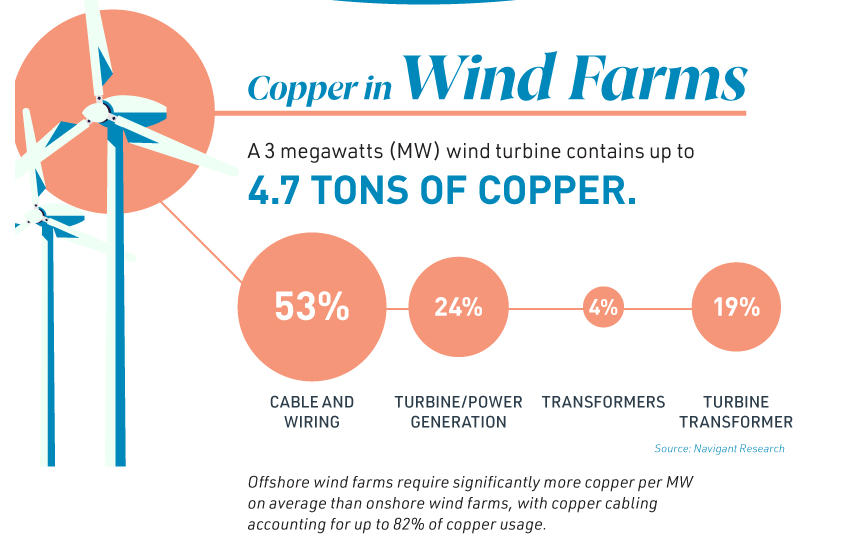

I am bullish on copper prices long-term and not because of the reason everybody else is currently bullish on copper, which is renewables. Even if renewable related copper demand doubles in the next 10 years, that would still just add 0.8MT to global demand, or 3.3% of the current demand for refined copper which is 24MT.

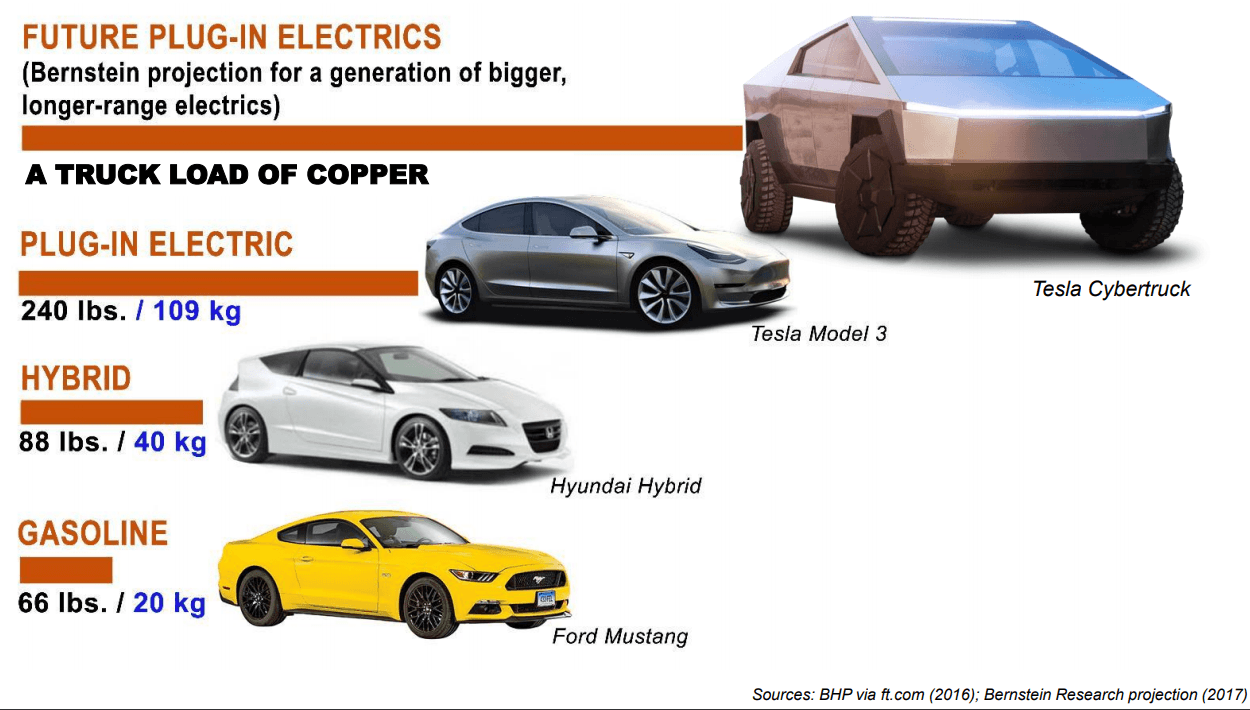

Some say electric cars will increase demand for copper, but that is also a long shot because the current share of automotive demand for copper is 6.6%. If that doubles by 2040 on more electric cars, it is again just 1.5MT added to demand, not that significant over a decade or two.

My bullishness on copper and why I see a strong tailwind for investing in copper, comes from the growing global middle class. 51% of copper consumption comes from construction and infrastructure and as the middle class grows, there will be more need for those and other things that make middle class living.

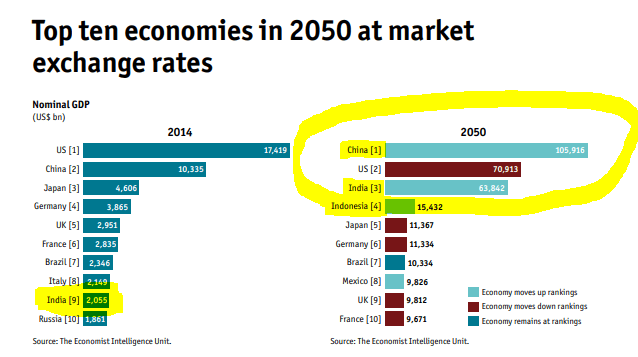

The Indian economy is expected to be 30 times bigger by 2050, which means much more demand for copper.

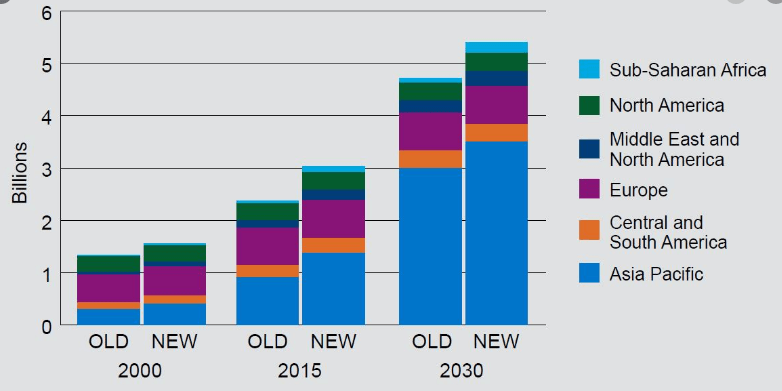

Plus, as it is expected that the current middle class grows from 3.5 to 5.5 billion by 2030, if they buy only one item of white goods, that is 2MT added to copper demand, not even considering other copper demand sources.

Middle class demand for copper is the key long-term driver, if they also buy electric cars, even better. But, be careful when it comes to the ‘green economy’ and businesses, most will shout about it, but as a friend of mine once said: “A CEO is a salesman first, then everything else”. Copper miners are all selling the renewable story now. 5 years ago, the easiest story to sell was global growth in combination with low supply growth based on little or no new deposits found. Unfortunately, reality is always far below projections. A good thing to always keep in mind.

Always take the projection of a miner with two grains of salt.

So, the long-term outlook for copper is positive. However, one must not forget that there is plenty of copper out there and that supply will follow demand over the long-term.

China makes 51% of global copper consumption, so the transition towards a service economy there, is what pulls copper prices and forecasts down. Consequently, copper prices are extremely volatile. China’s 51% demand for copper is 10 times more important than all the renewable and electric vehicle related demand.

Copper price analysis

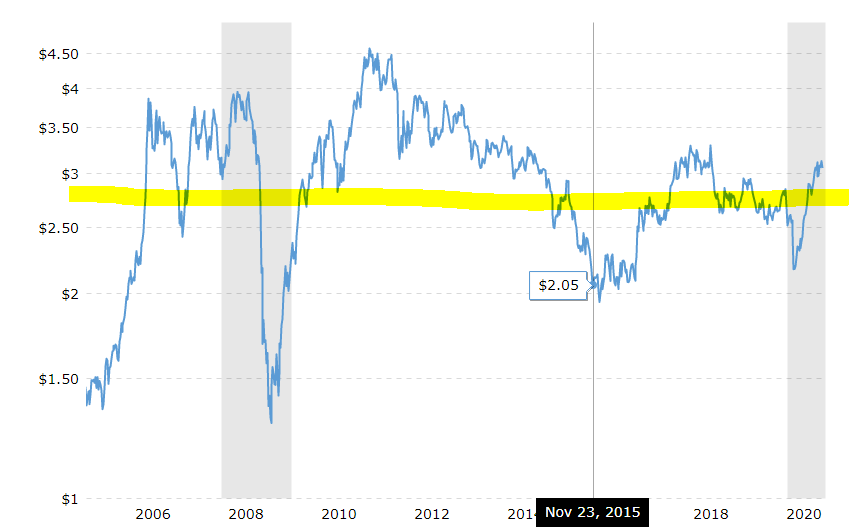

Copper prices are currently at $3 and where copper prices go next depends on the short-term supply demand situation. Over the past years, there were many new copper mines that had been launched when copper prices were close to $4 in 2011. These mines have increased supply and created downward pressure.

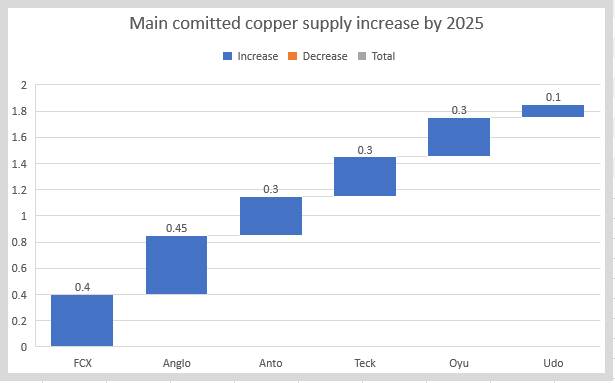

Given the current economic situation, the expected growth in supply of at least 2.8MT by 2025, I don’t see copper prices exploding soon. The figure below shows the main contributions to supply that don’t include the 1MT SCCO should add by 2027 and other big projects that might be ramped up by then. 2.8MT growth is almost 15% of current mine supply and I don’t think demand for copper will grow at 3% to cover for the already committed new supply.

Main copper supply growth sources – Source: Sven Carlin Research Platform

I see copper trading in a range between $2.5 and $3.3, possibly going down to $2 in bad times which will likely come again given the current economic situation where the things that really matter are totally neglected.

Understanding the forces driving copper prices is key for understanding the risk and reward of investing in copper mining stocks. Copper will always be a cyclical industry which means the only think you can count on is volatility. The best investment strategy in such an environment is to buy low and sell high.

That is of course easy to say, but the fact that the long-term outlook is positive, means that one can be relatively sure about demand picking up after bad times, which creates low risk and high reward investment opportunities.

Investing in copper mining stocks

I have looked at every copper miner out there and my conclusion is that one has to see how each miner fits one’s investing strategy. The things to look at are:

- Production outlook, life of mine,

- Production costs

- Sensitivity to copper price changes

- Jurisdiction

- Debt

- Free cash flow yield and long-term valuation

- Issues: accidents, lower than expected grades or harder ore, strikes, taxes, legal issues, environment etc. Will always go bad at some point in time, be sure to price it in!

The differences in specific mining companies, where all have individual issues and risks, makes the sector extremely variegate with free cash flow yields going from 5% to the high teen ranges for some. I show below an excerpt from my analysis and you can see how the market likes low cost, low debt, long-mine life and strong jurisdictions. The better the company, the higher the price and lower the cash flow yield.

The above volatility is something you must take into account when investing in copper mining stocks. There are two ways to approach this:

- Having a portfolio exposure strategy

- Being patient by waiting for the fat pitch

Copper as part of portfolio strategy

Given the positive long-term trends for copper, you could set a fixed portfolio exposure to copper that makes you sleep well. As copper stocks will certainly be volatile, every time the portfolio exposure increases by 50%, you can sell the gains and bring down the exposure to the initial level.

If stocks fall 33%, you can buy more and bring the exposure back up again. Given the environment, you will surely be buying low and selling high which is usually a very good tactic when it comes to investing. Also, by focusing on portfolio exposure, you’ll surely avoid the dangerous exuberant situations and force yourself to buy when things look really ugly, which are usually the best time to buy copper stocks.

An example of having COPX or a copper mining stock as a fixed part of your portfolio where you play on the inherent volatility on the strength of the long-term trend.

Waiting for the fat copper pitch

My personal strategy is to wait for copper mining stocks to reach a level where the long-term downside risk is minimal and the upside maximal. For example, the current downside for COPX is 50% or more and the unlikely upside is 100%, but only in case of a rally in copper prices.

I think that with copper at $2.5, some delays with the projects ramping up, COPX could easily fall 50%, which would create a situation where the long-term downside could be practically zero while the long-term upside could be minimally 100%. If you like such a strategy, please consider following.

If you enjoyed this analysis and would like to have me follow the copper environment for you and notify you when the time for the fat pitch will come, please check my Stock Market Research Platform where the focus is exactly on that.

If you wish to learn more about what I do and get an email when I publish a new interesting stock or sector analysis, please subscribe to my newsletter.