Altria Stock Analysis + BTI and PMI + Tobacco Industry

Contents

Altria stock analysis and fundamentals.

Reason for stock price decline.

BTI stock – British American Tobacco

Among the top 10 requested stocks to analyse over the last year were definitely Altria (NYSE: MO) and British American Tobacco (BTI). The reason is simple, we have declining stock prices and strong looking fundamentals. This article will explain what is going on and why is the market pricing these companies in a certain way by looking at MO, BTI and Phillip Morris International (PM).

Source: CNN Money – Altria Stock Price

Source: CNN Money – BTI Stock Price

Stock prices had done extremely well over the past decade, up till 2018.

Altria stock analysis and fundamentals

Let’s first discuss the fundamentals, which have been improving at first sight.

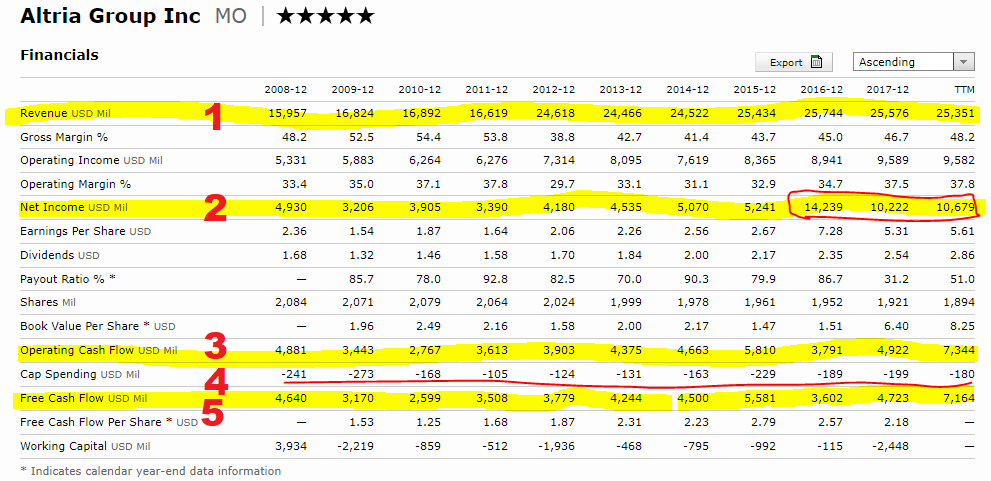

Altria’s fundamentals look excellent. Revenues are up over the last decade, albeit stable for the last 7 years (line 1), net income had been stable but exploded in the last 3 years (line 2), operating cash flows have been constantly positive and significantly increased in the last 12 months (line 3) while capex spending is minimal (line 4) which leaves plenty of room for high free cash flows (line 5).

Source: Morningstar MO Key Ratios

The just mentioned positive fundamentals translate into high shareholder rewards in the form of higher earnings, higher dividends and higher buybacks.

Source: Altria

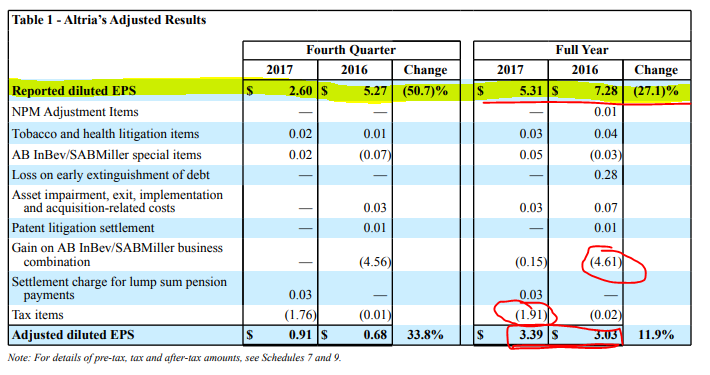

However, we have to understand that the recent years earnings have been skewed by special items. Altria’s EPS in 2017 was $3.39 when adjusted for special items. The reported earnings per share were higher in 2017 due to tax items that increased earnings by $1.91 while earnings in 2016 were higher due to the gain on the AB InBev/SABMiller business combination.

Source: Altria

The actual earnings for the company have been $3.03 in 2016, $3.39 in 2017 and are expected to be between $3.95 and $4.03 in 2018. This means that the adjusted average PE ratio (using 3 years average earnings of $3.47) on the current stock price of $50 is around 14. The price to book value is 6, so one has to focus on the cash flows and book value is not really significant.

Reason for stock price decline

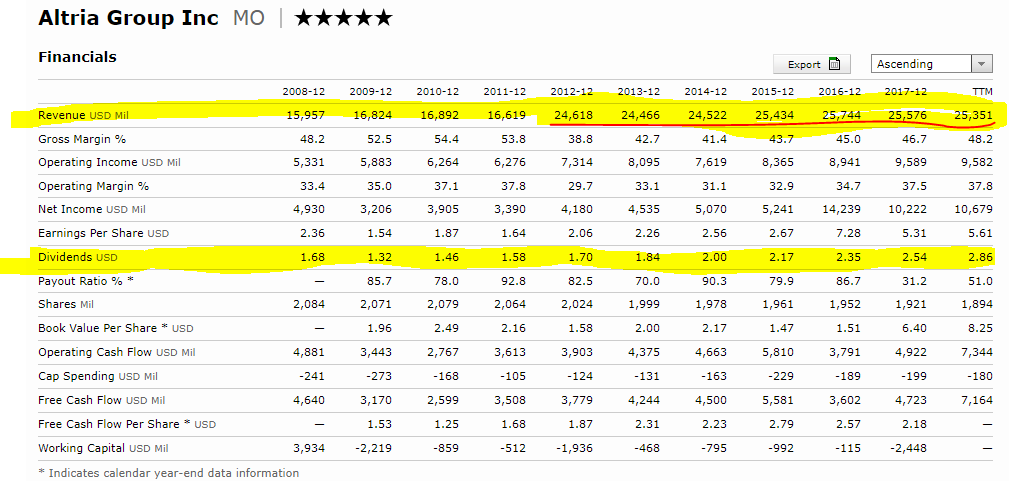

A company in a declining or stable sector is usually called a cash cow and cash cows are often looked at as you look at bonds, or even worse, annuities. If we look at MO’s revenue and dividends, it will give a better picture over what has been going on. Revenues haven’t been growing lately but dividends did grow over the past 10 years.

Source: Morningstar MO Key Ratios

The dividend is $2.86. On the price of $50 it gives a yield of 5.7%, a very good yield. The forward yield is at 6.5% as the dividend is expected to increase further. So, what investors expect from MO, is a stable dividend for as long as it lasts as smoking is slowly getting out of fashion.

Tobacco business overview

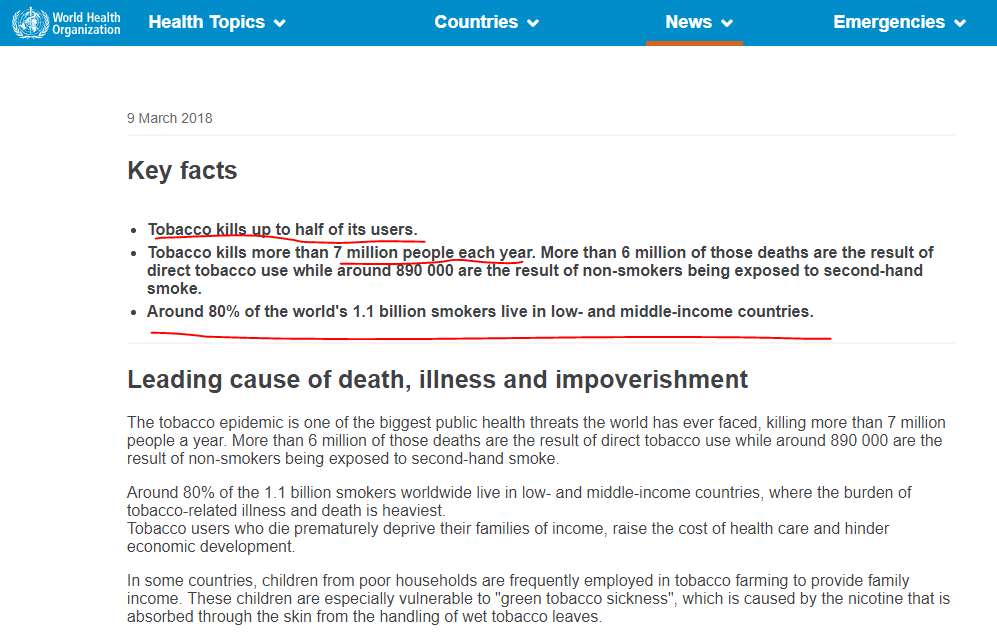

We cannot say the sector is in a positive trend, actually it is an industry that kills its customers.

Source: WHO

The trend is actually pretty clear when it comes to cigarettes consumption. Other threats are the FDA regulating nicotine in cigarettes, taxation, litigation, goodwill impairment, tobacco prices and who knows what ghosts can come out of the closet. I always urge investors in any company, to read its Risk section in the annual report. A quote from Altria’s 2017 annual report:

“Legal proceedings covering a wide range of matters are pending or threatened in various United States and foreign jurisdictions against Altria Group, Inc. and its subsidiaries, including PM USA and UST and its subsidiaries, as well as their respective indemnitees”

Source: World in data

What makes this comparable, but different than a bond is the value at maturity. You expect to get your principal in full from a bond, with MO, you don’t know whether you will get a principal or how big it will be. Therefore, it is all about the cash flows. The value of an asset is the discounted sum of its future cash flows.

Discounted dividends for MO

Let’s assume that dividends grow by 9% over the next 6 years, are flat for the following 4 years and then start declining by 10% per year. This are the cash flows an investor could expect over the next 20 years.

Source: Author’s estimation

The 2037 dividend will be $1.79 in the above case to which I can attach an expected yield of 10%, as the dividends are declining, that would give me a 2037 stock price of $17.9. What we have to do now is to discount the future cash flows to the present value and sum up those values. When we compare it to the stock price, we get the net present value.

At a 5% discount rate, which is extremely low for stocks, the present value of the stock is $50. At an 8% discount rate we are at $39 while at a 10% discount rate we are at $33. To invest in Altria and other tobacco stocks, you need only two things, estimate their future cash flows, discount them to a present value by using your required rate of return and then compare to them to the price. That is what you can do, but what the market does is usually a bit different.

The key when discounting future cash flows is what discount rate to use. The usually used rate is one that puts a premium on the risk-free rate, which is usually US Government Treasury rate. If I take the yield on the 10-year Treasury note over the last 5 years, it had been declining up to mid-2016 and since then it has been going up mostly.

Source: FRED

If I put a 300-basis points premium on a required dividend yield from a company, the required dividend yield in 2016 would be 4.8%, while in 2019 it would be 6%. Usually, when yields are low, even the spreads between the yields are low. So, I could add 200 basis points on the 2016 yield and 300 on the 2019 yield. We have then an expected yield of 3.8% in 2016 and then, due to the increase in the risk-free rate, it suddenly jumps to 6%. This is extremely important to understand when looking at cash cow companies like Altria. It firstly impacts the present value of the future expected cash flows and secondly, it changes the expected dividend yield.

If I keep a constant dividend of $3 for MO, when the market expects a 3.8% dividend yield, the price of the stock will be $78.94. If the markets require a 6% dividend, the price of the stock will be $50. Such things are never linear, but MO’s stock declined from $70 in 2016, went even above $75 in 2017, to the current $50. In line with the higher expected market returns due to higher interest rates.

Source: CNN Money – Altria Stock Price

This is what explains the pressure on the stock over the last 3 years on top of all the other issues.

The business

Then, apart from milking the cow, sometimes the management decides to do something exciting, something they maybe had to do earlier. They buy a competitor, or just part of it. MO announced paying $12.8 billion for a 35% stake in JUUL, the U.S. leader in e-vapor. The problem is that the deal is at 33 times sales, financed by a loan and focused on growth.

Source: Altria’s JUUL rationale

Investing in a growth business, increases the uncertainty for future revenue or profits, but increases the certainty on the $14.6 billion of debt.

Source: Altria’s JUUL rationale

Apart from purchasing a stake, a stake, not the whole companies, MO also bought a 45% stake in Cronos, a cannabis company for $1.8 billion.

Suddenly, on top of the yield contraction, the company is turning into growth in a desperate move to counter the negative trend in its sector.

BTI stock – British American Tobacco

Similarly to MO, BTI declined too over the last 3 years.

Source: CNN Money – BTI Stock Price

However, the decline is much bigger due to the risk of a menthol ban in the US that gives 25% of profits to BTI.

On top of that, BTI, has a big debt issue as it quadrupled its debt in the last 10 years.

Source: Morningstar

The debt is why BTI stock declined more that MO. Debt is a certainty, and when you acquire other companies by using debt, you are always buying at a premium in an uncertain world. And such an acquisition is the perfect example of what I’ve been discussing. They bought Reynolds at peak tobacco where the debt will remain at peak and interest rates have been going up while industry headwinds are getting stronger. This is a perfect example of short-term management thinking taking into account current interest rates, current premiums and current earnings not caring that those all change. Usually debt costs go up and earnings go down.

However, this is also in line with the prevailing strategy for tobacco companies over the past decades that focused on acquiring other smaller players. Such a pyramid strategy works well until it doesn’t.

Source: Bloomberg

Actually, over the past 5 years, BTI has been the worst performer.

Philip Morris International

PM stock is also under pressure and close to 7 year low.

The fundamentals look good and the dividend is also high.

Source: Morningstar PM stock

The interesting thing here is that cigarette volume sales are actually declining between 1 and 2% per year. The question is, like with the other stocks, what will happen which leads us to the investment strategy and whether tobacco stocks are a bargain?

Are tobacco stocks a bargain?

Well, that depends on you, what return do you want and who are you competing against?

When analysts are positive, pension funds check their target, they have to be invested and diversified and they buy as they have the money and must buy things. Further, it also depends on interest rates. When those are low, tobacco stocks look very attractive as any kind of yield is amazing. When yields are higher, then a declining industry is not so attractive and be careful not to jump into the growth trap.

If you are invested or interested in investing, you have to approach this from a scenario perspective. Nobody knows how will the environment look like in 10 years, if earnings are above expectations, interest rates etc, stocks will do good, if earnings go below expectations, dividends are cut, stocks will suffer. And here is the problem, you cannot know what will be the tax rate in 2024, you cannot know whether there will be a menthol ban or not, you cannot know what will other countries do and you cannot know what will the cannabis or vapor industry look like in 10 years.

So, now that I have welcomed you to the world of investing, one has to look at all these “cannot knows” and see about an investing strategy. My key message is to look at the future and then invest, I know the dividend is attractive, but think what happens and how you would feel if the dividend goes from 6% to 8%, then to 10% and consequently to 12% due to the stock price declining? What would you do and how would you feel? Let’s compare this in an example.

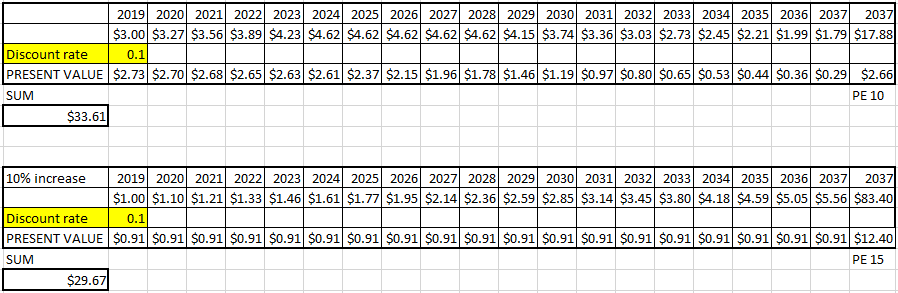

Source: Author

If I sum up the present values of a stock with a $3 dividend, like the one we used with MO at a 10% discount rate and a PE ratio of 10 after 20 years to a stock that pays only $1 in dividends now, but growths that dividend at 10% over the next 20 years, the present value is similar.

So, the question is what you want and whether you can predict dividends in the future? Try to do such comparisons for as many stocks as you can, compare tobacco stocks to others, and if tobacco stocks come out on top of the hundreds you compared in a good, bad and neutral scenario, then you invest.

On a price of $50 – a dividend of $1 is 2%, a dividend of $3 is 6%. But the present values aren’t much different if one is my MO case and the other growth its dividend by 10% over the next 20 years.

My opinion

Now, if I take risk, in this case in the form of FDA, regulation, negative trend, interest rates etc. I want to be paid for it. That’s it. I personally think that across the globe, you can get equal of higher yields in growing industries, with much less regulatory risk and much less pressure and much less baggage.

For full disclosure, I did invest in tobacco when I was a kid, I think 2009 and 2005 or something like that. But, I was just buying a 3.5% yield, no debt and net cash. I would buy 20% under cash per share and sell 20% above cash per share. The company was Tobacco Industry Rovinj from Croatia. I called that compensation for passive smoking as a kid. Later the company got acquired by BTI.

So, my personal message is to simply compare what are the risks you are taking in comparison to the dividends you are getting. For example, a completely different story, but perhaps a bit more positive trend over the next decades can be found with Daimler.

Source: Morningstar – Daimler

The dividend yield is even higher, and in 20 years people are more likely to drive cars than smoke. So, it is as always, up to you to see how what fits your portfolio. What will happen to the stocks mentioned short term? Let’s leave that to speculators and media, we focus on investing here.