Ingredion stock analysis – 10% yield

Summary – Ingredion

The operating cash flow yield is 11%, the company expects to grow earnings at 8% per year over the next 4 years, the PE ratio is just 13 for such a growth story, the cash flows are strong, it is a defensive stock and the returns might be substantial for investors over the next few years.

The company operates in two segments; one is a commoditized, low margin starch and sweetener production while the other is specialty ingredients that bring high margins and growth. It is important to keep the two separated when analysing the company as the market might miss the big picture.

Contents

Introduction – Lamb Weston Holdings Example

INGR’s potential business growth

Current situation with Ingredion

Introduction – Lamb Weston Holdings Example

When it comes to food stocks, if you can find a company that will grow thanks to more food consumption and won’t be hit by volatile food prices, you might have a winner. An example is Lamb Weston Holdings, Inc. (NYSE: LW) that is in the business of potatoes, mostly frozen fries.

LW is a ConAgra foods spin-off that did extremely well. Since the spin-off in 2016, the stock is up 112%.

Source: CNN Money – LW stock price

What did they do? Well, they invested in growth, had a nice return on capital, expanded margins and consequently earnings. Revenues were up 20% over the last 3 years, earnings 50% as there was margin expansion and the dividend increased too.

Source: LW Stock fundamentals – Morningstar

What they did is, acquired smaller players that allow for scale and expanded their own facilities. So, the above is something to look for when looking at such growth, niche food stocks.

Just an ending comment on LW, potato prices are increasing and 2019 earnings are already expected to be lower so a PE ratio above 22 is a bit risky for me and what is a bit expensive is a free cash flow yield of just 3%. I prefer higher yields if possible, or less growth risk so I am not going to dig deeper into LW, but it is a good example of what to look for. At the spin-off date, the stock was at $30, with current earnings at $3.21, the forward PE ratio was below 10, implying a double-digit return. A company that might do the same is Ingredion (NYSE: INGR), let’s see.

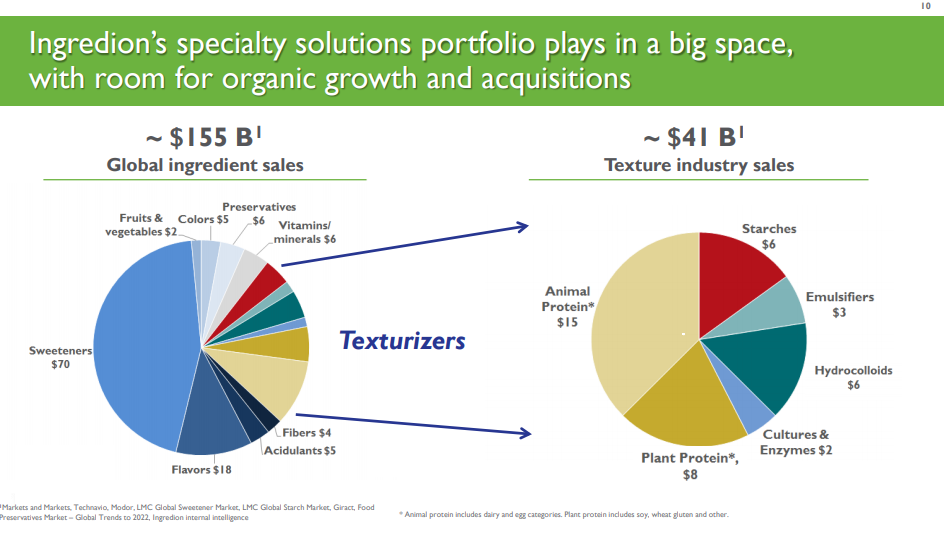

Ingredion Business Overview

INGR is an ingredients company. They produce starch and sweeteners that are commoditized products which make 70% of revenue but less than 50% of profits and specialty ingredients that include flavours, colours and other stuff that goes into processed foods to make it look better and taste better. The specialty section has higher margins as it often includes own formulas. It makes 31% of revenues, up from 20% in 2010 and more than 50% of the profits.

Source: Ingredion

Although we all know of the unhealhiness of processed foods, the trends are clear, people want better, faster and more convenient food. This leads to more and more demand for processed foods, artificial flavours, starch filled foods with sweetener that the market for INGR is there and is growing. I personally think the whole sector, that actually caters to the American diet, is worse than tobacco for people’s health so I don’t think I’ll invest in this, but if you need money for a heart bypass in the future due to your bad diet habits, you might as well make money on INGR.

I’ll just show one example of what is going on in the environment and then I’ll go back to business and investment analysis. So, a company wanted to reduce costs with its spreadable cheese so they replaced the milk fat, i.e. cheese with starch. So, people will think they eat something related to cheese while in fact it will be starch.

Source: Ingredion

Unfortunately, given how prepared and processed food aisles are just growing and growing, the market for INGR will probably grow and grow, especially in emerging markets. As economic power grows, cooking is something mostly watched on TV and seldomly done in the kitchen.

INGR’s potential business growth

The company expects to grow sales mostly through their specialty segment. The other part of the business, currently making 71% of sales is commoditized, sweeteners for example, that has lower margins. Therefore, the focus is on specialty ingredients that lead to higher margins.

Source: Ingredion

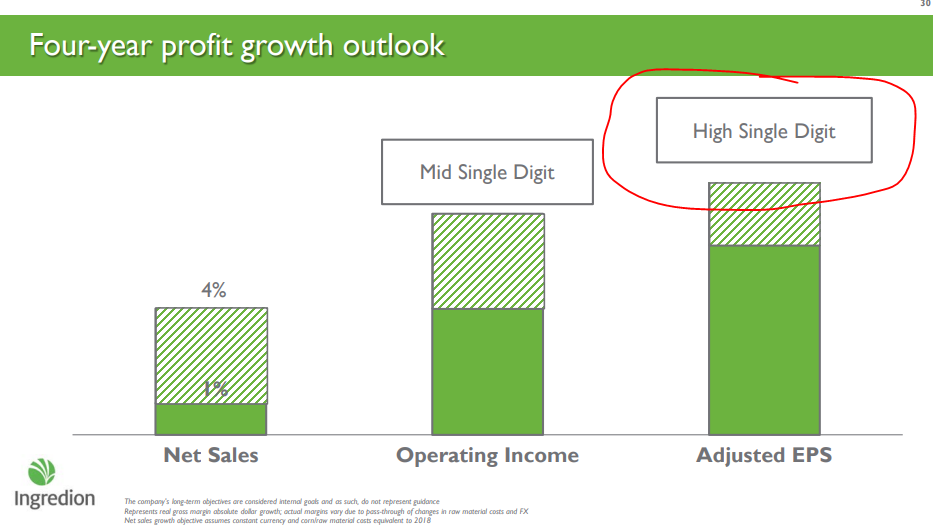

Even though the growth in sales is expected to be small, margins and earnings should expand by high single digits per year.

Source: Ingredion

High single digit earnings expansion over 4 years, on a PE ratio of 13 could be very significant. Their net debt to EBITDA of 1.7, compared to LW’s 4, allows for more room for growth through acquisitions, that are often a good thing in a growing market.

Source: Ingredion

If they reach their target return on capital employed of 10%, investor should expect similar returns. Plus, there is always the possibility that somebody bigger buys them. As we have mentioned in the food sector analysis, mergers and acquisitions are common in the sector.

Source: Ingredion

Current situation with Ingredion

Things haven’t been really that great with INGR lately. The stock is down more than 30% over the last year. The reason for the decline is weakness in North America on lower sweetener prices and a lower than expected guidance, also because of lower commodity prices.

Source: CNN Money

However, the specialty ingredients part continues to grow and the company has been delivering on the ROIC above 10% for the last years, so we can expect it to continue to do so and even improve margins.

On the shorter-term noise, there are issues in Mexico related to retaliation for US corn sweeteners, the situation in Argentina is unclear, margins are expected to decline in some segments but those look like normal business issues.

If they could do an acquisition like the National Starch one, they did in 2010, where their earnings quickly jumped from $3 to $5 per share, that would be great but perhaps current market circumstances prevent them from doing that as even Buffett says valuations are sky high for acquisitions. Since the 2019 acquisitions they have kept debt levels steady between $1.6 and $2 billion.

Investment outlook

Estimated EPS for 2019 is between $6.8 and $7.5 so if I take $7, that is still just a PE ratio of 13 for a company that expects to grow earnings by 8% over the next few years. If they deliver on their promises, we could see earnings per share of around $10 in 2022, and depending on the valuation and future expectations, a price between $120 and $170. If I take an average target price of $150 in 2022, 4 years from now, that leads to a 13% yearly return plus a 2.7% dividend and some share repurchases. In 2018 they have repurchased $607 million of stocks which leads to a 10% buyback yield, not bad.

Cash from operations in 2018 was $703 million, that gives a cash flow yield of 11% where capital expenditures of $349 million are focused on production expansions across the globe.

Food, and especially INGR’s starches and specialty ingredients shouldn’t be much affected by a recession, so we can call it a defensive stock. If their specialty segment manages to take over, turn this into a growth stock and not a stagnating stock due to commoditized products, things might get interesting again as temporary price pressures weaken.

If you want a food stock to follow, this might be it. INGR looks like a stable defensive business with strong cash flows, a good management and a focus on rewarding shareholders.

I am personally not that happy with the healthy side of what they do as I don’t consider sweeteners and starch much of a meal, but you see how it fits your portfolio.