Kroger Stock Is Offering Good Dividend & Great Buybacks

Kroger stock analysis

Kroger’s historical stock price chart shows the company is a compounder, but also that Kroger’s stock price (NYSE:KR) is often volatile which is something that creates investing opportunities.

Kroger doesn’t need much introduction as it is the second grocer by sales in the US.

Here is the video overview discussing Kroger, Sprouts Farmers Market and Ahold for those who prefer watching. More details in article below.

Kroger stock analysis – investment overview

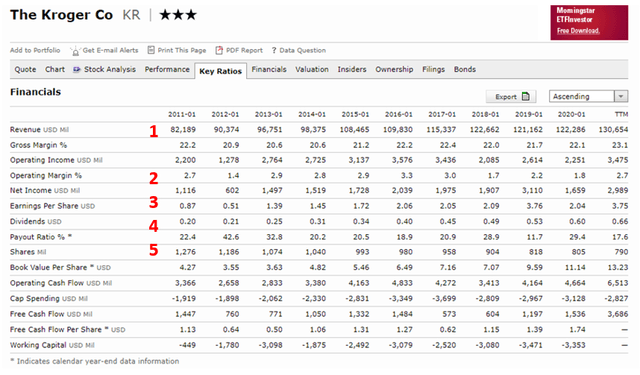

Revenues (1) have been flat over the last years if we exclude the recent COVID boom. Margins (2) and net income have been volatile but what the company did well is buybacks that lowered the number of shares outstanding from 1.27 billion to the current 790 million (5), consequently pushed earnings per share higher (3) and dividends (4) too.

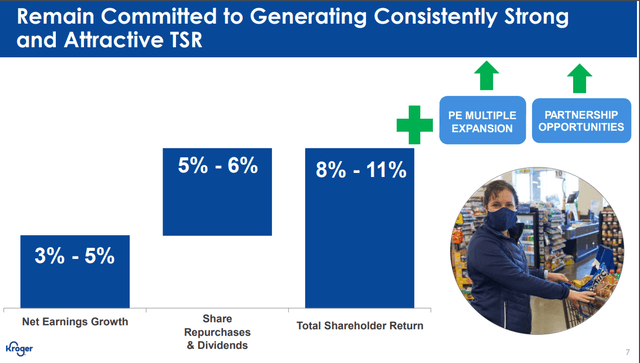

Kroger’s plan is to keep doing buybacks and dividends alongside trying to grow earnings naturally, hopefully reaching low single digits growth.

By being the second largest grocer Kroger is leveraging on its economies of scale and therefore taking advantage, as much as possible, from private labels, customer data collection, rewards, marketing, logistics, partnerships (Ocado and Walgreens) to increase its margins and lower costs.

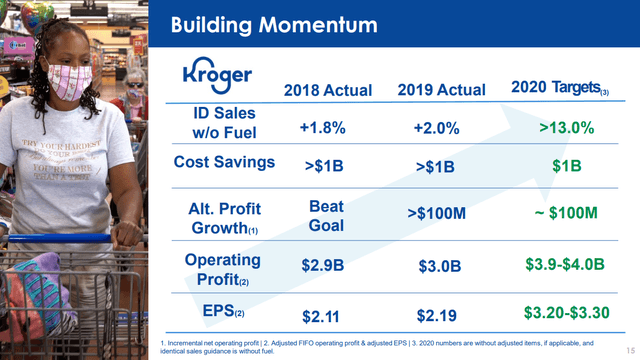

The goal is to create costs savings of $1 billion.

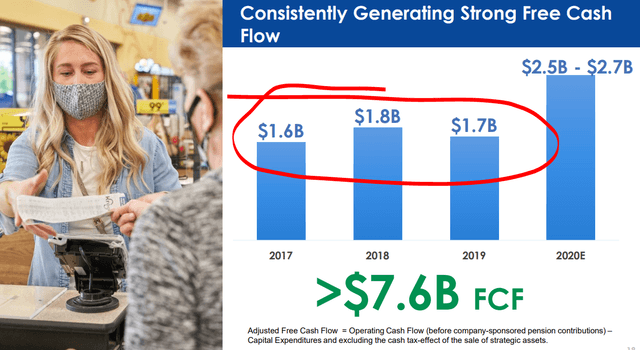

Free cash flows have been improved thanks to COVID boosted demand but even prior to COVID, free cash flows were strong. Using the 2019 $1.7 billion the free cash flow yield is at 7% given the current market capitalization of $24 billion.

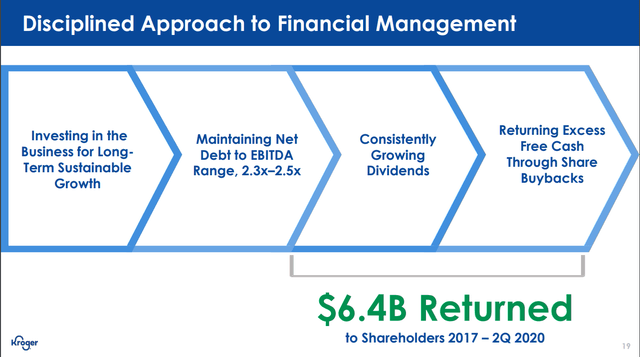

All the free cash flows are returned to shareholders through either dividends or buybacks so there is a strong focus on rewarding shareholders which is not that common these days.

Kroger’s current business situation – comments on last conference call

One of the best ways to understand the situation a business is in or a stock is to listen to the last conference call. The management tells their story but the analysts’ questions always offer key insights exposing the main issues and worries. My comments on the last conference are the following:

Managements’ introduction:

- Digital is profitable and growing, private label is growing fast too – not telling us how profitable.

- Ocado partnership, building fulfillment centers,

- Pension liabilities are an issue – $1 billion charge coming or $0.98 per share, healthcare costs are also a factor to watch.

- Quote: “During the quarter, Kroger repurchased $304 million of shares under its $1 billion Board authorization announced on September 11, 2020. Year-to-date, Kroger has now repurchased $989 million of shares. In June, Kroger increased the dividend by 13%, marking the 14th consecutive year of dividend increases.” Really strong focus on rewarding shareholders.

Questions topics:

- E-commerce reflection in P&L? Answer: Management is excited about it and positive for future growth – doesn’t share any specifics,

- Gross margin COVID benefits of 2020 declining in 2021? Answer: Some headwinds surely but management is working on underlying fundamental improvements constantly,

- Online pharmacy industry development? Kroger’s answer is multichannel and combining healthy foods with pharmacy requirements (smart I must say), plus they say “it appears that about half of healthcare costs are driven by the way people eat”,

- Inflation in supply chain, from corn to freight? Management seeing 2% inflation running at the moment where they aren’t impacted and can transfer prices to customers,

- From whom are you taking market share? Smaller players, big? Answer: just seeing the customer spend more at Kroger’s, very broad-based market share comment.

Kroger stock valuation

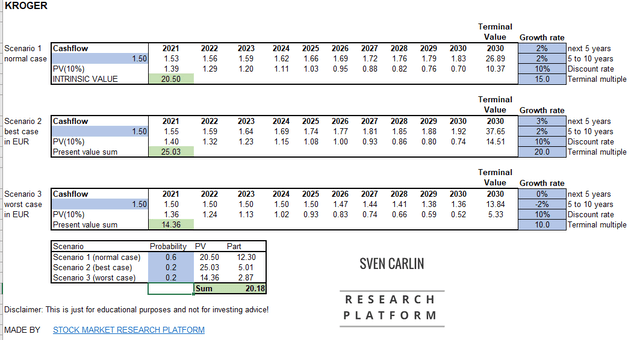

I have made a valuation using a 2% growth rate for Kroger stock over the next 10 years and using the free cash flows as basis. Their plan is to use the money to do buybacks so I haven’t included the buyback induced EPS growth into the model because I have included the cash flows are rewards for shareholders. Buyback returns will depend on the stock price at which Kroger does its buybacks so it is something difficult to model.

Kroger stock valuation – Source: Sven Carlin Research Platform (downloadable)

At the current market cap of $24 billion, Kroger is still likely to deliver a high single digit yearly investment return over time which is really good for a stock in such a safe business environment and working hard on strengthening its foothold.

As for the stock, here goes the investment thesis.

Kroger stock investment thesis

Kroger is a huge business and investment returns will depend on the underlying fundamentals alongside the nuances surrounding the business; from the effects of the Ocado and Walgreens partnerships to the impacts of the pension liabilities costs or union discussions and the general state of the economy.

I am sure there will be periods of bad news and others with good news that will have big impacts on the stock which could make it a very interesting stock to watch around those expectation sensitivities and buy when the sentiment is bad but the fundamentals remain good because I don’t think the business is going to dissapear, we have to eat after all.

One of my first YouTube videos was on Kroger stock where I discussed how the market is irrational when assessing Kroger because it is too focused on short-term issues and not on the long-term investing fundamentals – such situations make a great investing opportunity and make it worth to at least follow and put KR stock on your watch list.

I made the video after the June 2017 stock drop while Buffett bought a billion of Kroger when the stock dropped again in 2019.

I think that by following Kroger, one could get to really good returns by simply following the natural cycles in the grocery sector. We have to eat so the underlying fundamentals are stable, but we have to compare the real value to the market’s sentiment.

The following excerpt from my stock watch list shows how Kroger is cheaper than Ahold Delhaize but a bit more expensive than Sprouts Farmers Market. I will follow it over time and consider adding to my portfolio if we have situations like 2017 or 2019, but this doesn’t mean it is not a good stock to just own now, enjoy dividends and the buybacks. If there is a valuation expansion and KR gets to a similar to market valuation, you get a 100% return.

The reason I don’t have any positions, to explain the disclaimer below, is that for now I have things that might be better, that is all.

If you like my approach to investing and valuing companies, please consider subscribing or check my Stock Market Research Platform.