Index Fund Investing Explained with a 150 year Return Analysis of the S&P 500

Index fund investing

I recently received an email from Peter asking about investing in index funds. He likes the idea of constantly adding money to his investment account in order to earn an average yearly return of 10% – 10% is all he wants. He wants to invest in Vanguard funds and not to bother with stocks, just low commission investing.

In this article I wish to discuss investing in index funds, discuss the 10% yearly return that Peter wants, how to get it from index fund investing and whether index fund investing is the right vehicle for your or not.

We’ll discuss a bit of history where I’ll analyse 10, 20 and 30 year S&P 500 returns since 1871 using professor Shiller’s data to see what to expect from index fund investing over the next decades and then share the only index fund investing strategy has been shown to always work. You will see how it is all about you, not about index funds. You need to be a long-term investor, patient, disciplined and not greedy – that’s all you need for a successful index fund investing career.

If you prefer watching, here is the video, article continues below.

10% annual returns from investing in index funds – current outlook

There is this infatuation with index fund investing and given the wonderful performance over the last decade, even 4 decades, it is logical.

The S&P 500 index fund is up more than three-fold over the last 10 years for an annualized performance of just below 12%.

Add the dividend yield that has been approximately 2% per year during the period, your annualized return would be close to 14% per year.

If we take a 40 year perspective, the situation is really amazing. The S&P 500 Index is up 29 times for an annualized return of 8.04%. Add the average dividend yield of around 3% and you get to a remarkable return of 11%.

If over the past 10 and 40 years, the S&P 500 index has returned 14% and 11% respectively, why would you expect anything to be different in the future, why would you look for anything else, and Peter’s wish of just 10% per year should be a rational one, right?

Well, let’s make an historical analysis of what investing in index funds can bring over the next decade, or even 3 decades. You will see at the end, it is not about index funds, it is not about bull markets or stock market crashes, it is all about YOU and your strategy.

Investing in index funds – what to expect

Investing in index funds is based on the theory that markets are efficient, that there is no point in looking at individual stocks where you just invest a little bit in each stock out there through a low cost fund, and you’ll do great over time.

If you invest in the S&P 500, you invest in the 500 largest companies traded in the United States that comprise 80% of the total market. The indexes are weighted by market capitalization, so the largest companies by value, have the largest weight as the market considers those are the most valuable.

There is absolutely nothing wrong when it comes to investing in Apple, Microsoft, Amazon, Facebook, Berkshire or other household names on the above list. The only important thing is that you keep your expectations in line with what the above businesses at their current valuations can offer over the long term.

Index fund future investment returns – a historical analysis

The S&P 500 went from 100 points in 1982 to the current level of above 3,000 points. What do you think is the probability for the index to repeat such a feat?

Index values did go up 30 times since 1982, but earnings didn’t increase at the same rate. The current S&P 500 earnings when measured in points are 133.

When we divide the current S&P 500 index level of 3,200 points with its earnings expressed in the same points(133), we get a price to earnings ratio of 24 or an earnings yield of 4.16%.

In 1982, since when the remarkable S&P 500 returns have been made, the S&P 500 earnings yield was 13%. Consequently, returns since then were in the double digits.

If we listen to the eternal wisdom of Charlie Munger, investment returns will be closely correlated to the earnings of the underlying businesses.

So, if the businesses in an index fund earn a 4% yield, earnings grow approximately 2% per year, the expected long-term returns from investing in index funds now should be around 6%. 6% is a wonderful return for most investors and you can even increase those yearly returns if you have the right strategy that we’ll discuss in a moment.

It is important to understand that the above approximate 6% yearly return will be delivered over the very long-term, we are talking decades here. You can never know how will your investing returns be over the next year, five or ten. What is important, is that you have a good strategy in place so that whatever happens, you do well.

Index fund historical distribution of returns

If I take the average 10, 20 and 30 year returns for the S&P 500 since 1871, the likely outlook is the following for 10 year nominal returns (excluding dividends) (Data from Shiller database):

- 20% chance for a yearly return between -6% and 0.01% (worst 20% of 10-year returns)

- 20% chance for a yearly return between 0.02% and 2.75%

- 20% chance for a yearly return between 2.75% and 5.15%

- 20% chance for a yearly return between 5.55% and 9.77%

- 20% chance for a yearly return between 9.81% and 15.91% (best 20% of 10-year returns in S&P 500 history)

For 20-year returns, we have the following distribution:

- 20% chance for a yearly return between -2.38% and 1.28% (worst 20% of 20-year returns)

- 20% chance for a yearly return between 1.28% and 2.96%

- 20% chance for a yearly return between 3.09% and 4.97%

- 20% chance for a yearly return between 5.18% and 7.75%

- 20% chance for a yearly return between 7.84% and 13.62% (best 20% of 20-year returns in S&P 500 history)

For 30-year returns, we have the following distribution:

- 20% chance for a yearly return between -0.59% and 1.67% (worst 20% of 30-year returns)

- 20% chance for a yearly return between 1.69% and 3.36%

- 20% chance for a yearly return between 3.59% and 6.05%

- 20% chance for a yearly return between 6.07% and 7.63%

- 20% chance for a yearly return between 7.65% and 9.65%

Did you notice how the returns smoothen as we use a longer period for analysis? Well, now you know what to expect from investing in index funds over the long-term.

Source: Author’s calculations

The thing is that over the long-term, investment returns tend to correlate with the underlying business returns. The average yearly 30-year return was 4.71% with a maximum yearly return over 30 years of 9.65% and a minimum of -0.59%.

Adding the average historical dividend of 4.33% to the average 30-year return from stocks of 4.71%, you get to an average long-term investing return of 9% which is what index funds have delivered over time. This is also correlated to the average earnings yield of 6.75% alongside economic growth and inflation.

But, don’t forget that index funds as investable vehicles didn’t really exist before the 1970s so we are using only hypothetical data.

Given that the current earnings yield is 4.16%, if you get 6% on average over the next 30 years, that should be great, right?

Well, not to be the devil’s advocate, but the above doesn’t discuss real returns, only nominal returns. As we don’t know what will be the inflation rate over the next 30 years, I am not going to analyse the impact of inflation on potential real and nominal returns now as the focus is on other things, but I’ll do it in the future so please subscribe.

Index fund returns and valuations – surprise, surprise

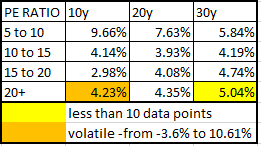

When I plot valuations to the above distribution of returns, I find an interesting surprise. I have analysed the yearly 10, 20 and 30 year S&P 500 returns in relation to the price to earnings ratio and put those in the following distribution: PE below 10, between 10 and 15, between 15 and 20 and above 20.

The results of my analysis explain what long-term investing is all about. If you invest for the long-term, the current valuation doesn’t even matter that much, but if you even think about short-term investing (10-year horizon), you should be wary of valuations that can limit your risk but can’t exclude a catastrophic situation.

Average long term investing returns over 30 years are all between 4 and 6% while the shorter the analysed period is, the higher are the returns in the years starting with a lower valuation.

Note: a percentage point difference of just 1 or 100 basis points on a yearly basis makes a big difference over decades. So, it is not a thing to overlook, but we are going to focus on other things here, namely what to expect long-term from investing in index funds now.

History is pretty straightforward – your investment returns will be closely corelated to the natural business earnings and their inherent natural growth ,where the longer your investment horizon, the smaller is the range of possible outcomes.

Therefore, the most important thing when it comes to investing in index funds, isn’t really index funds, but you. Let’s talk about strategy.

Index funds investing strategy – 3 key factors to follow

If you have a long-term investing horizon, one counted in decades, you have nothing to fear if you are investing in index funds. You don’t need to put any effort in it, actually what you need is to forget about the investment, put it on automatic and your returns will be between 4% and 8% on a yearly basis including dividends. Nothing wrong with that.

The problems start when an investor’s expectations are not aligned with what index funds are here to offer.

1) Short term goals – long-term investing mindset

Given the historical performance and media discussions, I have the feeling many investors think index funds can only go up. Unfortunately, that is not true and there have been times in history when an investor had to wait a few decades to just breakeven in nominal terms. A look at the DOW JONES index chart from 1896 shows how there were 4 periods when investors had to wait more than a decade to achieve positive returns. The sum of years when the S&P 500 was below a previous levels since 1871 is a staggering 76 years over a 130-year period. So, you have to expect that 50% of the time, investing in index funds will not deliver any kind of positive return.

Now you might be thinking, Sven you just described how index funds will deliver between 4 and 8% per year over time and now you say that more than 50% of the investment time I should not even expect positive returns? Where is the fun in that?

Well, the fun is exactly there. Apart from investing for the long-term and allowing the businesses you own to compound their returns, the second part of the best index fund investing strategy is to invest constantly over time. Most of us are net contributors to our portfolio and therefore we should rejoice lower stock prices rather than higher. Let me explain.

2) A stock market crash is amazing news – discipline and patience

The biggest fear I hear people talking about is a stock market crash similar to the last two crashes when the S&P 500 crashed 50% in consequence of the dot-com bubble bursting and the great recession.

What I don’t understand is why the fear of something like the above happening, we should all hope it happens.

Let’s imagine we have a $100k portfolio invested and we add $500 per month or $6,000 per year into stocks. I have created 3 scenarios; the first where stocks simply continue to go up 6% per year, and two scenarios where stocks fall 50% and then continue to go up 6% as in the first scenario while in the third scenario, stocks first fall 50% and then grow at 15% per year to reach the same level reached by the constant 6% growth scenario. Given that sooner or later stocks always pass their previous highs, it is logical to expect something similar to happen in reality.

The above table is a bit complex but the message of the story is that lower stock prices allow you to accumulate businesses much cheaper and that even if stocks crash 50% tomorrow, once stocks reach their expected level thanks to natural growth, you will be better off thanks to the crash.

So, the key is to be disciplined to constantly add to your investment portfolio on a monthly basis, especially if stocks crash. We have seen how long-term investing returns are skewed towards the positive and in the high single digits no matter when you start investing or the valuations at the time.

So, if you keep investing month after month, no matter what is going on, you’ll do well. The only thing you have to be is to be the opposite of greedy.

3) Don’t be greedy – be the opposite and only be greedy when others are fearful

The third step towards a strong index fund investing strategy is not to fall pray to whatever is going on. I’ve heard too many stories about investors that sold panicky in 2002 or 2009 because they feared loosing their wealth and perhaps even worse, investors that reached all their dreams in 2000 or 2007, that then didn’t sell because if the market went up just a bit more they could add 10 feet to their boat or another spare room to their holiday home.

The thing is that given the volatility of the stock market, you will be given the opportunity to cash out at favourable terms at some point in time. Will it be when you have 55, 63 or 67, I don’t know, but if you patiently wait, the market will give you the opportunity to cash out and reach your financial goals. When that happens, don’t bee greedy and risk what you have and need for something that you don’t have but also don’t need.

Index fund investing is about you

So, it is about knowing what you need, when you need it and then simply use the above ‘how the market works’ forces in your favour over your investment life-cycle.

I personally don’t invest in index funds because I think I can do better by investing in individual businesses globally. However, my strategy involves meticulous research, analysing and following businesses which is a full-time job and I do research businesses for a living.

The funny thing is that you don’t have to be exclusive, you can invest in both index funds and in individual businesses that you understand. Just compare what is the risk reward of the investment, how it fits your investment goals and then make the decision. As would Buffett say: “you only need a few good investments in your lifetime.”

This article is part of my Investing in Asset Classes section within my Free Stock Market Investing course so if you wish to learn more about investing, sign up.