Fixed versus variable mortgage interest rate – what is the difference in 2019

I’ve made a few videos discussing real estate investing as brick is a key component of one’s financial life. If you look at most people, a large chuck of their wealth is accumulated over the years by investing in real estate, be it their own home or other properties. So, taking a mortgage and buying a house seems the smart thing to do. But what kind of mortgage to take, a fixed or variable interest rate? That is what we are going to discuss today.

Here is the video for those who prefer watching or listening to reading, article continues below.

How to choose between a variable (adjustable) or fixed interest rate mortgage

Think of this first – you are making a 30 year long decision – don’t make it on current news, make it on what might happen over the next 30 years.

Variable and fixed interest rates – definition

A variable interest rate or adjustable interest rate changes in relation to how market interest rates change. Your mortgage will probably have an interest rate that is a bit higher than the interest rates set by the central bank.

Source: FRED – historical 30 – year fixed mortgage (red) rate and interest rate (blue)

Over the past decades, mortgage interest rates have always been a few percentage points above the FED’s rates. What is important from the above picture is that 30-year mortgage rates have also been above 13% for a long period of more than 4 years in the 1980s, something to keep in mind before taking a mortgage.

Fixed interest rate mortgage

If you don’t like uncertainty when it comes to your monthly payments, you will take a mortgage with a fixed interest rate. That should not change over the whole course of your mortgage but be sure to read the fine print (ESSENTIAL TO DO THAT) so that if interest rates go back to 1980s levels, you bank can’t trick you.

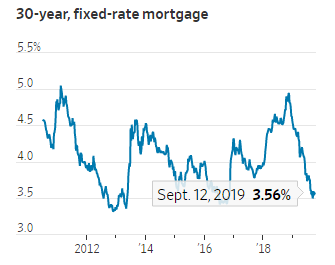

Current US 30-year, fixed-rate mortgage:

The negative side of the fixed-rate mortgage is that rates, and thus the cost of your monthly payment is usually higher than with variable rates. A bank has to insure against changes in interest rates for the next 30-years and therefore requires a higher rate.

Source: FRED – adjustable rate mortgage (blue) versus 30-year fixed (red)

There is not much difference between the adjustable rate and fixed rate mortgage at the moment, but those things usually diverge by a percentage point or more. The difference is cost globally isn’t much these days. On 1 one percentage point difference, it is $50 on an $80k mortgage.

Source: Bankrate – mortgage calculator

Now, which one is better? Let me show you my risk versus reward investing perspective.

Variable or fixed: which is better?

So, for just $50 per month on a $80k loan, assuming you bought a $100k home, you can sleep well because you are sure nothing will change over the next 30 years. Adjustable interest rates in 2007 were above 5%, average adjustable rates were above 6% during the 1990s and often above 10% during the 1980s.

Now, let me put this into perspective. Let’s say you take out a $80k loan, you take an adjustable rate of 3.6% on it. The rate remains fixed over 10 years, but then, due to inflation, rates spike to 10%.

On an $80k loan, after 10 years you pay down only $15,626 of your principal because you have to first pay interest on your loan.

Now, if interest rates spike to 10%, you still have 20 years to return $64,374. The monthly payment at a 10% interest rate would be $732, or 47% higher than the current one. That is the risk for taking an adjustable mortgage, you never know what lies ahead.

So, because of paying $50 per month more, or $600 per year more, that is probably tax deductable in some countries so the difference is even less, people choose for adjustable rates, not even thinking of what might happen over the next 30-years.

In the current environment, where central banks will constantly print money, I think it is crazy not to take a 30-year fixed interest rate mortgage. But, then again, I always seem to be the crazy one. Those that require higher mortgages, like to take adjustable rate mortgages to have lower payments, they are probably buying homes they can’t afford.

ARM risky, should you go for 10 or 20 fixed years?

My thiking is why take a risk on something like a mortgage, any kind of risk? Given that mortgage rates are at historical lows. In the Netherlands, mortgage rates have not been so low for the last 500 years, the smartest thing to do is to fix the rate for 30 years. Given the difference in the monthly costs that is really small, versus the potential costs if interest rates go up, and those will likely go up as central banks print more money, it is much better to take a 30-year mortgage in the current environment.

But then again, people make decisions on whatever assumption. On my stock market research platform, a subscriber asked me about what mortgage to take in the Netherlands.

So, dig deeper into all kind of scenarios before taking a mortgage. Remember, it is a 30-year decision you are making! I am sure you didn’t go for one cup of coffee with your spouse and decided to live your life as she or he said. But, you are going to have a 30 minute chat with the nice mortgage officer, they will explain you what is the best option where they get the highest commission, and you will buy the house of your dreams.