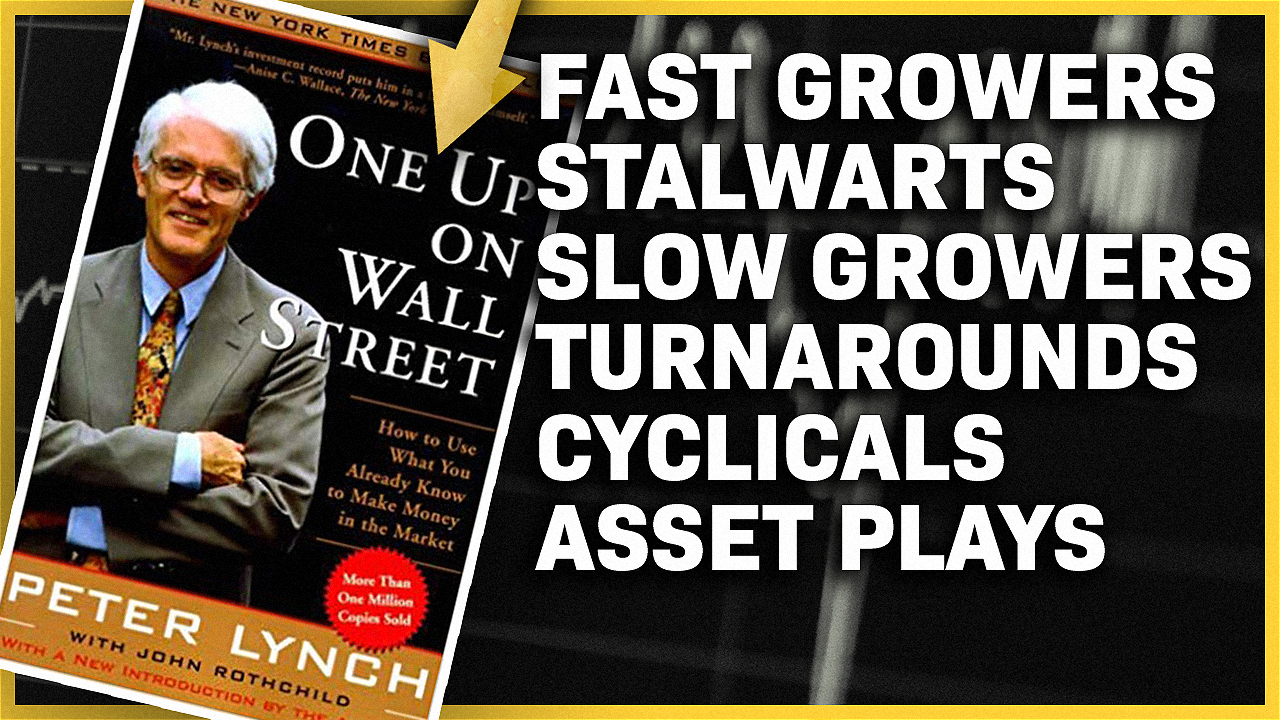

When To Buy Stocks And When To Sell Stocks – The Six Stocks Categories Tool by Peter Lynch

Six Categories of Stocks – When to buy stocks, when to sell stocks! From One Up On Wall Street by Peter Lynch – A MUST OWN INVESTING BOOK

“Investing without research is like playing stud poker and never looking at the cards”

Peter Lynch

Here is the video for those that prefer watching or listening, written article below.

The thing is that looking at the cards when it comes to investing takes a few hours to first research the idea and then one hour per week to keep up with the interesting stories you have found!

Use Occam’s razor (stick to simple explanations and stay away from what you can’t understand), you might miss out on some, but you will be right on most of them as the most likely explanation will be the correct one.

When looking for investing ideas, the best way to approach a potential stock to buy is to categorize it into the following categories. This will give you a clear indication of whether something is a buy, sell, hold or stay away stock.

When to buy stocks – SIX CATEGORIES OF STOCKS:

- SLOW GROWERS

- STALWARTS

- FAST GROWERS

- CYCLICALS

- ASSET PLAYS

- TURNAROUNDS

We are going to explain each category in detail, what to expect from each type of stock and you can then see how does a stock you own or you are looking to buy fit the discussed categories.

Before we start, just a comment on Lynch’s idea that we should look into smaller companies out there.

BIG STOCKS SMALL MOVES – focus on small caps if possible

Big companies perform well in certain markets, but don’t expect miracles.

KO stock is up 36% since 1998. That is not much over 22 years! Yes, it globalized, it grew earnings and dividends, but due to its high global presence already, it had more to lose than to win.

So, to find really great investments, you might want to look into the stocks that are not that famous, small caps. However, it all depends on the situation and that is something we are going to learn by analyzing the 6 categories of stocks Peter Lynch presents.

SLOW GROWERS – STOCKS TO AVOID

Keep in mind that fast growers turn into slow growers at some point in time. A recent example is Apple. Apple and IBM are discussed in the book as fast growers. IBM became a slow grower much earlier than Apple, but sooner or later all stocks hit the upper limit.

Slow grower expectations:

- Flat chart (flat earnings – Stock can move on valuation)

- Generous and regular dividend (Apple’s dividend and buyback payout is large)

- CHECK THE DIVIDEND SAFETY – low payout gives a cushion, high payout makes it risky (both the dividend and the stock)

NOT A BUY FOR PETER LYNCH because earnings are what enriches a company. Apple in 2009 yes, now, not anymore. Actually, this tells us when to sell a fast grower. You sell when the dividends and buybacks attract a different kind of investor, one that loves the apparent safety.

THE STALWARTS – KEEP SOME IN YOUR PORTFOLIO FOR RECESSION PROTECTION

Stalwarts grow a bit faster than slow growers, but not that fast. 10 to 12 percent earnings growth is what defines them for Lynch. Given the current economic environment and low inflation, we should take 5 to 10% into consideration.

With such companies, to make profit, you need to time your purchase well. If a stalwart goes up 50% in a year or two, you might want to think about selling.

For example, BMY grew revenues at about 10% since 2014. Those that bought it in 2012, had a good return, but don’t expect miracles. To note, from 2005 to 2011, over the great recession, the stock was flat.

Another issue with such companies is envy. They see other companies grow faster, and then they enter new businesses at a high cost – Lynch calls it diworseification. Be careful when a big company announces a merger with something not really within their circle of competence.

Stalwarts expectations:

- Make 30 to 50 percent and sell

- Always keep some in your portfolio because of recession protection

- However, check how it did in previous recessions and see how much protection it gives

- Unlikely to go out of business

- Price to earnings ratio will tell you the value

- Beware of diworseification

THE FAST GROWERS – THE STOCK THAT MAKES AN INVESTING CAREER

Lynch’s favorite investments that grow faster than 20% per year. This is the land of the 10- to 40-baggers, even 200-baggers. One fast grower can make a career.

It doesn’t have to belong to a fast growing industry, all it has to do is have the room to expand in a slow industry.

Starbucks (SBUX) was a fast grower in the 1990s and 2000s that has now turned into a stalwart.

Those that invested in the 1990s ended up with a 20-bagger, those that invested later did still good, but not as good.

Fast growers expectations:

- If growth slows down the market doesn’t like it

- If finances become an issue Chapter 11 (bankruptcy is probable)

- Look for good balance sheets making substantial profits

- Figure out when they’ll stop growing and how much to pay for growth.

- At some point they will stop growing and turn into something else – that is the only guarantee. Check how much more room for growth there is.

- 20 to 25 percent is the best growth – 50 percent is for hot industries and you know what that means (hot industries attract many competitors)

- Proven, profitable expansion in more than one city or country

- PE ratio should be below the growth rate

- Check whether growth is expanding or slowing down.

- Look for those that few institutions own and that few have heard of.

THE CYCLICALS – IT IS EASIER TO PREDICT AN UPTURN THAN A DOWNTURN

Cyclicals follow the economy. Automotive, airlines, tyre companies, steel, chemical, travel etc. are all cyclical companies. Ford’s stock is a perfect example, down with every recession or slowdown, and currently down again on the expectation that there will be a recession.

Cyclicals expectations:

- Flourish when the economy turns good again

- Suffer when there is no economic growth

- 50% drops are normal if you buy at the wrong part of the cycle

- You can wait for years before seeing another upswing (Ford down since 2013)

- Large and well-known companies that make the unwary stock picker most easily part with his money

- Timing is everything – watch for inventories and for new market entrants

- Stock usually declines when peak earnings is reached and investors expect next recession (look at Ford)

- Know your cyclical and figure out the cycles – Within the car industry, 3 to 4 bad years are usually followed by 3 to 4 good years.

- The worse the slump, the better the recovery.

- Easier to predict an upturn than a downturn in the industry.

TURNAROUNDS – BUY ONLY WHEN YOU KNOW THE MARKET IS WRONG IN ESTIMATING THE MAGNITUDE OF THE CRISIS

Turnarounds are companies that are close to chapter 11. However, when bankruptcy fears ease, stocks explode as investors start to rerate earnings and potential.

Turnarounds expectations:

- Explode on the upside when things improve

- Go bust when things don’t improve

- Understand whether the issues are as big as perceived or not – if you can’t, say next

- Can the company survive a raid from creditors?

- Ask how will the company turn around?

- Restructuring is not good, even if perceived as such

- However, one-time losses make buying opportunities

- What will be the effect of cutting costs?

THE ASSET PLAYS – BUY WHEN YOU ARE HAPPY OWNING NO MATTER WHAT

An asset play is a company sitting on something valuable that the market is overlooking or the asset hasn’t yet started to print cash. The asset can be cash, real estate, even accounting losses, inventory, the number of users etc.

I remember buying prime Adriatic real estate for 1 EUR per square meter in 2010. It took 4 years of waiting for the value to get recognized, but it was worth it.

Asset plays expectations:

- Know the asset

- Have patience until the value unlocks

- Look at the debt

- Look at hidden assets

- Is the management destroying or creating value?

- Is there an activist investor involved?

THE INVESTMENT STRATEGY – ALWAYS PUT A STOCK INTO THE ABOVE CATEGORIES

- Figure out what kind of stock it is, closely follow and then make decisions.

- Putting into categories helps in defining the first story, next what we have to do is to watch the important parameters impacting the story.

This article and video are part of my FREE Stock Market Investing Course.

If you want to check my research, the stocks I follow where we focus on trying to find the best moment to buy in line with the above, check my Stock Market Research Platform.