Accounting for investors – Misuse of EBITDA explained

An Accounting Warning by Charlie Munger

I am reading Poor Charlie’s Almanack and will discuss the things I find most relevant for investing! Investing is about having the right mindset first – that is why we always emphasize psychological concepts – and only secondly about doing relentless research and also having the skills to do such research. Speaking of skills, without accounting you are doomed when it comes to investing, you are practically gambling. So, let’s discuss a bit of accounting. Here is the video for those that prefer watching, article continues below.

In his book, Charlie Munger mentions 5 things I think are extremely important to understand:

- EBITDA misuse

- Pension fund estimations – overly optimistic

- Aggressive accounting

- Ethics and accounting

- Derivatives

I’ll do my best to explain those concepts in simple terms and use examples.

Misuse of EBITDA

I always argue with CFAs or business school viewers about how EBITDA doesn’t help when it comes to investing. In my work, when I analyze companies, I always look what is there beyond EBITDA.

EBITDA is earnings before interest, taxes, depreciation and amortization:

- Earnings before interest, like debt doesn’t matter.

- Before taxes, like taxes don’t matter – do taxes matter to you?

- Before depreciation and amortization. D&A are a cost that you have had, no matter if not in cash, the company already invested that money in the past.

Munger calls EBITDA as bullshit earnings, let me give you an example.

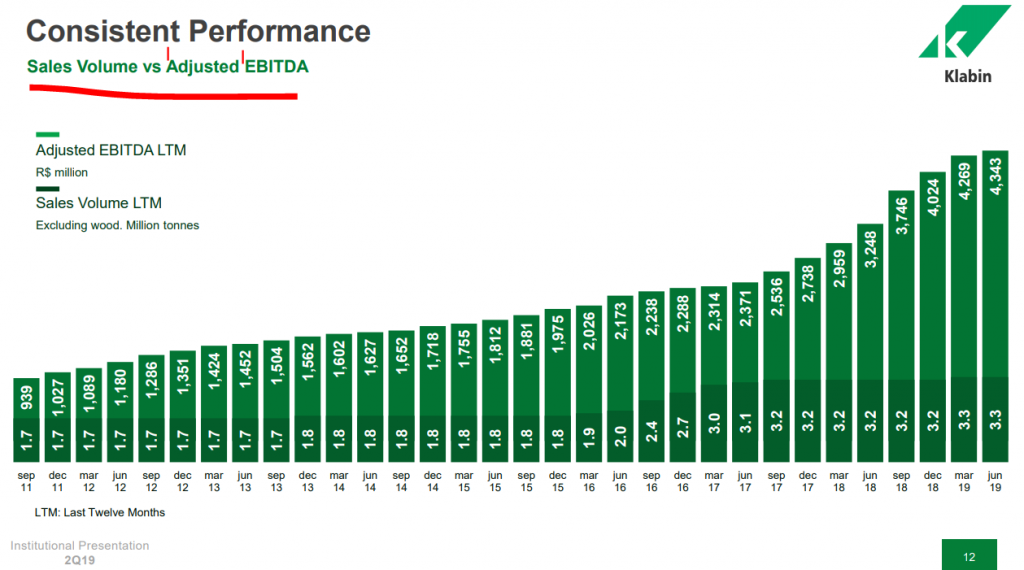

Klabin is a Brazilian paper and pulp company. In their investor presentation they show a beautiful chart of constantly growing EBITDA.

Source: Klabin

EBITDA, adjusted, grew from 939 million Brazilian Reals to 4 billion over 7 years, that is a terrific performance, right?

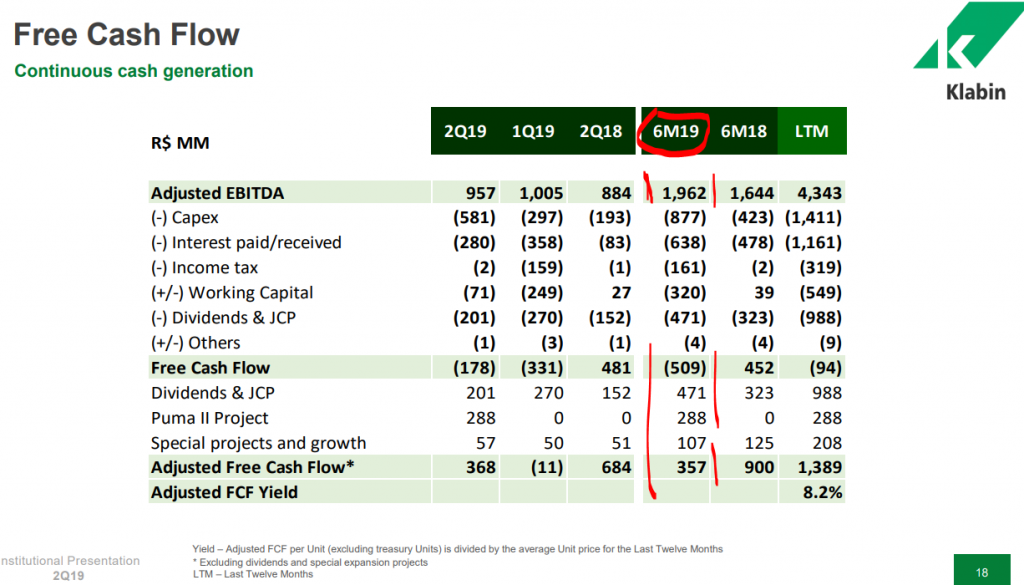

To look beyond EBITDA I look at the cash flow, in the first half of 2019, they have managed to have 500 million of negative cash flow on 2 billion of positive adjusted EBITDA.

Source: Klabin

Ok, when you adjust for the investment in growth and for the dividend, they get to positive cash flows of 357 million. So, on 2 billion in EBITDA, the earnings or cash flows available to shareholders is 357 million. That is just 18% of EBITDA. Which number is a better representation of what is going on with the business and what will your return be?

Why is Wall Street’s focus on this adjusted EBITDA and not on cash flows? Well, that is the number people use to estimate debt levels. Klabin’s debt level looks good, the debt is just 3 times EBITDA. However, if I look at it from a cash flow perspective, it is ‘just’ 10 times adjusted free cash flow, or just xx free cash flow. Well, I can’t even calculate it because the free cash flow is negative.

We have a company that doesn’t add cash, but has 13 billion in debt. It actually takes debt to pay dividends. This doesn’t have to be bad; it is just risky and if market tailwinds change, the company could get in trouble. For example, if the Brazilian real strengthens against the dollar, the company’s margins would decline because their costs are mostly in their domestic currency while the revenue is in dollars and the whole house of cards could collapse.

The Brazilian Real lost 50% of its value against the dollar over the last 9 years, exactly since the above beautiful EBITDA chart has been calculated.

Source: XE

This is on a company specific level, but there is so much more beyond the misuse of EBITDA. The presumption is that to compare business performance you should eliminate taxes and debt or interest payments. That is bonkers, to use Charlie’s words, because no company can borrow to infinity at a fixed interest rate. When shit hits the fan, people see how they were blinded by EBITDA, covenants get breached and companies go quickly bust.

When things turn, in a recession, you see how futile EBITDA actually is.

Pension fund accounting

I recently received a message from my Pension fund in the Netherlands that I contributed into while I was an accounting professor there. The email said it is likely my pension will be lower than expected.

Pension funds use too optimistic measures for their future performance than what is logically possible to achieve. Just look at the investment return assumptions by pension plans, this is included in their calculated obligations in the balance sheets of the firms that have such plans. Those returns are staggering, 7% on average and higher.

Source: NASRA

How are they going to achieve 7% when the yield on the 30-year Treasury is 2.1% and on high yield bonds 6%?

This simply means that there will be a lot of pain in the future because of the misuse of accounting. The overly optimistic assumptions are included into balance sheets when they calculate the present value of future obligations and compare them to the current assets in the pension plan. I have been seeing some changes in such policies lately, but still the above optimistic assumptions are dangerous.

Aggressive accounting

Aggressive accounting is the practice of adjusting the numbers in order to make them look better than what those actually are. For example, British company Carillion went bust in 2018 after it used supply chain finance to cover up for business not going that well.

Source: Euromonitor

Carillion has used supply chain financing where it engaged in financing suppliers for the receivables they had towards Carillion. That was pushed to the limits and once uncovered, the company went bust as then net cash position went from 467 million to minus 292 million because the debt was recognized as real debt, and not some form of receivables versus payables.

I could give you many examples of where companies stretch their finances, leases versus debt is just one example. A long-term lease contract doesn’t go into your long-term debt account on the balance sheet, but the obligation is there. So, that is another way to make your finances look better. As always, look at the cash flows of a company.

Demise of ethics among major accounting firms

An example is KHC, Buffett’s holding, it had to restate 3 years of earnings.

Source: Reuters

So, be careful and keep it in mind as a possibility. Munger says it nicely about accountants, a long time ago, no accountant was rich, they were ethical. Today, accountants are rich, so their incentives are skewed.

There is one equalizer you can watch here, it is one that saved me from losing money a few times, it is cash. That is something hard to hide, whether you have it or not.

Accountants stay silent

Charlie summarizes this by saying the reason why accountants stay silent is: Whose bread I eat, his song I sing”.

On Derivatives, a topic we didn’t go into, Charlie says that comparing accounting for derivatives with sewage is an insult to sewage. BRK sold all of the General Re derivatives at a big loss and I am going to show you how those derivatives end up by showing you DB’s stock chart.

Conclusion – look for those that keep things simple or, play the accounting game but be sure to understand the risks and move fast.