Woodside Stock Analysis – Dividend Value & Capital Gains

This Woodside stock analysis has 4 key investing lessons:

- Value can be found in cyclicals and Woodside surely offers value.

- Sticking to a dividend no matter what is costly, the same holds for buybacks.

- However, dividends are what create long-term returns, so it is a fine balance there.

- On low risk high reward investing (value investing): playing on the inherent volatility of the stock is also value investing, as Would Seth Klarman say in his book Margin of Safety: “Volatility is a value investor’s friend”. Woodside will surely be volatile.

Housekeeping: US dollars unless otherwise stated in the figures and writings.

Woodside stock analysis content:

- Woodside stock price overview

- Woodside business overview

- Woodside stock fundamentals

- Woodside dividend

- Woodside cash flow valuation

- Woodside risk reward investment conclusion

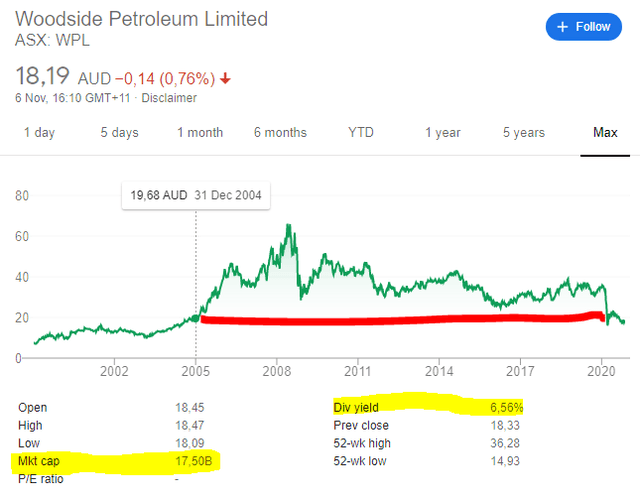

Woodside stock price overview

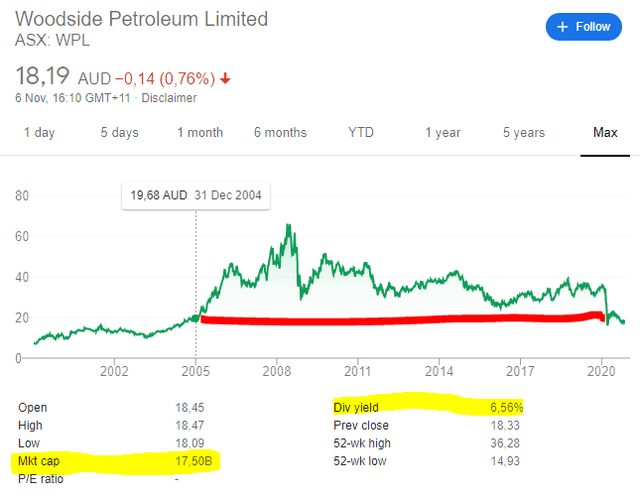

Like it is the case with many other oil and gas stocks, Woodside stock didn’t really reward shareholders over the past 15 years except for dividends. We first had the boom in the late 2000s when some even predicted oil at $200, then a slow and steady decline down to the current situation. Actually Woodside Petroleum stock is where it was in 2004.

As value investors, we have to see whether Woodside stock is cheap now and we can figure that out by estimating future cash flows, because investing is about the value we get in the form of cash flows compared to the price we pay, not about what happened over the last decade.

However, the negative stock market return means that the investments made didn’t create the expected return on capital and that shareholder value was actually destroyed. On the other hand, the oil and gas industry is cyclical and we have to watch it from that perspective too, perhaps a new positive cycle will happen in the 2020s. Production costs are the key to watch there.

Woodside business overview

In short, Woodside is a growing natural gas producer and LNG exporter. When a company has a growth focus, that also means high capital requirements and operating risks, something we have to focus on. Let’s first give an overview of the business.

They have low production costs, but one must look at total costs for production, including investments to see what is the real margin. I will take 2019 margins as a good conservative indication of what could average long-term margins be.

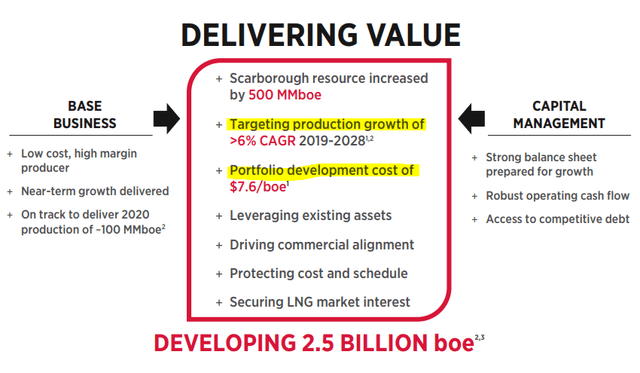

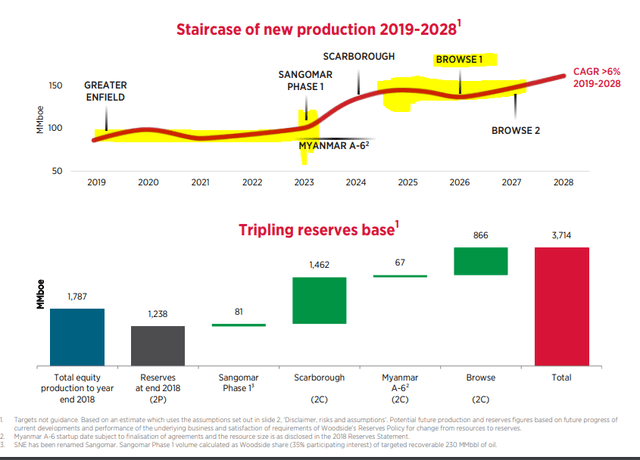

The growth trajectory sees production stability till 2024, then a jump in growth as Sangomar and Scarborough are developed. More growth with Browse 1 and browse 2 beyond 2026.

The returns of the investments above will depend on future natural gas and oil prices, Woodside might be a bit too exuberant there or maybe not?

Woodside investing issues – price estimations

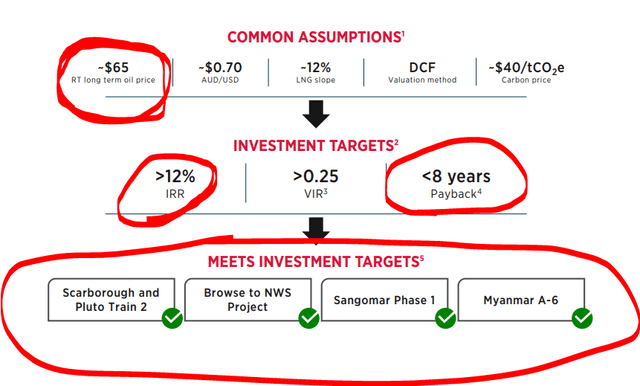

And here is the problem with Woodside, and probably the reason for the low investment returns in the past. Their assumption for oil prices could be too high. I have analysed RDS stock, and their projections for longer term oil prices are at $60, not $65, while Russians make investments decisions expecting oil prices to be at $40. If oil is below the expected $65, investment returns will be below 12% and below the cost of capital, which then creates negative returns for shareholders, no matter the price of the stock.

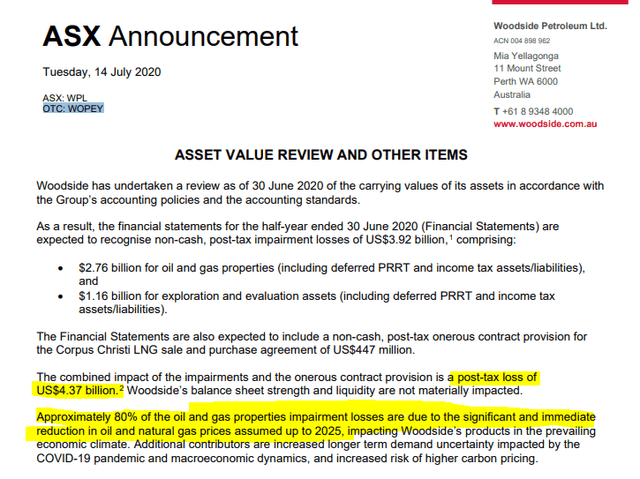

When you miss pricing projections, and we all know forecasting is difficult, especially when it is about the future, you end up with impairments.

This is how impairments look like; a mention here and there, saying it is not a cash cost and the management goes forward like nothing happened. For me this is huge and really explains the risks of investing in companies like Woodside. $4.37 has just been erased like nothing happened, that is 30% of the current market capitalization.

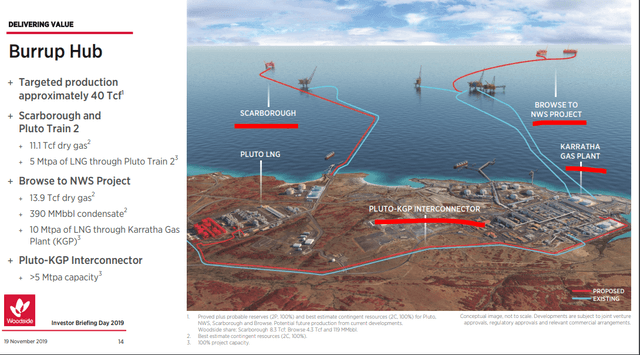

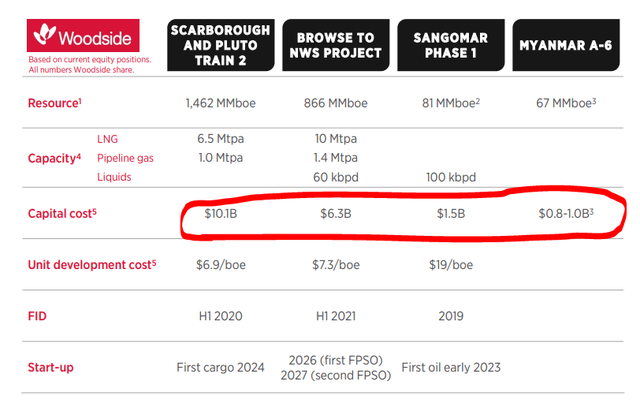

Of course, the future returns on the projects will all depend on natural gas prices and LNG. Here are the visuals on the projects.

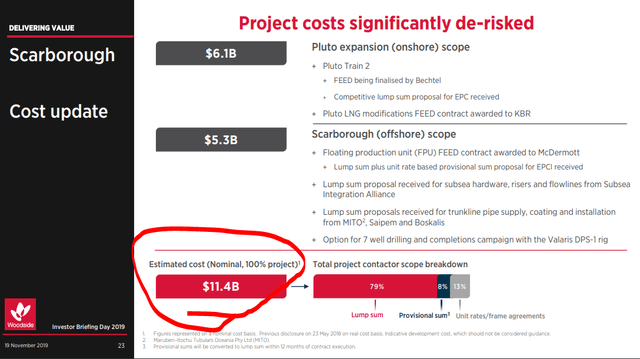

The costs to develop the above projects are significant.

The Sangomar project will cost another 1.5 billion, Browse to NWS $6.3 billion.

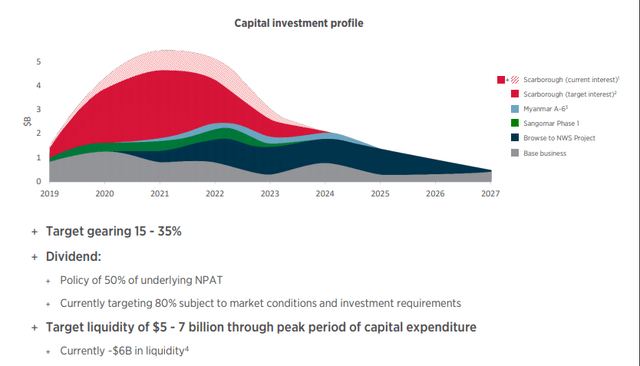

For the next 3 years, capital expenditures are expected to be at $4 billion.

The main question is will the above projects deliver value over the long-term and if they deliver value, for how long will it be like that?

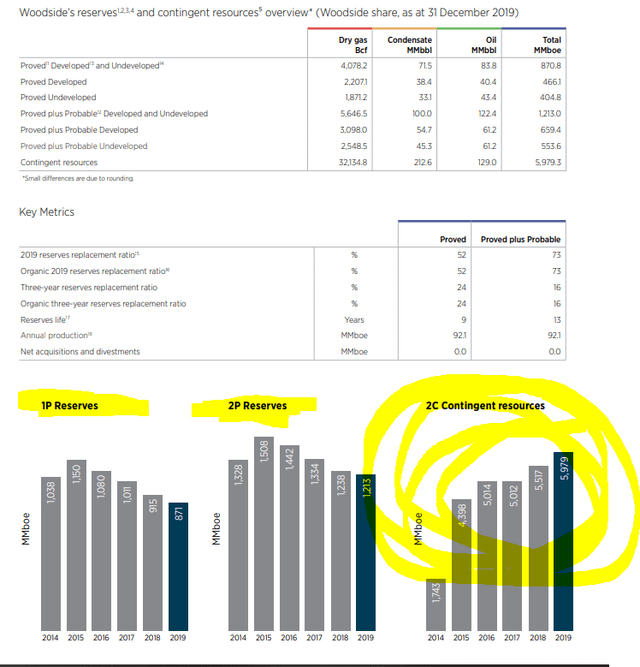

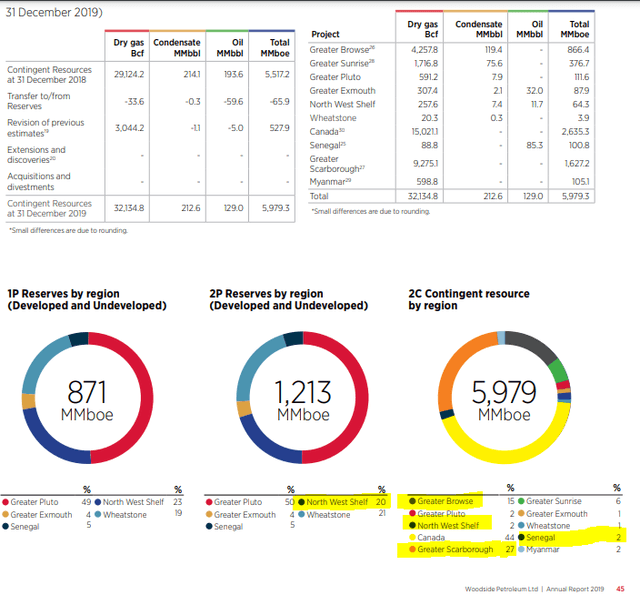

On a reserve basis, Woodside has enough to produce for another 7 years of proved (1P) reserves, 14 years of probable (2P) reserves and 30 years on contingent reserves, that still have to be proved, then developed and the price of natural gas has to be right.

Nevertheless, I am going to use 30 years of production ahead for my calculations because they are likely to invest into the contingent resources and develop them in the coming investment cycle.

Let’s see how the above looks from a financial perspective.

Woodside stock financials

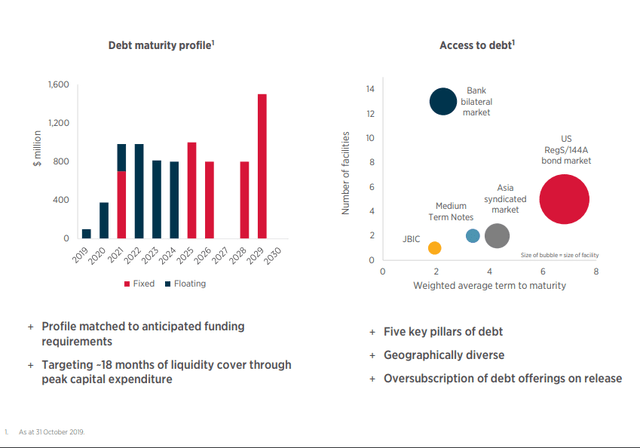

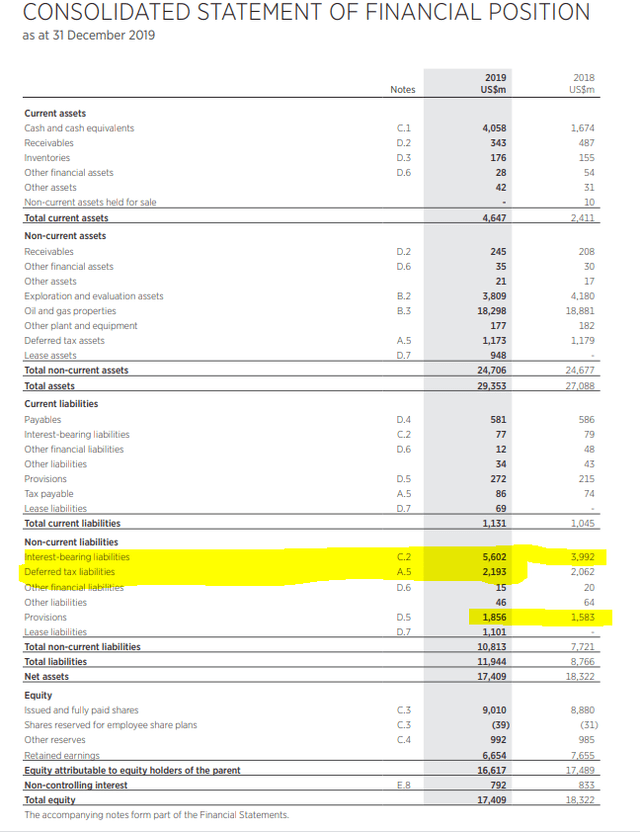

The above investments will require significant capital and the debt is already significant with Woodside, but not high. The issues is that if they don’t reach their estimated returns with the projects, they will not able to repay the debt.

They say they have leading margins, that might be the case in Australia, but natural gas is about global competition, let’s look deeper into financials.

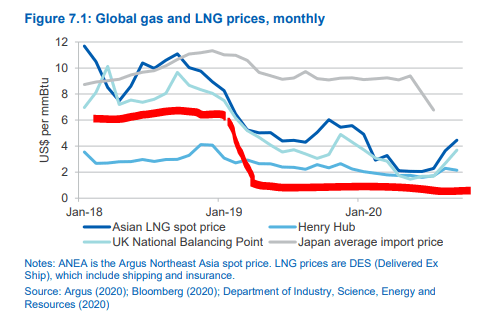

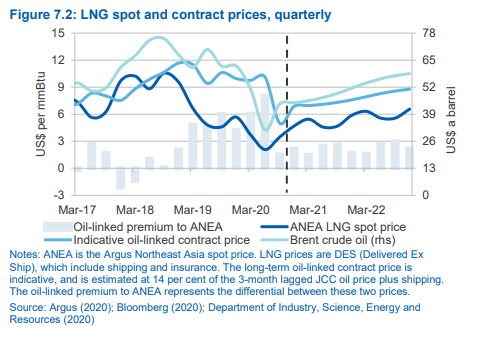

It will all depend on natural gas prices. 2018 was one with high prices but 2019 has seen a big decline and we have to see when will this balance out and where will the average long-term price settle.

Compared to oil prices, the below chart shows what is going on.

Except for a brief period in 2018, approximate LNG prices were never above comparative $65 oil prices, which is the level Woodside uses for their calculations and investment decisions.

Nevertheless, turning natural gas into LNG costs already something around $3per mmbtu, Thus, prices will have to go higher and be higher, at least at $6 mmbtu. I think we can use 2019 financials as very conservative assumptions for the future.

They have impaired $4 billion of assets based on lower for longer price expectations, but let me tell you something, price expectations are almost always wrong and analysts usually take the current price and project the future. I haven’t heard of anyone being capable of knowing what the future brings. If you know someone, please let me know, would make my job easier.

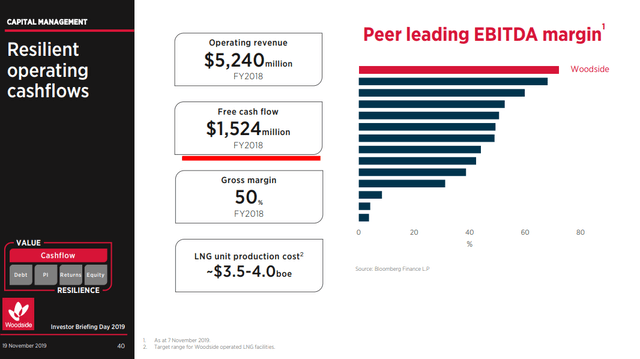

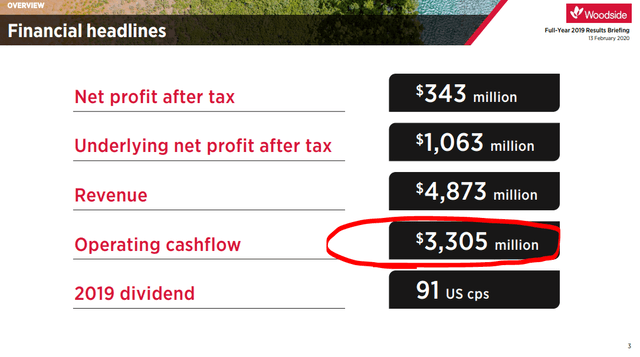

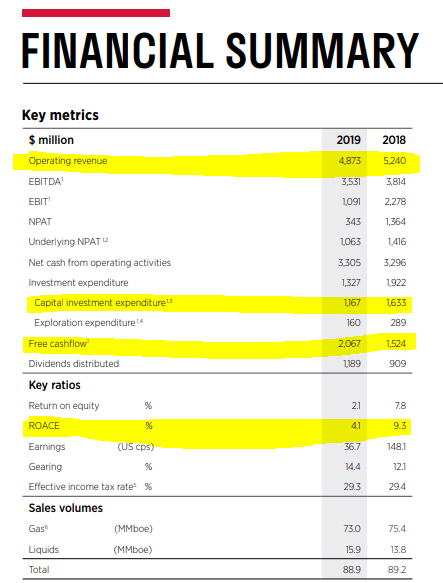

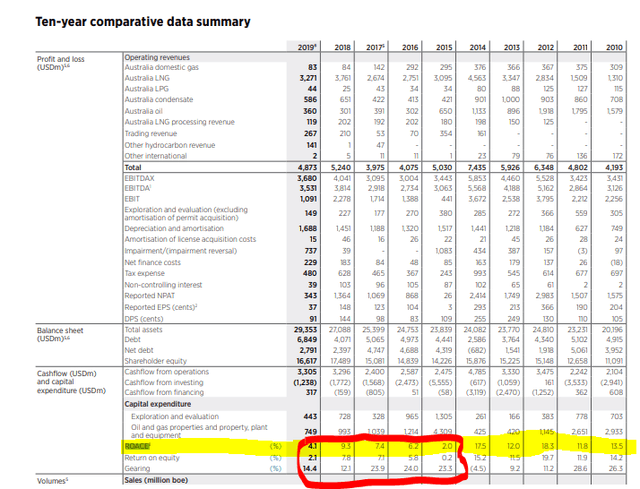

2019 free cash flows have been estimated at $2 billion.

Ok, in a normal year like 2019, Woodside makes $2 billion in free cash flow.

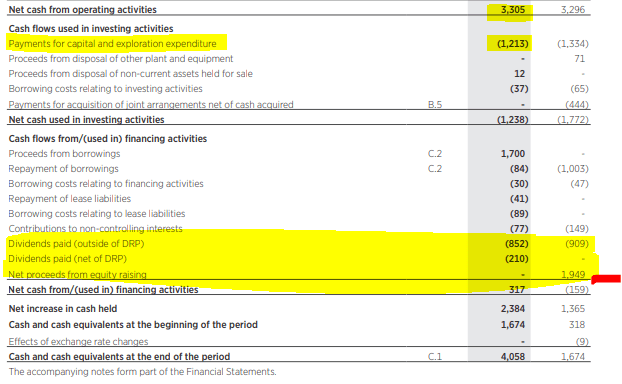

The company pays out $909 million in dividends in 2018 and at the same time raises $1.949 billion. What is the logic behind that?

Debt is manageable at 2.5 times free cash flows.

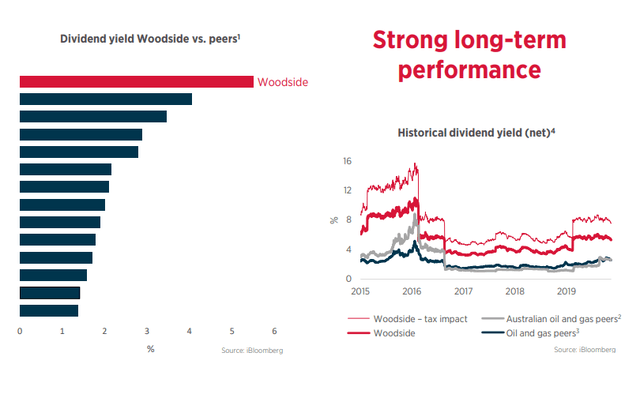

Woodside dividend – fully franked

If I were at Woodside, there would be no dividend. Them keeping high dividend payments really increase the risks of the business and the possibility that long-term returns continue to be negative. But hey, investors want dividends and managements will do all to cater for investors, even if it means jeopardizing the long-term financial health of the business.

As we saw earlier, with Woodside it is all about the dividend, they issue stocks to pay dividends, make investments with questionable returns but good momentarily cash flows to pay dividends. At some point in time this game might come to an end, and not even 20 years of dividends will save you, this is also reflected in Woodside’s stock price chart over the years.

Woodside is all about dividends, nothing more, but let’s try to make a valuation based on current numbers and likely future numbers.

Woodside stock valuation

I’ll first make a valuation based on 2019 numbers and LNG prices and I will come back to this and update when I have looked at more than 20 natural gas stocks when I identify the most likely long-term average range for natural gas and LNG prices.

Sustaining capital expenditures are expected to be around $400 million per years, let’s put $500 to be sure. I’ll take an average cost of debt level of 5% which is in line with the latest issued bonds.

If I use 2019 levels on future production, given the investments and the cost of debt of 5% I don’t get far, except for the $1 billion dividend payment. Plus, if debt escalates, cost of debt might go higher than the current 5% and that could be detrimental on the company as a going concern.

The problem is return on average capital employed, if the cost of capital is higher than the return, you are not creating much value for shareholders. And if I use 2019 returns, their investments will not be profitable and will not create value.

All in all, the most likely scenario is one where the company keeps paying a dividend over the next two decades. That is not bad, but not even something great, that is why the yield is relatively high.

Woodside stock investment thesis

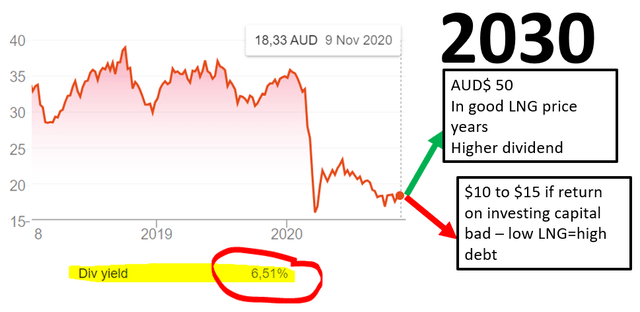

There is value with Woodside stock if and when oil prices and natural gas equivalents go to $65. Then, even if there are just a few good years, above average years, Woodside will deal with the debt, have huge free cash flows, increase dividends and the stock will likely triple. This is the investing upside, likely, possible and will happen here or there, but I don’t know whether it is sustainable in the long-term.

If natural prices don’t go up, and I don’t think it will happen except for, as mentioned above, certain periods, Woodside will not deliver great returns.

Woodside looks like value, but it isn’t, except for the $1 billion dividend there and the trading potential (nothing wrong with that).

Now, you might think there could be value if they don’t go further with their investments? Yes, but then there is just 8 years of production remaining, where the cash flows would just cover for the market capitalization and it becomes a timing issue on where will natural gas prices be over the next 8 years. So, Woodside could be called a fairly priced bet on natural gas prices, but a risky bet.

If they cut the dividend, then we could see positive free cash flows for new dividends somewhere in 2030, which means the stock could be valued at $30 billion in 2030 on a 7% required dividend yield.

No dividend would lead to better fundamentals and actual value within the business around 2030 with 3 billion in free cash flows. At a price to cash flow ratio of 10, the market capitalization would be 30 billion which is 3 times the current. That is a return of 11.6% per year, which is higher than the dividend – this is the reason why Buffett never pays a dividend.

Woodside stock investment conclusion

The more I look at natural gas stocks, the more I see that the market might have overreacted over the last 6 months. Many businesses are really not profitable with oil below $60, which means that prices will likely go up. Oil is not about to disappear that fast, especially LNG.

On Woodside stock, going back to the 4 investment lessons:

– Woodside offers value from a cyclical perspective, likely also a good capital return.

– The dividend is the focus, it increases business risks but it also rewards you – a mixed bag there.

– If the world keep using LNG, and it is likely demand will double over the next 10 years, the stock is value.

This Woodside stock analysis is part of my full analysis of the natural gas sector for my research platform. I am looking at stock by stock and recently I did something similar for the copper sector recently. If you wish to know more, please subscribe.