RDS Stock Analysis – A Buy But Be Careful (Not The Best Oil Stock)

This Royal Dutch Shell RDS stock analysis will give you an answer on whether RDS stock, at historical lows today, at lows not seen since 1994, is a buy, hold or sell. Here is the video analysis, article continues below.

RDS stock was very often required in the comment section of my videos but I never felt the need to look at it because it was usually a bit too expensive for me. Now, things have changed, unfortunately both on the stock price and fundamental side. Here is my oil price and environment analysis.

Two years ago, Shell was promising returns to shareholders of $125 billion through buybacks and dividends over 5 years. Since, this is what they delivered:

- Impairments of $17 billion

- A dividend cut that hasn’t been cut since World War II

- A stop in the much-loved buybacks

- And a staggering 65% RDS stock price decline

and,

- $25 billion returned to shareholders through buybacks and dividends in 2019.

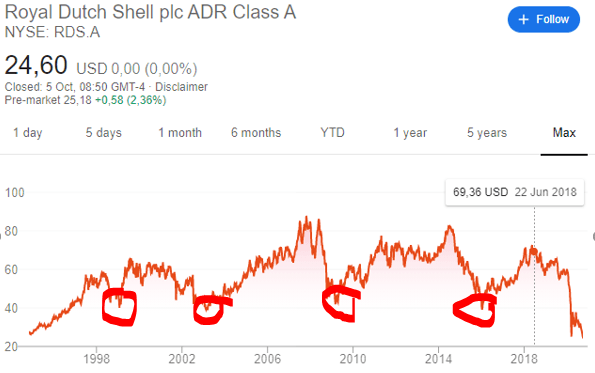

If we look at the long-term RDS stock price chart, those that bought when it looked like it was game over for Shell, in 2003, 2009 or in 2015, did great from a short-term investing perspective.

Let’s make a full RDS stock analysis and give an answer on what is the risk and what is the potential reward with RDS stock now.

RDS stock analysis content:

- RDS stock price overview

- RDS business overview

- RDS stock fundamentals

- RDS dividends and buybacks

- RDS stock cash flow valuation

- RDS stock investment risk and reward thesis

RDS stock price overview

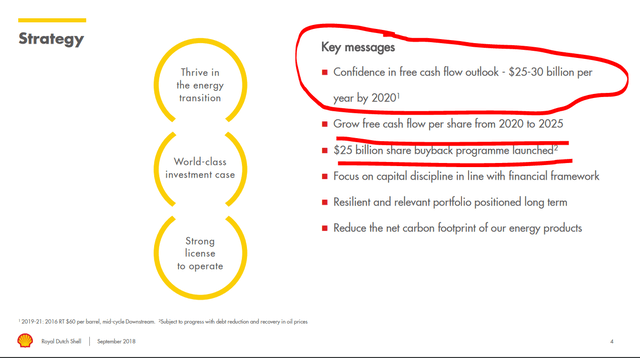

Over the past years, whenever I would look at RDS, I was stunned by RDS’s management statements. At the 2018 Retail Wealth Management conference the message was clear; the company will create $25 billion in free cash flows per year, do buybacks, increase dividends and reward shareholders immensely over time.

The $25 billion shareholder rewards implied a double digit return for shareholders through buybacks and a generous divided and many investors bought RDS stock that was above $60 at that point in time. It seemed that nothing could possibly go wrong with such a name, such a strong and big company, constant dividend growth and 2019 where they actually delivered on promises.

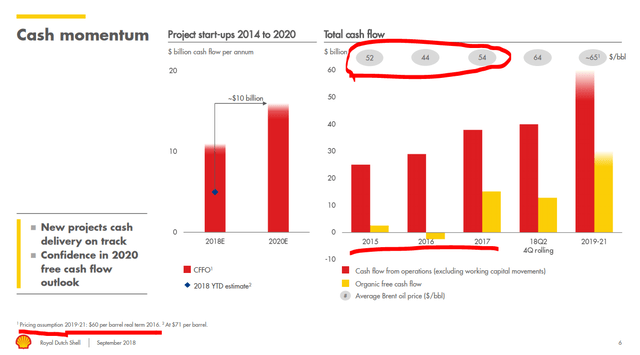

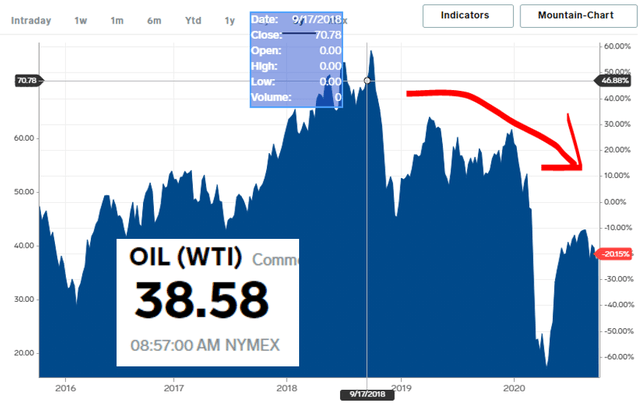

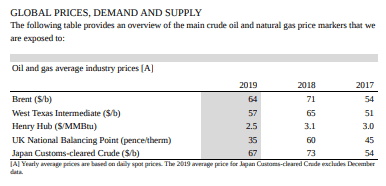

Shell’s the free cash flow assumptions were made on an oil price of above $60. The market didn’t care that in no year prior to 2018, average oil prices were above $60.

Since then, oil prices passed $60 for just two short periods in 2019 and then crashed in 2020 only to stabilize to the current level around $40.

Of course, nobody could have predicted what happened with COVID-19, but common sense tells me to always look at long-term cyclical averages, especially for commodities. My view was quite different back then because when I was looking at Russian stocks in the period where their future projections all considered an oil price of $40 and not $60 like RDS used. Thus, someone was a bit too exuberant or the other side was too conservative.

Russian oil producers have one focus, to increase the dividends paid as their management is not incentivized by increasing stock prices or any other metric through buybacks because the Russians are not under the influence of Wall Street, so just business there. On the other hand, Shell’s management incentive is to grow constantly, no matter the cyclical nature of the business, the cost of doing so or the risks involved – typical Wall Street pressure. Sometimes, the smartest thing to do is to liquidate a business, especially when it is at its best, but this is something not comprehendible within the current human investing mindset.

The oil industry is cyclical where when oil prices are high, everybody is pushing you to invest more. This leads to oversupply and low prices when everybody is pushing you to cut costs and save, that consequently leads to undersupply and that is why it is a cyclical commodity. Another reason to buy an oil stock when it is low.

Oil prices are low, much lower than what RDS expected and the consequence is that the company will not be able to deliver on the $25 billion per year of organic free cash flows promise.

What went wrong?

RDS business overview and outlook

When I look at Shell and its management, I always feel like they don’t live in the same reality. Then I think how I live somewhere in the mountains and I am the one wrong, but unfortunately for Shell, reality catches up with them soon. Let me give you a few examples and the first is related to people.

The CEO’s top quote on the 2019 annual report is about people and sustainability.

At the first sign of difficulty, the company decides to cut jobs. I guess the 9,000 losing their jobs didn’t have high hopes and social commitment.

On sustainability, probably more than 30% of the discussion in the annual report is about sustainability, climate change, hydrogen etc.

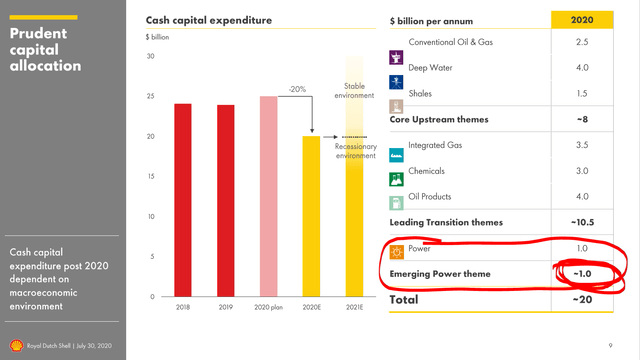

But then, if you take a look at capital expenditures, only $1 out of $20 billion will be invested for clean energy. The rest is business as usual.

And this is a problem I have personally had with RDS whenever I would look at them; a management I can’t trust because I can’t see the connection with reality in what they say, what they do, and what the market tells me is going on. Take a look at the investment spending in the upper right corner of the above figure; $4 billion for deep water and $1.5 billion for shales while we all know deep water and shale is not profitable at low oil prices.

So when I see their $60 long-term oil price projection, it simply doesn’t hold and the market has taken notice of that too. Consequently, the stock is down. But ok, let’s keep analysing.

RDS business fundamentals

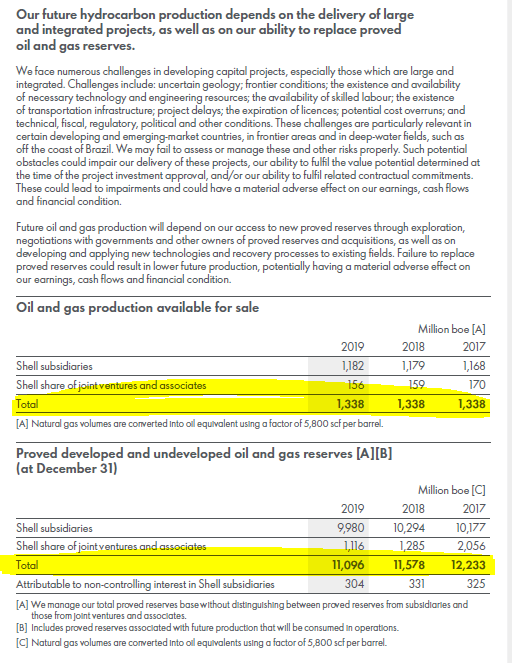

What I always look with a resource company, is how much production there is ahead because it gives me an indication of new necessary investments and long-term risks.

RDS is producing 1,338 million boe per year while the oil and gas reserves are 11,096. This means there are 8.2 years of production left at current rates. Plus, this includes undeveloped reserves which means there are still risks and costs to do that. Further, reserves have been declining over the last 3 years meaning how RDS is not capable of finding new profitable sources. On of the reasons the acquired BG in 2016 for $53 billion are lower production costs, to lower their high average.

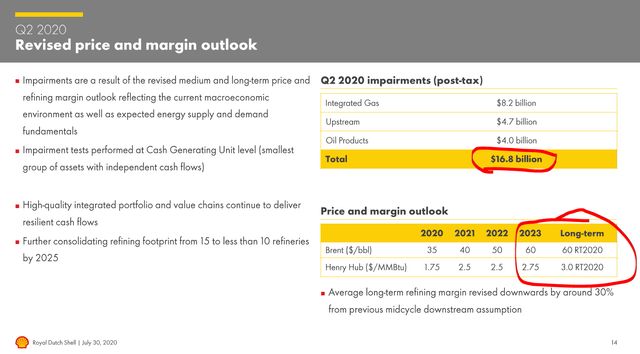

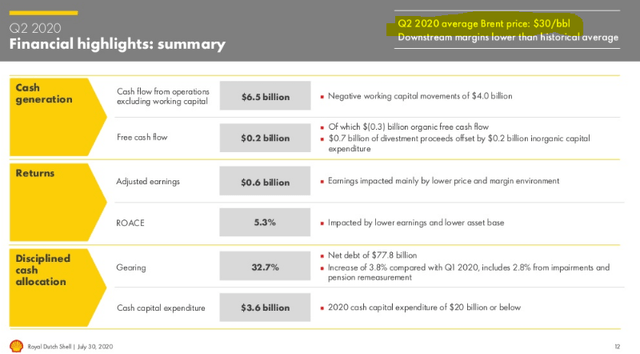

The most recent impairment in Q2 2020 was $16 billion because of lower expected oil prices. However, they still expect $60 from 2023 onward and long-term and this is the biggest risk for RDS stock; what if it isn’t $60, but $50?

These impairments and mistakes based on wrong oil price assumptions are not new for RDS. Another example is the Artic debacle where they spend more than $8 billion for nothing.

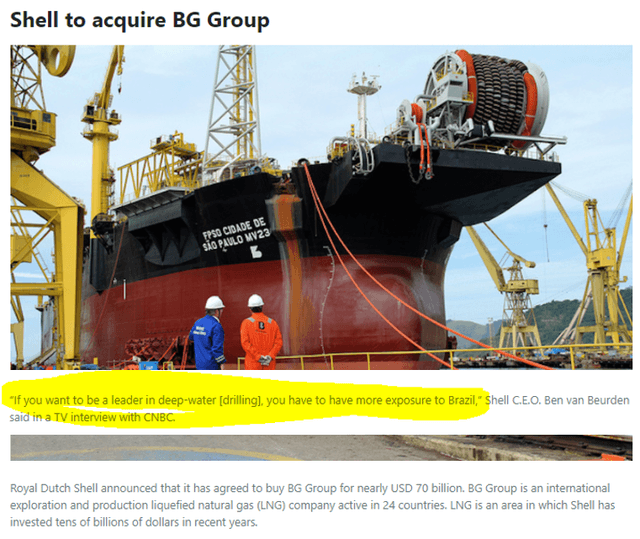

To have those more production options, RDS acquired BG in a $70 billion deal where the CEO of RDS said that you need to have exposure to Brazil for deep water drilling.

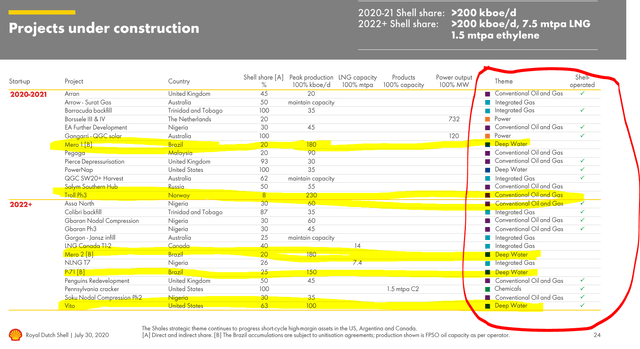

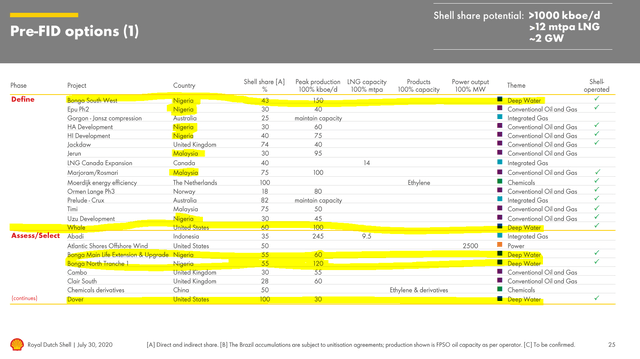

The problem is that deep water drilling is among the most expensive types of production and if I look at RDS’s options for future production, the biggest projects are mostly deep water ones.

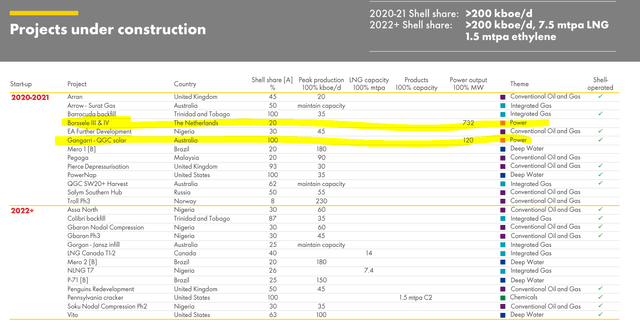

Going back to Shell’s big talk on renewables, only two projects in the mix, a solar in Australia where there is sun and solar in Borselle, Netherlands which is where my mother lived. She is now renting her house out there and I bet she has double the return on capital than RDS has.

The largest longer-term projects are again deep water and then even in Nigeria to make things more interesting.

On Shell’s business, I don’t think there is an upstream competitive advantage. On the downstream and chemical business, I feel the same, it all depends on oil prices but again you don’t have much of a competitive advantage.

RDS stock fundamentals

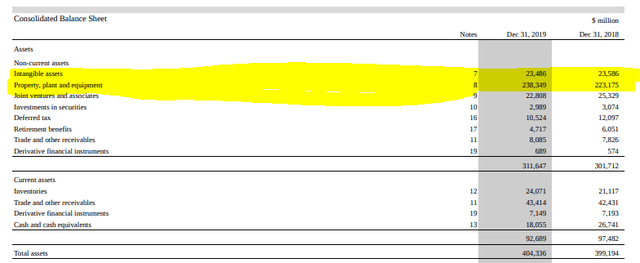

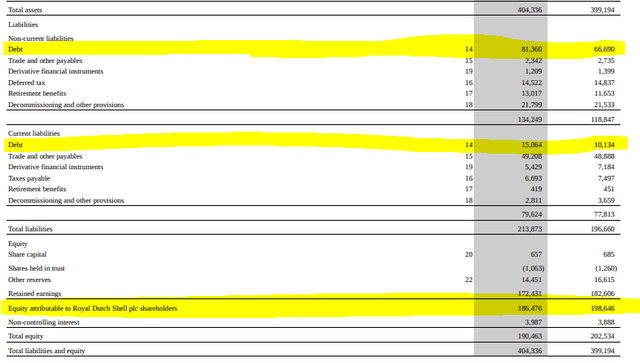

From a fundamental perspective RDS looks very strong with $404 billion of assets on $95 billion in debt.

However, the value of the assets shows what they had spent on them, not the long-term value in the form of future cash flows that will come back to shareholders. So, the $238 billion in property plant and equipment might not be $238 billion and we have already discussed the $18 billion impairment in the most recent quarter.

The stock is trading at a 0.537 price to book value, but investing is not about book values, it is about what will those book values produce in the future in the form of cash flows, thus dividends and buybacks.

RDS dividend and buybacks

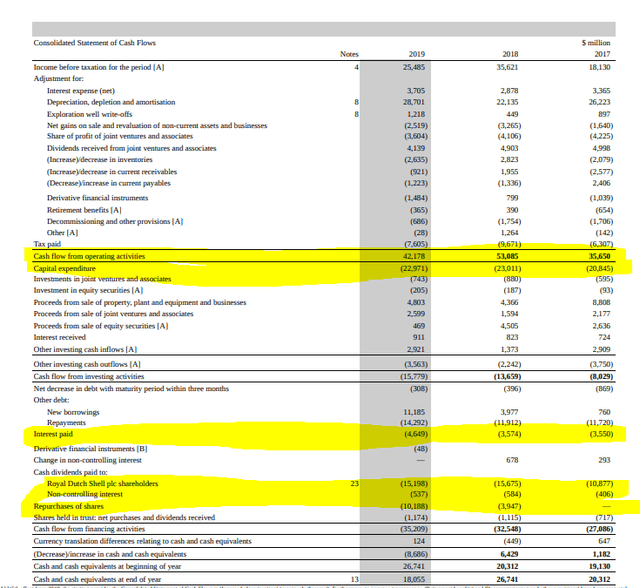

In 2019, the company did greatly, it paid $15.7 billion for dividends and did buybacks of $10.1 billion while the cash position went down just $8.6 billion. Cash went up $6.4 billion in the previous years so it almost evens out, but the buybacks were just $4 billion.

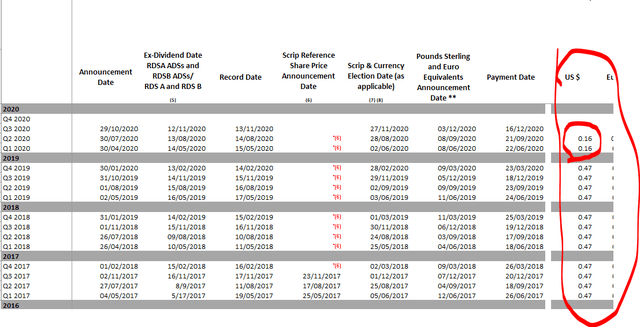

When it comes to dividends, they needed $16 billion per year to pay them. The recent two thirds cut brings that down to $5 billion. I don’t expect buybacks for a while.

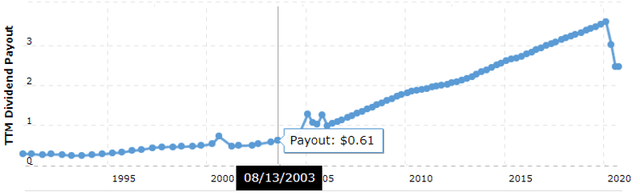

I don’t think the dividend growth story will continue, this cut is likely not to be temporary and all those dividend investors that have based their investment decision on 30 years of dividend growth, are likely going to be hurt the most.

Whether RDS will pay higher dividends depends on available cash flows that depend on oil prices.

RDS stock in the oil price environment

It all depends on oil prices. When oil prices are at $60, RDS can make $20 billion in free cash flow, at $70 we are already closer to $30 billion as it was the case in 2018.

However, at $40, they don’t make much money at all. RDS managed to reach free cash flow of 0 thanks to savings and lower investments.

This is how I see the situation, with oil at $60 RDS does good, $20 billion in FCF, with oil at $40 RDS will make practically zero.

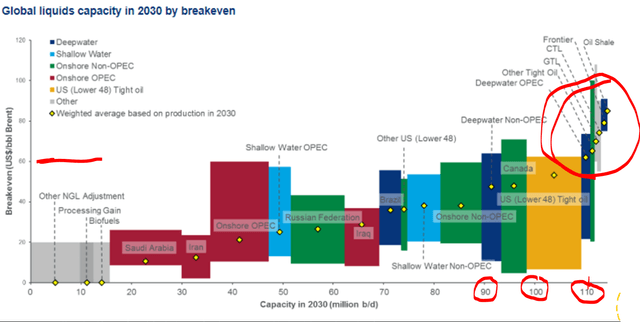

The name of the game is to determine what will oil prices be in the long-term. Shell’s forecast is $60, some use $40 for their calculations while some say oil has to go to above $80 to justify new investments to keep production up and cater for demand. The sad truth is that if there will be a structural decline in demand, or lower than expected growth in demand, oil can easily be at $40 for longer. Production costs on average are just above $30.

Oil prices are set by the marginal producer, and the cost curve is pretty steep, which means that in case of slightly lower than expected demand, prices will be much lower. A few million barrels of oil per demand can make the difference between oil at $80 or at $50. Plus, what is usually the case with oil, if prices go above $60 or $70, suddenly you find the supply that is going to cover the gap quickly.

Let’s put the above into a cash flow valuation for RDS and see what is the market pricing in.

RDS stock cash flow valuation

If I take Shell’s estimates of an oil price at $60 for the long-term, alongside the assumption that all their growth projects work as planned and that they can expand their resources, I get to a present value of $200 billion by using a discount rate of 8% and a terminal value in 2040 of $100 billion. This doesn’t include the $100 billion of debt that will have to be repaid one day given that oil demand will likely be much lower in the future.

If oil continues to be used as it is now, RDS is undervalued by 50% at least. Unfortunately, that is not what the market is pricing in because the market capitalization is half the valuation.

If I take average oil prices at $50, assume $7.5 billion of free cash flows for RDS long-term and a terminal value of $50, the sum of present values is down to $80 billion which would make RDS stock overvalued even now.

I feel this is the future for oil over the coming years, to trade within a range between $40 and $60 with short spikes above and below that which is what the market is pricing in.

It is not really about COVID, it is about the fact that things never happen linearly. We were at the local farmers’ market today and everybody stopped for a second to listen to the silence of a hybrid Lexus passing. EVs are slowly creeping up, but when they start to really get traction, it will not be linear as many expect. If oil demand drops from 100 to just 95 million barrels a day, oil prices might tend towards $40 over the long-term.

From a free cash flow perspective, despite the fact that the stock is at decade lows, RDS is still overvalued.

RDS stock investing conclusion

One of my favourite investing truths is that you should invest in sectors with tailwinds not because you might get to great returns, but because if you make a mistake, it is likely to be less costly than when investing in a sector with headwinds.

The oil sector has many headwinds which increases the losses in case you make an investing mistake. Two years ago many were asking me about tobacco stocks so I made an analysis of Altria stock and said how it simply doesn’t pay to invest in sectors with headwinds because what is cheap can get much cheaper. I think oil stocks are in the same pickle as tobacco stocks.

This means that we have to expect a lot of volatility because small changes in oil prices will have huge impacts on cash flows and consequently valuations. Plus, what Wall Street doesn’t know how to do is to not apply the current situation and perception to eternity. If oil prices reach $60 in 2022, Wall Street will calculate $60 forever for oil. That moment, will be the time to get out if you are deep in oil stocks now, because oil will likely hit $60 again someday, but it will not stay there for long.

To summarize my analysis on RDS stock:

- Expect a lot of volatility as small oil price changes have big impacts on valuation

- Take advantage of the fact that Wall Street doesn’t know to think long-term, thus it might give you another chance to get out when oil prices hit $60 and all expect them to stay there, they will not.

- Oil is a sector with a negative headwind, thus the only sleep well stocks to buy are extremely low-cost producers but those trade in Saudia Arabia, Russia and perhaps Norway that has a 74% oil profit tax.

- Unfortunately, I expect things to remain ugly for RDS over the long-term because their touted transformation into a green company are just words where the investments are just 5% of their total CAPEX.

I prefer other sectors like natural gas, copper or emerging markets for long-term investment opportunities. More on Sven Carlin Stock Market Research Platform.