Semperit AG stock analysis – high dividends ahead

Semperit AG stock analysis is part of my full, stock by stock analysis of the Austrian Stock Market that offers interesting investing opportunities. Check my Austrian Stocks List for more Austrian stocks.

Semperit AG stock is a manufacturer of industrial rubber and plastic products. Every second escalator handrail in the world is made by Semperit. Another major business segment is medical gloves manufacturing.

Semperit stock price analysis – VIE:SEM

By just looking at the stock chart, we could sense a kind of cyclicality. Additionally, the main market is in the industrial sector. Therefore, Semperit’s stock can be categorized as cyclical in the Peter Lynch stock categories. Let us look at the business model, the fundamentals and give an outlook.

Business fundamentals of the Semperit AG stock

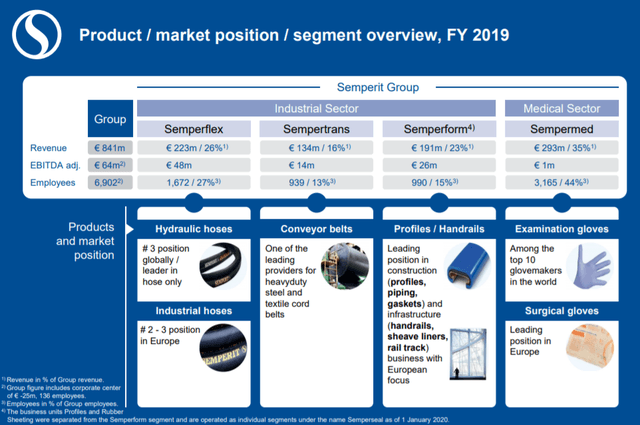

Semperit operates in the industrial sector with three business segments and the medical sector with one business segment.

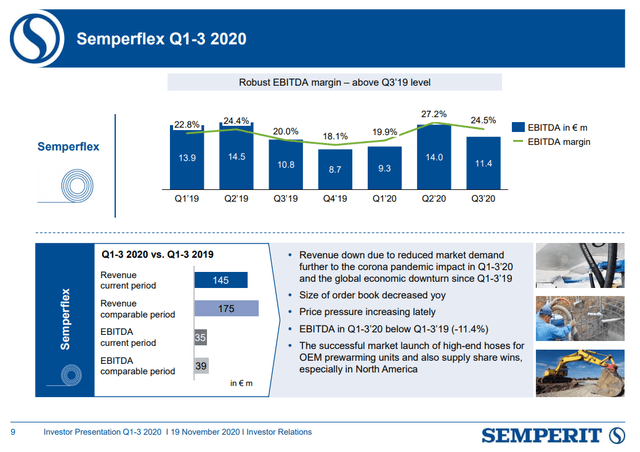

Semperflex develops, produces, and sells hydraulic and industrial hoses worldwide. With hydraulic hoses, it is possible to transmit pressure and energy in heavy-duty machinery (cranes, for example.) The use for the hoses is in the construction and transport industry, as well as for mining and agricultural machinery. Demand for the products depends on infrastructural investments and the growth in the mining and agricultural sector.

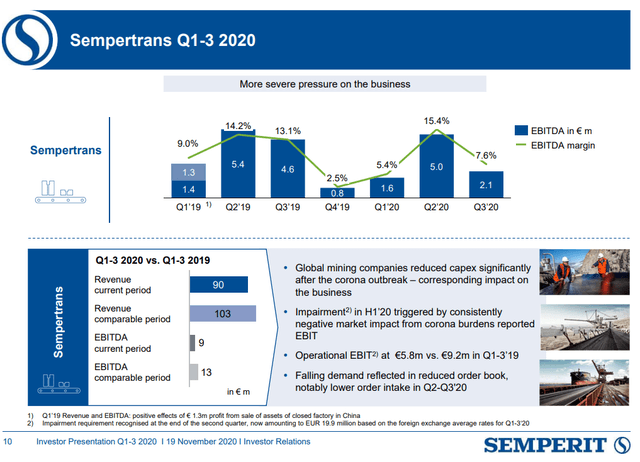

Sempertrans produces conveyor belts for the mining, steel, cement, and transport industry. The demand is in correlation with the demand for raw materials extracted and transported via conveyor belts.

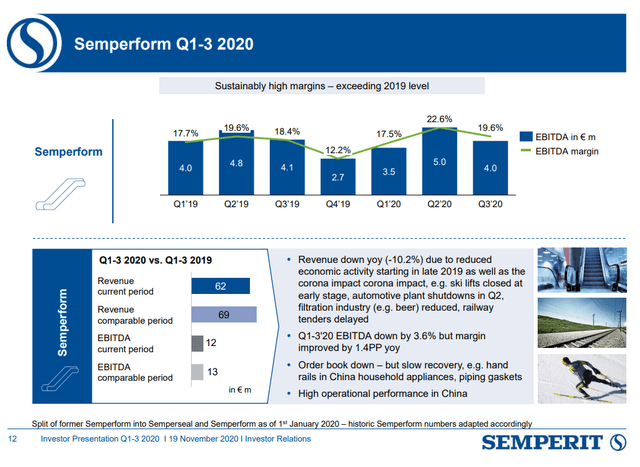

Semperform produces molded and extrusion products made of rubber and plastic. The products range from insulation profiles for windows, doors, and facades. Other products are escalator handrails and vibration reduction foils for skis and snowboard, and custom molded parts. Demand is here also dependent on investments in infrastructure and the trend of urbanization.

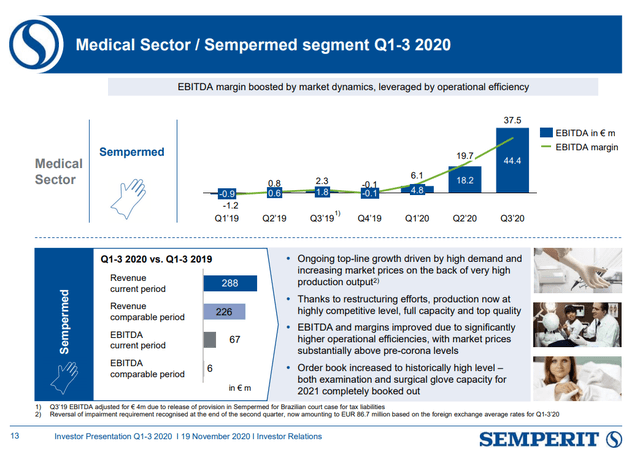

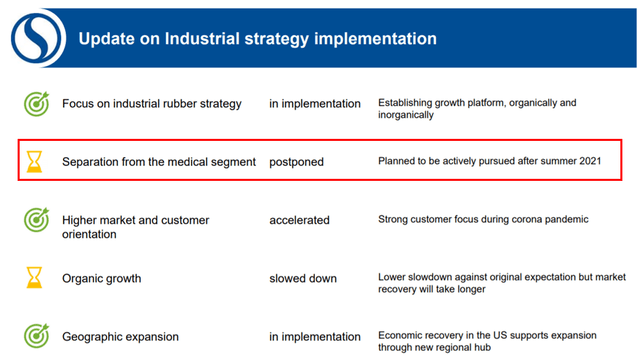

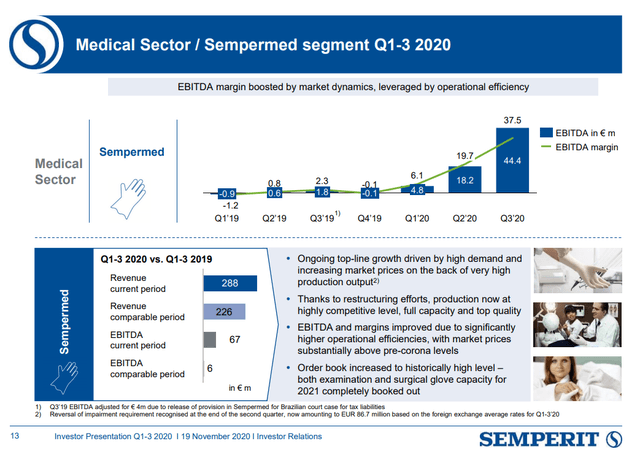

The medical segment (Sempermed) produces surgical gloves in the medical area and protective gloves in the industrial area. Increasing health and hygiene requirements resulted in the global growth of 6 % to 7 % annually. In January 2020, the management decided to separate the medical business and transform it into an industrial rubber specialist.

As the Covid-19 pandemic started to gain track, the management quickly postponed their decision till summer 2021. The management expects the Corona price premium to continue into 2021. Consequently a reversal in impairments of 88 million EUR was made.

Semperit Stock Dividend

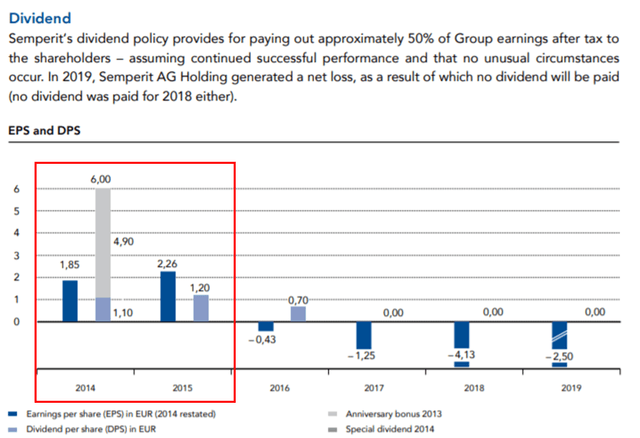

Semperit’s dividend history does not look that great. 2014 was an exciting year as there was an anniversary bonus dividend and a special dividend.The general dividend policy is to payout approximately 50 % of earnings after tax. Earnings were negative since 2016, and therefore the dividend got cut. But the 7.84 EUR dividend in 2014 and 3.46 EUR in 2015 look extremely tasty compared to the current stock price.

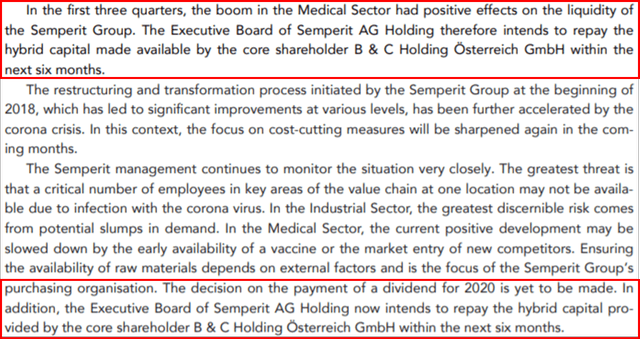

Another burden on the dividend is the hybrid capital from its core shareholder B & C (130 million EUR). The priority of Semperit seems to be to make their core shareholder happy, not with dividends, but with the repayment of the loan and interest.

B & C owns 54 % of the stock and has strong voting power within the company. The primary focus of B & C is fostering Austrian entrepreneurship and have signed a long-term commitment.

Semperit had to pay 10,5 million EUR in interest in 2019, which equals a rate of 8 % for their long-term partner B & C. The other shareholders got no cash flow returned. Additionally, Semperit now has the priority to repay the 110 million EUR in the next six months before they plan to pay a dividend.

However, if things continue as those are, the hybrid debt will soon be gone and there will be much more left for dividends and given the 500 million market capitalization, they yield could be substantial.

Semperit stock analysis – financials

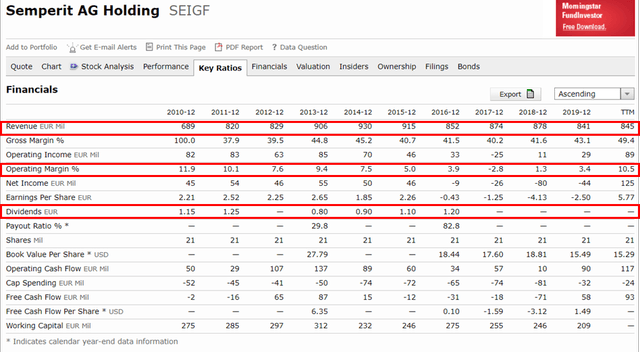

Revenues increased by 200 million in the last ten years — slow but steady growth. In good years (2011 and 2013), the operating margin is around 10 % as it is now. The stock price reached highs of 44 EUR per share (24 EUR now). If Semperit decided to pay out a dividend of 1,25 EUR as in the last good years, this would equal a yield of 5 % now.

Semperit Stock Financial overview – Source: Morningstar

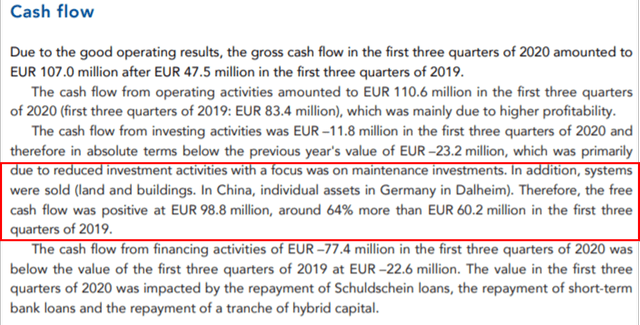

In the three-quarters of 2020, Semperit earned 111 million EUR in operating cash flow and had 12 million EUR for investments. In the annual report of 2019, Semperit estimated CAPEX of 40 million EUR. Therefore, we should act conservatory and take 40 million for their CAPEX.

For 2020 the free cash flow will result somewhere between 70 and 100 million EUR. On the market capitalization of 520 million EUR, this equals a free cash flow yield of 13 % to 19 %.

Investing cash flow was low because Semperit sold land and buildings in China and Germany worth 5 million EUR and did not invest much in their own business.

In summary, Semperit has 110 million EUR in operating cash flow. 40 million EUR are for CAPEX expected. Potentially there is 70 million EUR in free cash flow available for shareholders. Their long-term debt is 245 million EUR, 17 million EUR from the current liabilities, and 110 million EUR in the form of the hybrid capital equaling 372 million EUR in debt. Minus 157 million EUR in cash gives a net debt of 215 million EUR. In good years this is about 3 times free cash flow and, therefore, a reasonable debt.

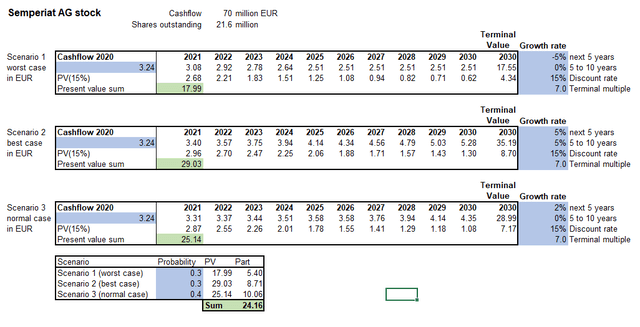

A cash flow model will give a rough stock price valuation. This model’s general assumptions are a discount rate of 15% and a terminal multiple of 7. These figures are estimated conservatively as no recession, or economic downturn is considered. The model uses the free cash flow to be more on the safe side as the current earnings per share of over 6 EUR is quite unusual.

In the model below are three scenarios:

- Scenario 1 (worst case): 5 % decline for 5 years and then 5 % growth with 30 % probability

- Scenario 2 (best case): 5 % growth for 10 years with 30 % probability

- Scenario 3 (normal case): 2% growth for 5 years and then 0% growth with 40 % probability

Based on this model, the investor could expect a return of 15% annually with the current stock price and the above assumptions.

The problem with the above is the possible reversion to the mean for the medical segment and lower for longer industrial margins. If EBITDA for the medical segment returns to 2019 levels, we can deduct more than half o f the free cash flows of the company. Production capacity is fully booked going into 2021 which is good, but when things normalize, one should expect lower cash flows.

The medical business was so great that the plan had been to sell it in January 2020 because of low profits. They have postponed the sale and it will be interesting what EBITDA they get. At normal 10 times EBITDA sales, just this sale would cover the market capitalization, but we all now the party has to end soon and you have no competitive advantage withing medical gloves.

Semperit AG stock investment outlook

As seen on the stock chart initially, Semperit is ready for continuous stock price acceleration. The bottom of the cycle seems is passed, and now it is the time for the potential upturn.

If they get a good price for the medical business, they will be able to reward shareholders very well.

The other parts of the business should lead to cash flows of around 30 to 50 million per year and be valued around 500 million. So the upside depends on the profits from the medical business sale. I feel there is more upside but the stock price is moving up so fast that I don’t know what to think about it.

Let’s say they get 5 times 2020 EBITDA for the medical business, that still leaves us with a 300 million valuation based on free cash flows for the other businesses. This makes the stock undervalued at the moment, but at the end it boils down on whether you with to own a business like Semperit in your portfolio.

Given it is a pure cyclical stock, the best is to buy such stocks at bad economic times, it is not really a hold forever stock because of the cyclical nature, you can leave the holding forever to pension funds.