Polytec Stock Analysis – A Cyclical Automotive Play If You Wish To Make Money on Pension Funds

Polytec Holding stock analysis is part of my full, stock by stock analysis, of the Austrian Stock Market that offers interesting opportunities like Polytec stock is too. Check my Austrian Stocks List.

Polytec Holding AG is an Austrian automotive supplier and plastics processor based in Hörsching (a small town with 6.200 inhabitants). With around 4.300 employees in 27 locations, the company achieved sales of around 630 million EUR.

Polytec stock price analysis

Polytec went public in 2006 but was not an ideal investment for long-term investors. Without taking dividends into account, a loss of just under 18% would have been the result from investing in Polytec stock.

Currently, the stock is down around 70 % from its peak in late 2017. But as you can see by the indicators in the chart above, there were some phases with high potential returns in the 15 years of history since Polytec stock has been listed.

For example, the stock went from 1 EUR during the financial crisis to the highs of 2011 with around 8 EUR. The other time Polytec stock did really well would have been from 2016 and 7 EUR to the all-time-high of 21 EUR in 2018.

We could categorize Polytec stock a clear cyclical because it depends on another cyclical industry, the automotive industry (see business fundamentals).

However, from an investment perspective and possible upside, Polytec stock could be interesting as a Peter Lynch cyclical stock investment. The blue line is indicating the stock did not drop below 5 EUR for long, not even during the 2012 European crisis that could be indicate a bottom. Could a cyclical rebound happen in the next few years? Let’s look at the business fundamentals, the dividend, and the valuation.

Polytec Stock Analysis – Business fundamentals

Polytec is a complete supplier in the injection molding field and is a specialist for fiber-reinforced plastics. The product range consists of the painted exterior (Car bumpers), powertrain acoustics (soft engine cover), underbody solutions, new mobility products (battery box for hybrid vehicles), and truck/bus/Agricultural application (engine hoods).

Their vision is “We are European industry’s first point of address and preferred supplier with regard to trendsetting plastics solutions of the highest technological standard. Our primary focus is on the automotive sector.” With this explanation, the argument of categorizing the stock as a Peter Lynch cyclical stock is even more substantiated.

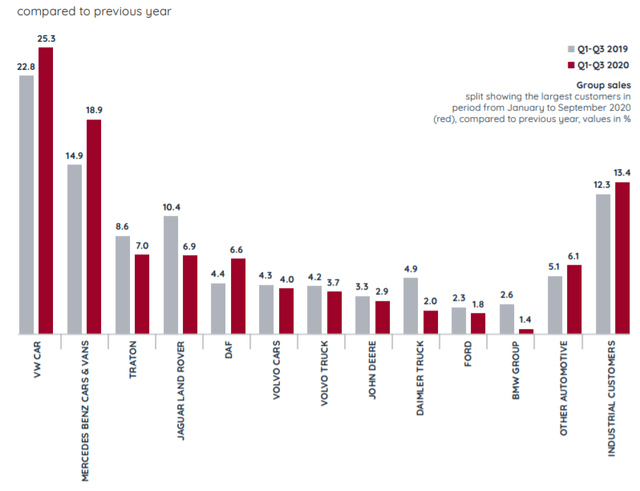

The company is selling its various plastic products to the automobile industry. As you can see below the biggest customer with 25 % is VW, followed by Mercedes Benz with around 19 %.

Their whole sales depend on cyclical industries (80 % automotive and 20 % industrial customers) and the automotive industry is not the fastest growing one, except for EV that are even taking market share and negatively affecting old supply chains.

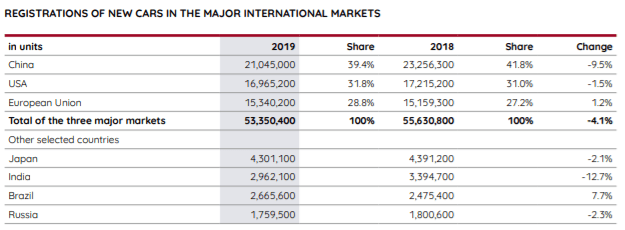

Their biggest market in China saw a decline of 9,5 % in 2019 and the European Union grew by 1,2 %. One emerging market is a special interest – Brazil. The growth was exceptional with 7,7 % but emerging market economies are also often volatile.

Many major market players are preparing for lower production and expect an upturn earliest in 2025 according to Polytec’s annual report.

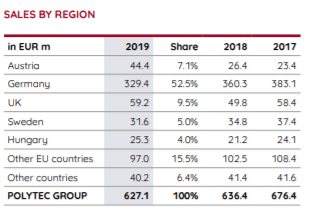

For Polytec the biggest market is Europe because just 6 % of sales are in other countries outside of Europe. Therefore, they can not participate in the growth of emerging markets. This issue is visible in the income statement.

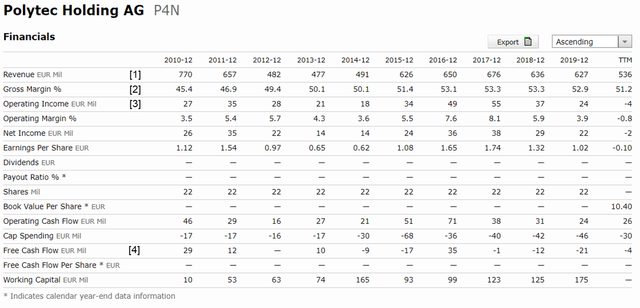

Since 2010 the revenue [1] has been declining and 2010 was Polytec’s revenue peak. The positive here is that they could increase their gross margin [2] from 45 % in 2010 to nearly 53 % in 2018. Improving gross margins unfortunately did not change much with operating income [3] as it was volatile over the years and declined in comparison to 2010.

Polytec dividend

The company is paying out a dividend. Free-cashflows [4 above] are positive in good years and then for many more bad years in the slight negative.

Even before the Covid-19 crisis, the dividend got a cut of 37,5 %. The reason for the dividend cut can also be found in the slow growth of the European automotive market.

From a stock price perspective, in 2016 the dividend yield was about 5 % and after that Polytec’s stock price rose where the yield got back to 3 %. A high dividend yield without a major stock drop is an indicator of an interesting potential buying opportunity for the short-term.

Polytec fundamentals – Margin of safety

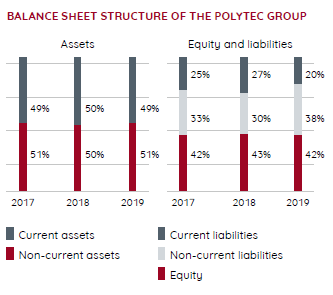

Long-term debt increased but in general the equity ratio in a solid and healthy. Polytec has 61 million EUR in cash on its balance sheet. With this cushion, a second COVID-19 wave can be survived and the solvency should not be a problem for the company.

99.2 % of all non-current and current interest-bearing liabilities to banks are in EUR and have an average nominal interest of 1.24 % which is a good financing rate for this cyclical company.

Polytec stock investment outlook

Polytec has a solid balance sheet and is very cyclical due to its business model targeting the automotive industry as its main market. Polytec will not be bankrupt in the next few years. The business can peak with a growing automotive market.

In a good year, the business can reach a net income of 40 million EUR that would give a price to earnings ratio of just 4 given the current market capitalization of 158 million EUR. I don’t think the stock would than trade at 7 and would probably double to 14 EUR. The book value per share is 10 EUR so there is a margin of safety there but keep in mind this is a cyclical, the best time to get in is when things start improving and a new growth stage of the cycle begins. Easy to say but hard to nail.

Thus, the company is not suited for the long-term investor as the dividend does not bridge the waiting time for an increase in the stock price. But for savvy investors, it could be a possible short to middle-term play if the price drops way below 5 EUR to levels seen in March 2020 of about 3 EUR. Keep in mind that when the fundamentals improve, European pension funds start buying, especially as the market capitalization increased, which gives a significant cyclical opportunity for us retail investors.

The main risks is that the European automotive industry doesn’t recover, but that is how it always looks with cyclical businesses. Keep in mind, the best buys are always made when the business and industry outlooks are the worst.

See how it fits your portfolio and investment style.

If you enjoyed this analysis and would like to get notified when I write more such analyses, please subscribe to my newsletter.