FSTR Stock Analysis – Only At Single Digits

FSTR Stock Price – L.B. Foster Stock

Up till now I have analyzed only railroad stocks (check the complete railroad stocks list with detailed analysis) that did well over time like Canadian National, Canadian Pacific and CSX. L.B. Foster (NADSAQ: FSTR) is not a railroad stock per se, but it is related to the sector. However, it is one that didn’t reward shareholders over the last years.

FSTR stock analysis content:

- Business overview

- FSTR stock fundamental analysis

- FSTR investment thesis

This FSTR stock analysis is part of my full railroad stocks sector analysis. Here is the:

If you prefer enjoying a coffee and listening to the content, here is the video on rail stocks, FSTR article continues below.

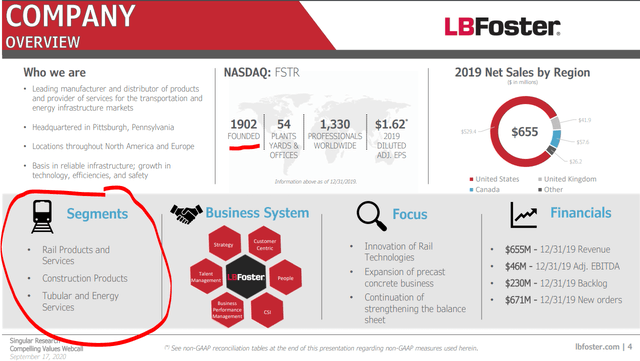

L.B. Foster business overview

One might say that FSTR is not a railroad stock but as its main business focus is railroad and energy construction, it is a great proxy to understand what is going on in the whole sector. Plus, on one hand we have railroad stocks at all-time highs while related stocks like FSTR are at decade lows. The market can’t be right for both, let’s see where the irrationality is.

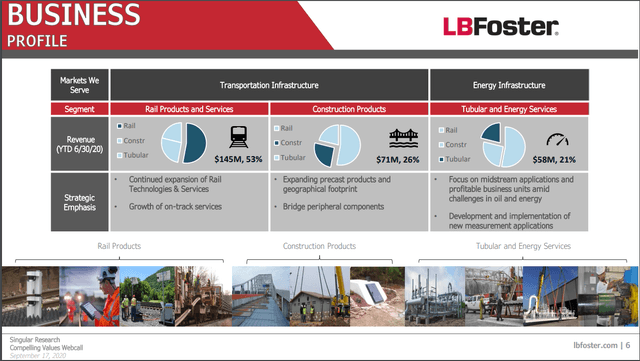

53% of revenue comes from rail products and services, 26% from construction and 21% from tubular and energy services.

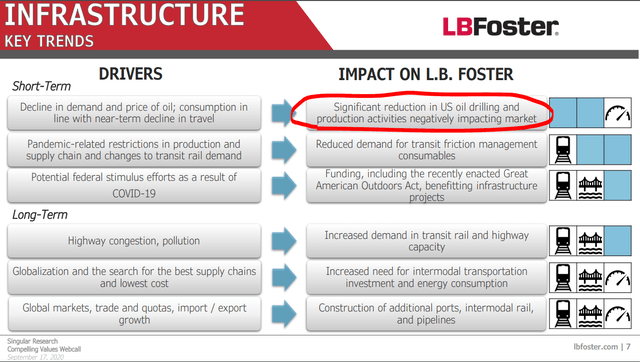

A big hit for FSTR is the decline in oil production. With oil at $40, it is not really smart to develop new shale oil fields where breakeven is around $60, so there is much less demand for all the related infrastructure. The hope is that there will be more need for infrastructure in the U.S. especially if the government provides the much-needed stimulus.

From a business perspective, it depends on how the oil markets develop, how ingenious will the company be in finding new sources of revenue and in general on the economy and government activity. As all of that is hard to predict, perhaps the best way to approach FSTR is to make a value analysis focusing on the possible downside and leaving all the good that can happen to be a positive surprise.

FSTR stock fundamental analysis

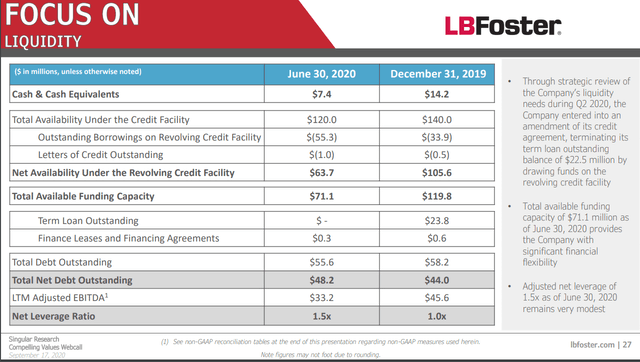

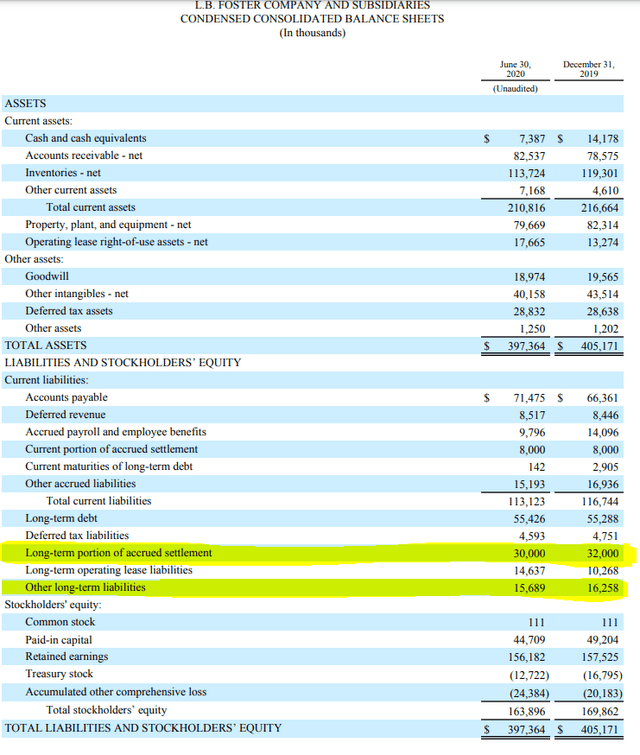

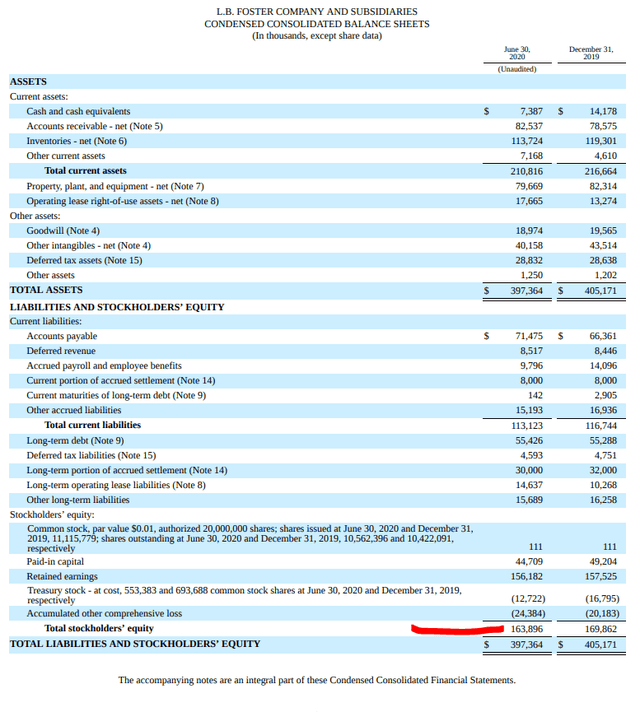

Let’s start with the debt analysis. What they say is that they have $55.6 million in debt outstanding.

But if I take a look at the balance sheet, is see another $50 billion in liabilities that they have to pay over the coming years.

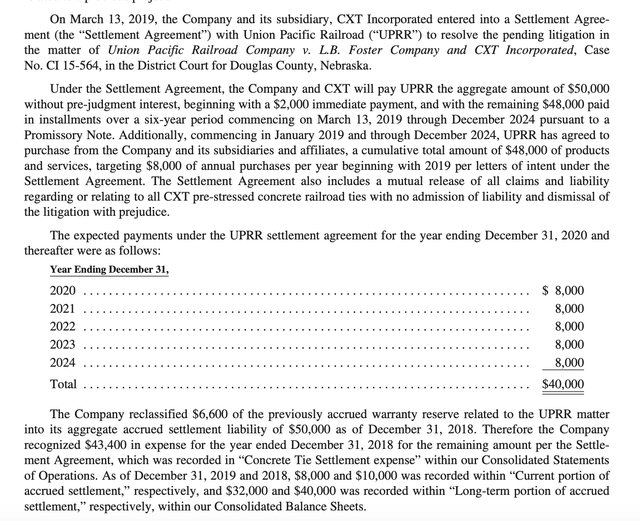

The liabilities arise from a settlement with Union Pacific where they agreed to pay $50 million over the coming 4 years. Union Pacific will also purchase equipment from that at for the same amount, but it is still debt.

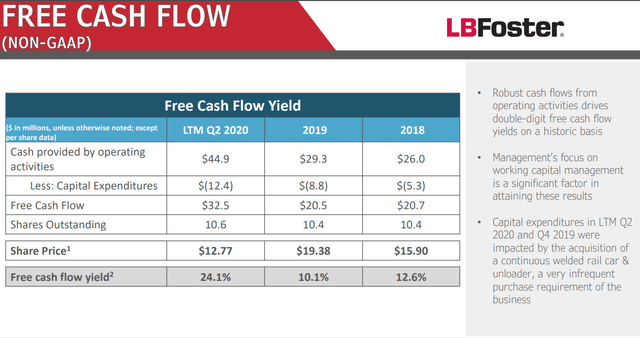

They also say their free cash flows are relatively high compared to the market capitalization of just $140 million. That sounds amazing and a cash flow yield of 24.1% is something I would put all my money in immediately.

However, there is the investor presentation and there is the real boring cash flow statement.

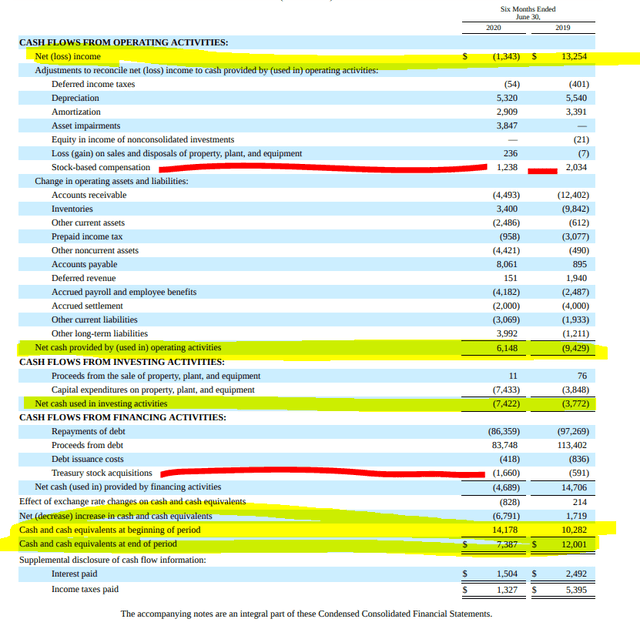

A look at the cash flow statement tells me they cash position went down $7 million over the last 6 months and had been up just $4 million over 2019 which was a good year for the business, so to say.

I see some stock buybacks (red) but I also see a higher amount within the stock-based compensation account, so there is not really a benefit there.

Given the situation it is unlikely the company will pay any dividends soon and therefore the situation doesn’t look bright. But, the best investments are usually made when things look the ugliest. For that you need a margin of safety.

Book value per share is $16.26 so the stock is trading below book but given that book value is made of $113 million of inventories, $18.9 million of goodwill and another $40 million of other intangibles, I would not take the book value at face. Therefore, the book value can’t be considered a margin of safety in this case.

By removing the $60 million of intangibles, impairing inventories a bit, I would say that a margin of safety book value is around $10 for the company and if you wish to make a margin of safety investment, you should wait for single digit stock prices.

L.B Foster stock investment analysis

FSTR stock is a small cap with a market capitalization of just $140 million. Therefore, it is overlooked by Wall Street which is good if things start to improve over time. However, the management said how their priorities are to deleverage the balance sheet and then, if possible, do acquisitions. Thus, they have no interest in paying dividends for now. The only option to make money here would be through an acquisition but that would also require an interested buyer. As the company isn’t really producing great cash flows, is in a declining business with oil headwinds, who knows when and if will that buyer come.

All in all, an investment in FSTR depends on the price paid. A logical buy would be when the downside is limited and the only thing left is upside. From a book value and from a technical stock price perspective, we are talking about single digits.

Below $10, FSTR would be a nice fit to a diversified Graham style value portfolio. The thing is that one buying FSTR must be ready to hold through an indefinite period of ugly before being rewarded when and if the cycle for L.B. Foster turns.

For more information on other railways stocks, please check my comparative railway stocks article with links to detailed analyses such as this one.

If you like this comprehensive approach to investing, please subscribe to my newsletter to be notified when I analyse a new sector. To check my past analyses, covered stocks and portfolios, feel free to check my Stock Market Research Platform.