Canadian National Railway Stock Analysis (Good Business)

Canadian National Railway stock – NYSE: CNI, TSX: CNR

Canadian National Railway CNI stock analysis content:

- CNI stock price analysis

- CNI business overview

- CNI financials and fundamentals

- CNI dividend and buybacks

- CNI stock valuation and comparison

This Canadian National Railway stock analysis is part of my full railroad stocks sector analysis. Here is the:

If you prefer enjoying a coffee and listening to the content, here is the video on rail stocks, CNI article continues below.

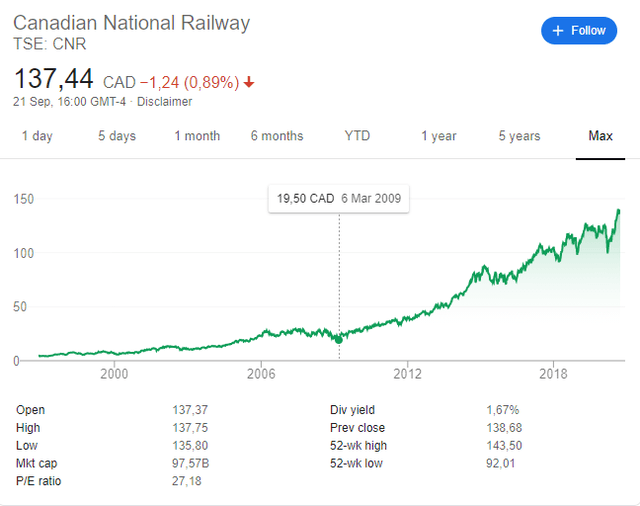

Canadian National stock price overview

As it has been the case with other railroad stocks, CNI shareholders have been greatly rewarded over the last decade.

Canadian National Railway stock market capitalization is $73 billion or CAD $97 billion. The stock is already above its pre COVID-19 peak and it looks like nothing can stop it from going higher. Let’s take a look at the business and fundamentals to see what are the expected returns from investing in CNI stock now.

CNI stock analysis – business overview

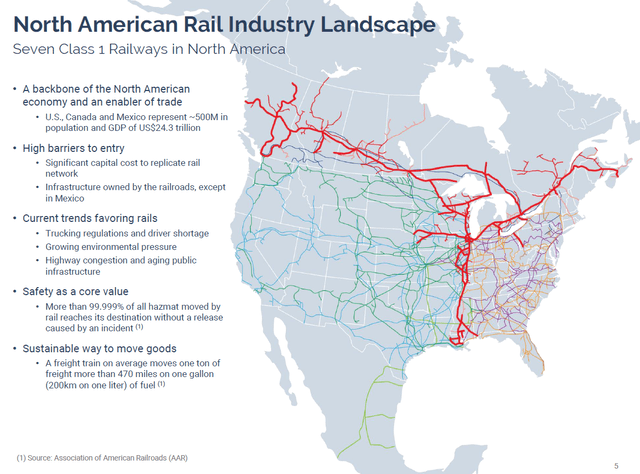

CNI is one of the seven class 1 railroads in North America.

Like with the other Canadian Railroad Stocks we analyzed, most of the traffic comes from commodities, which could be a positive if and when commodities end their downward cycle.

Growth ahead depends on operational improvements and improved services to capture as much business as possible.

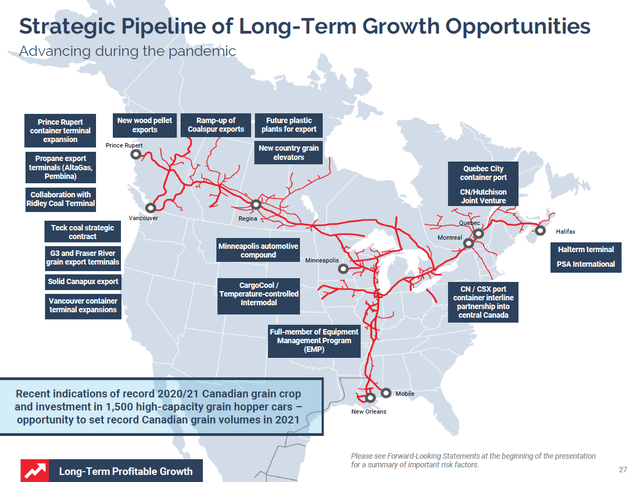

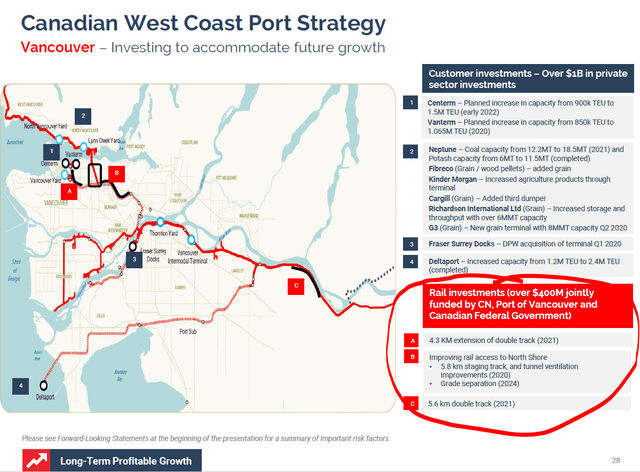

Here is an example of the growth projects the company is engaging with.

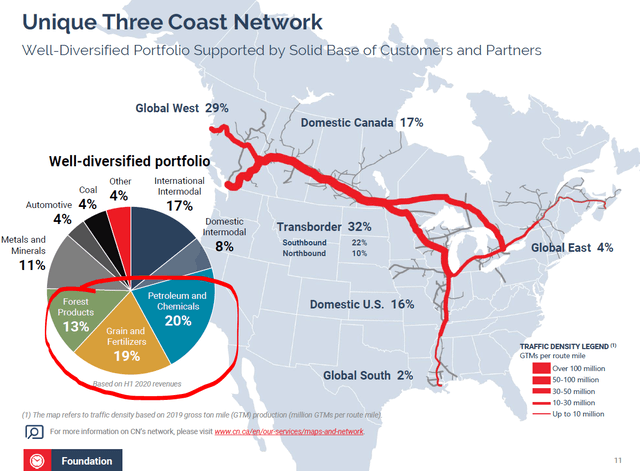

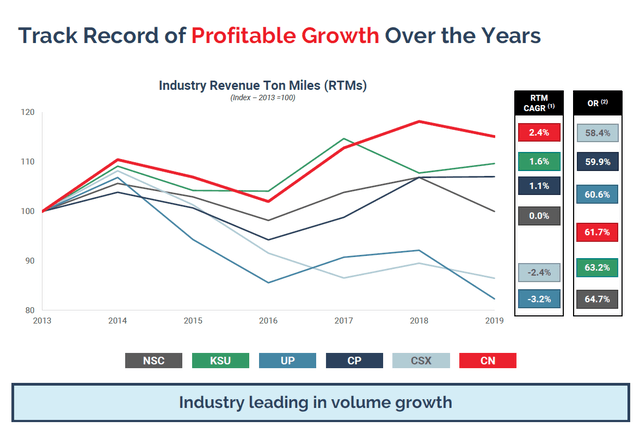

The company’s position allows it to increase revenue per ton, an advantage not all competitors have.

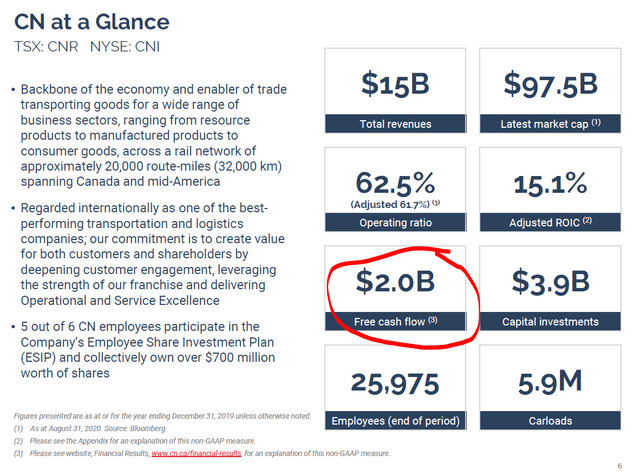

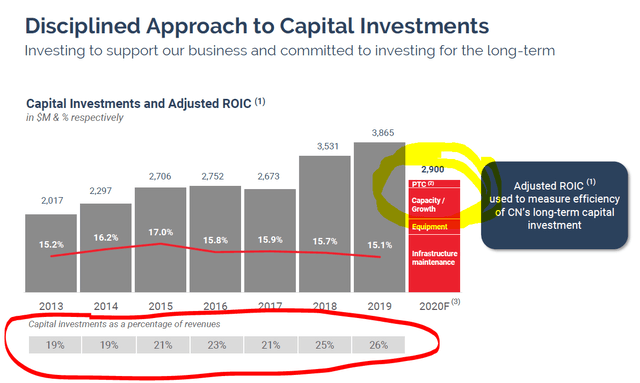

The metrics look good and the key metric for investing in Canadian Railway stock is the CAD $2 billion free cash flow. However, the CAD $4 billion in capital investments is relatively high compared to others and it might lead to significant cash flow growth in the future as capital investments decline and cash flows increase. The average investments for railroad stocks is 15% of revenue, CNI is spending 26%.

CNI stock analysis – Cash flow and investments – Source: CNI Investor presentation

If the current investment levels subdue over time, it could allow for higher cash flows to shareholders. It is likely that the company will create CAD$3 billion of free cash flows per year. Let’s take a look at fundamentals.

Canadian National stock fundamentals

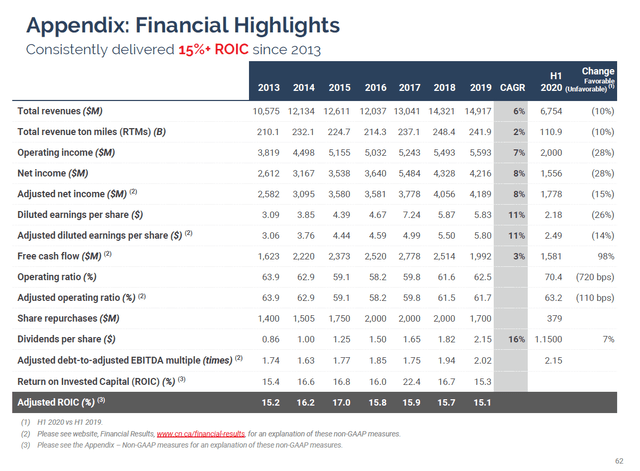

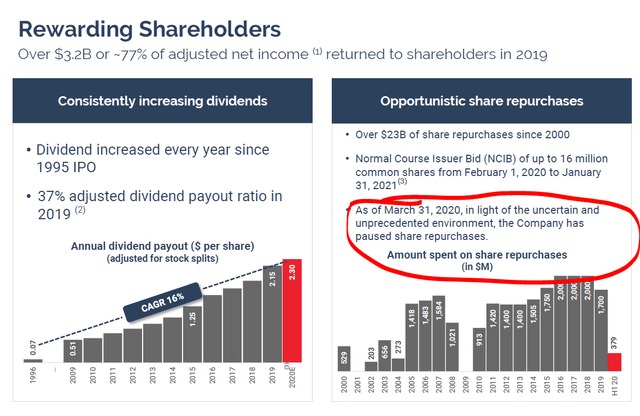

What is interesting is how revenue growth was relatively slow over the last years but operational efficiencies improved margins that allowed for dividends to grow at a 16% CAGR.

As is the case with other railroad stocks, price to book value is around 5, thus not a significant factor anymore as companies focus on cash flows and buybacks. Plus, if we would make a replacement cost analysis, I would assume book value would be much higher today because building 20,400 miles of tracks with all the infrastructure around it would be extremely costly these days.

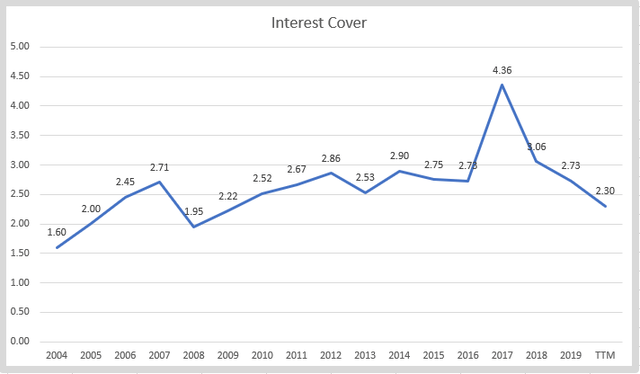

Interest cover has been improving and is almost twice as good as for competitors CSX and Canadian Pacific.

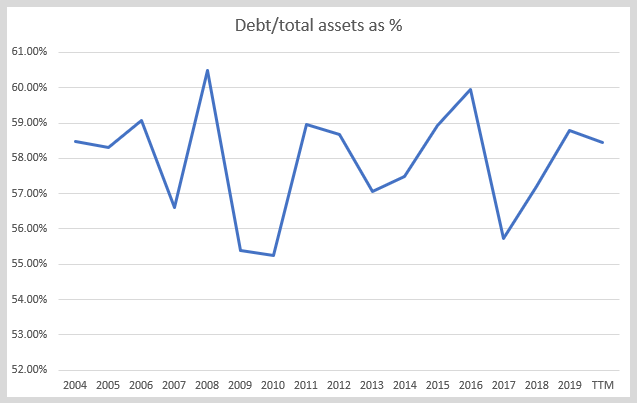

Debt to total assets is also lower than what the competitors have which gives the company more opportunity from a debt perspective to do buybacks and improve returns for shareholders.

Debt to free cash flow is 6, in line with all other rail stocks. Perhaps the only metric they all follow.

Due to the relatively high investment levels, free cash flow has been down in 2019 so to make a valuation I’ll use the likely free cash flow created when the investment cycle subdues.

The actual maintenance CAPEX is around CAD$1.5 billion while significant amounts are invested for future growth.

We could say CAD$ 2 billion are the actual CAPEX requirements per year which gives us with potential free cash flows at least CAD$3 billion that can be used to reward shareholders.

Canadian National dividend and buybacks

The company has increased its dividend at a staggering rate of 16% per year over the last decade and has also spend a huge amount on buybacks. Unfortunately, the buybacks were paused during the COVID related March 2020 crash and they didn’t take advantage of the low stock price but on the other hand the company played it conservatively.

With CAD $3 billion in cash flows I would argue the company will keep buying back stocks and increasing its dividend. If economic activity continues to grow, this will allow for more scale, improved operational efficiencies, higher earnings and dividends that should consequently push the stock price even higher.

Canadian National stock railroad sector comparative analysis

Compared to other railroad stocks, CNI is on the expensive side with a free cash flow yield of just 3% where we already assume free cash flows will increase from CAD$ 2 billion to $CAD $3 billion.

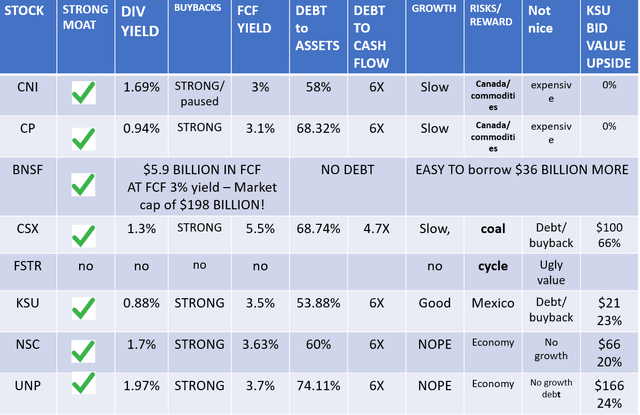

Other metrics like debt to cash flow, likely growth and the dividend yield are in line with what others offer. From a valuation point that takes into account the recent takeover bid for KSU, there is no upside for CNI stock because the takeover bid was made at a 3% free cash flow yield. Plus, CNI doesn’t offer the same growth opportunities as KSU. KSU stock analysis

For more information on other railways stocks, please check my comparative railway stocks article with links to detailed analyses such as this one.

If you like this comprehensive approach to investing, please subscribe to my newsletter to be notified when I analyse a new sector. To check my past analyses, covered stocks and portfolios, feel free to check my Stock Market Research Platform.