Union Pacific Stock & Dividend Analysis (Good Business)

Union Pacific stock price analysis

Union Pacific stock – NYSE: UNP

UNP’s stock price expansion is similar to all the other railroad stocks over the last 10 years. The performance has been amazing and those that dared to buy rail stocks in March of 2009 are now looking at returns of 1000%, not even including dividends.

However, that has already happened and the question now is whether to hold such a stock, buy it or sell it?

Union Pacific stock analysis content:

- Business overview

- UNP stock fundamentals

- UNP dividend and buybacks

- UNP stock investing thesis

This UNP stock analysis is part of my full railroad stocks sector analysis. Here is the:

If you prefer enjoying a coffee and listening to the content, here is the video on rail stocks, article continues below.

Union Pacific Business Overview

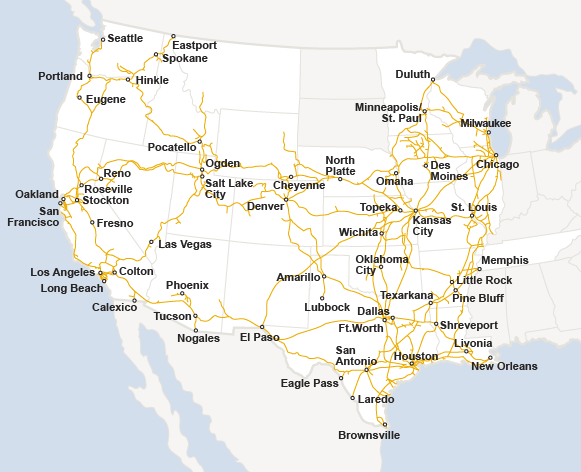

Union Pacific is a class 1 railroad operating across the center and west of the U.S.

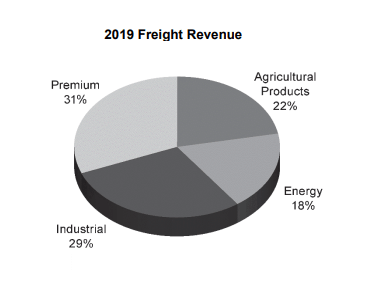

The freight revenue mix is diversified as is the railroad on the system map above so the business is not really exposed to any special trend or risk except for general economic activity.

The only problem with UNP might be its competitor, Burlington Northern that operates in the same area. I would not like to be in a business where my biggest enemy is Warren Buffett.

For now, it looks like the companies are cooperating well, revenue trends might slightly favor Burlington, but nothing significant.

UNP stock fundamentals

UNP is a railroad that hasn’t been growing for a while. The cash flows have been growing a bit but not really as fast as it has been the case with other railroads.

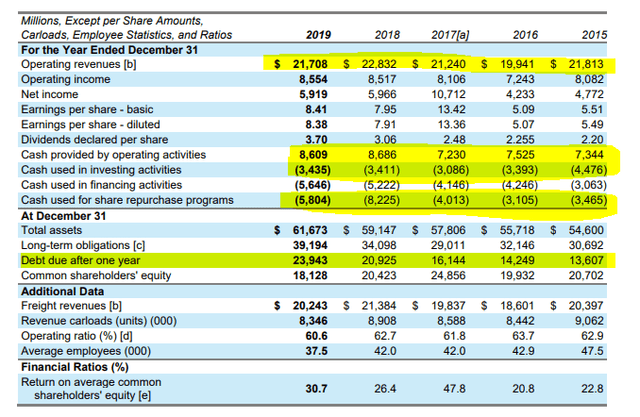

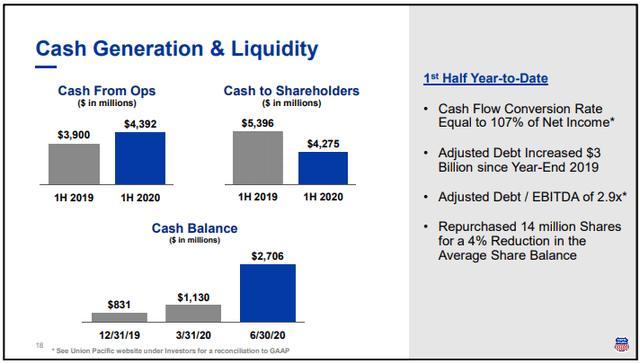

The free cash flows are around $5 billion given that operating cash flows have been $8.6 billion in 2019 while capital expenditures are stable at $3.5 billion. I expect the cash flows to stay stable at around $3.5 billion to $4 billion in the future.

As there is little hope for business growth, the goal is to just milk the cash cow and leverage it as much as possible to increase dividends and buybacks.

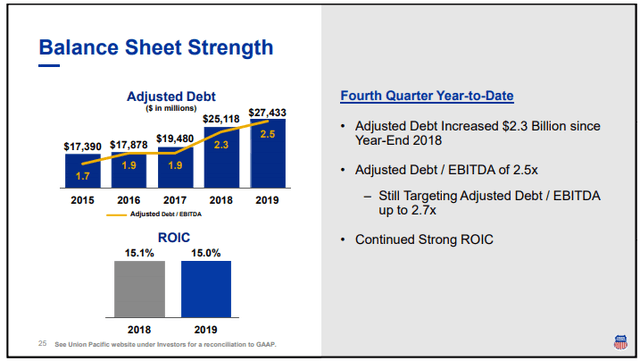

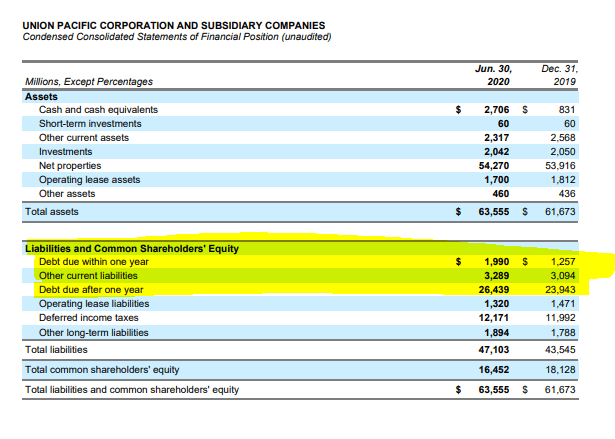

The company increased its debt from $17.3 billion to $27 billion over the last years. Actually to $32 billion if I don’t adjust the debt for the cash on the balance sheet.

Debt to free cash flow is exactly at 6, like it is the case with all other railroads.

Union Pacific dividend and buybacks

The company is spending more on rewarding shareholders than what it makes in free cash flows. This is pushing the stock higher but it is something that cannot be done forever.

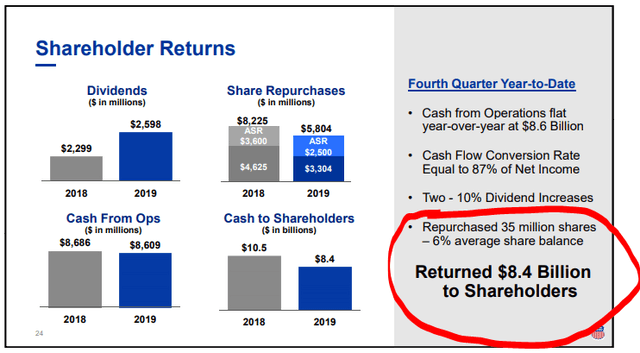

In 2019, the company returned $8.4 billion to shareholders while free cash flow was $5 billion.

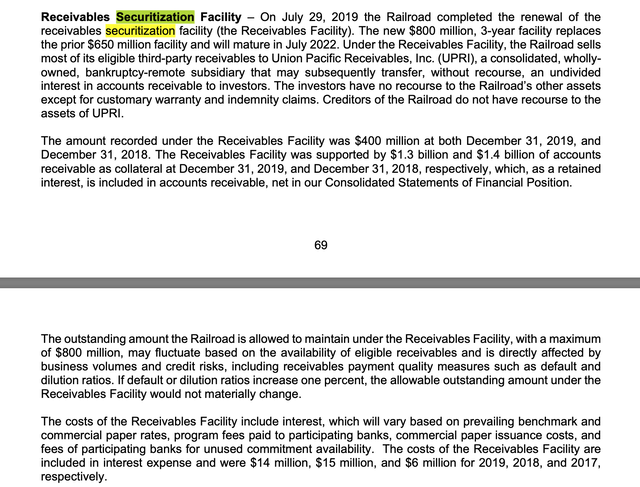

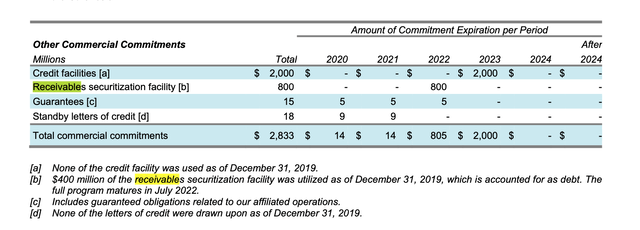

In order to have as much money for buybacks as possible, UNP is using some very questionable financial engineering called receivable securitization.

UNP sells its Receivables to a subsidiary (Union Pacific Receivables Inc) which raises money based on the receivables with third parties. They then loan this money back to themselves. In 2019 they increased the amount they are able to borrow from 650 mil to 800 mil. Using $1.3 billion of receivables as assets. This costs them around $14 million a year in interest expenses. The subsidiary is set up remotely so that it has no recourse to UNP assets etc. if things go wrong.

In this way they are able to show on their own balance sheets the $1.3 billion on assets they sold to themselves as Accounts Receivable – Net. Even though they have sold them (to themselves) because they still retain a residual interest.

This is just $1.3 billion and might not seem significant but borrowing from the future, as it is the case when increasing debt to do buybacks is something I don’t like as a long-term investor. It pushes the stock price higher for the moment yes, but I don’t think long-term GE investors enjoyed such financial engineering.

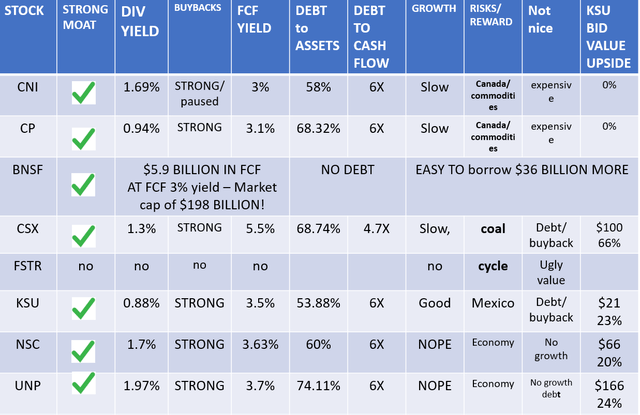

UNP stock compared to other railroad stocks

All in all, no growth except with the debt account on the balance sheet. UNP is another cash cow priced at a 3.7% cash flow yield. It doesn’t look much different from the rest of the pack except for a higher debt to assets ratio.

Investment returns for UNP shareholders will depend on how long will the buyback engineering last. At some point is bound to stop being able to push the stock higher and higher. If you don’t like owning a stock like UNP where the focus is on financial engineering, you might want to consider Burlington through Berkshire. (article to come)

For more information on other railways stocks, please check my comparative railway stocks article with links to detailed analyses such as this one.

If you like this comprehensive approach to investing, please subscribe to my newsletter to be notified when I analyse a new sector. To check my past analyses, covered stocks and portfolios, feel free to check my Stock Market Research Platform.