Flughafen Wien Stock Analysis – A Cheap Airport Stock (Third Runway Potential)

This Flughafen Wien Stock Analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian Stock Exchange and of my Airport stocks list. Austria is one of the cheapest stock markets globally at the moment so please check the Austria Stock List for interesting investments.

Airport stocks list with analysis

Flughafen Wien Stock – Vienna International Airport Stock Price Overview – VIE: FLU

Like for many other air travel related stocks, the Flughafen Wien stock price has been severely hit due to COVID-19. But it is still far above the levels in the early 2010s. Also, it is a cyclical business and consequently the stock is also cyclical. When things are good, investors get exuberant, while when things are bad, like it was the case in 2002, 2009 and 2012 investors tend to get scared. The market’s extreme psychology often creates opportunities for those that are greedy when others are fearful.

The Flughafen Wien dividend yield of 4.46% based on 2019 numbers is pretty high for an airport stock and the price to earnings ratio is of 14.16 is low. Of course, the dividend has been cancelled for 2020 and there also won’t be any profits for 2020, but it is a good benchmark to see what could the value be when things normalize.

This Vienna International Airport stock analysis will include:

- Business overview

- Growth potential

- Fundamental analysis

- Dividend analysis

- Risk and reward investment thesis

Flughafen Wien stock analysis – business overview

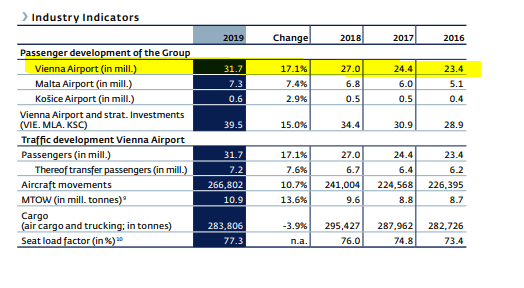

Flughafen Wien Stock or Vienna International Airport stock represents the Vienna International Airport, the Malta Airport and the Kosice Airport in Slovakia.

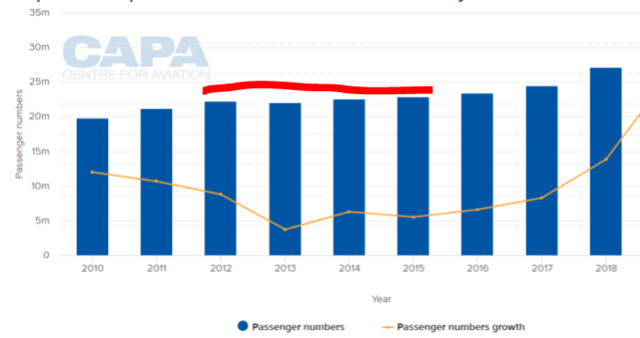

Unfortunately, due to the COVID-19 situation most airports are still and we don’t know when will the situation return to normality. But, normality has been great up till 2020 with the number of passengers increasing 50% from 2016. This is thanks to more domestic flying, the airport becoming a hub for transfers and also thanks to better load factors that went from 73.4% in 2016 to 77.3% in 2019. As said, more people more money for the airport. The growth is also thanks to the previous investments that were made for a second runway and new terminals.

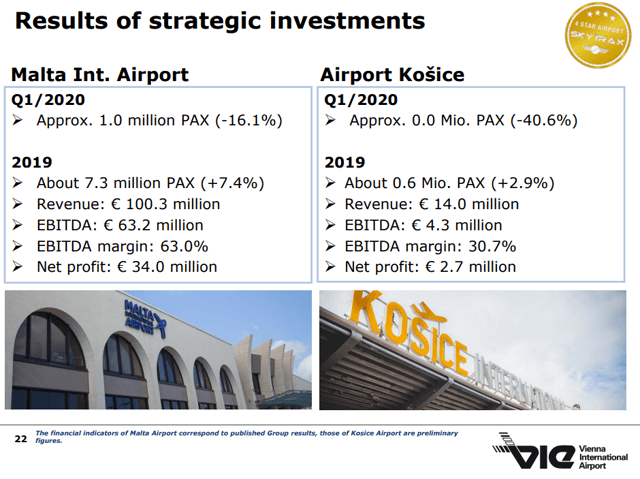

Growth has been similar within the two strategic investments: Malta and Kosice airports.

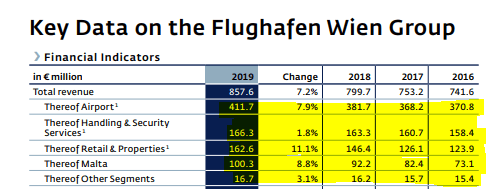

Revenues have been steadily increasing as the economic situation was good and the airport developed into a transfer hub offering cheaper options to carriers than competing cities like Frankfurt, München and Zurich.

However, traffic had even declined in 2013 and has been flat for a while before booming.

Vienna International Airport Stock analysis – Growth opportunities

As for investments, Hangar 8 and Hangar 9 were recently completed. They are modernizing Terminal 2 and the Plaza while the Office Park 4 office complex is almost completed. Other projects such as the southern extension, the conversion of Pier East and the planning and preparatory work for the third runway have been postponed for the time being.

However, the intention to build a third runway, a new pier and adjacent things shows how there is still room to grow for the airport. The key is also that the third runway has been approved.

But, we as investors also need to mind the costs of such an effort. The costs to build the second runway were 770 million EUR while the expected costs for the third runway go from 600 million to 1.2 billion EUR which would be a heavy burden for the company and such an investment would require a continuation of the strong growth rates. For now, especially with COVID-19, the management will try to fill the free slots it still has, especially in off-peak hours and then make the decision on the third runway in the future.

If traffic grows at 5% per year, as the expected airline traffic growth is, then shareholders will be well rewarded over the next decades. Let’s take a look at the fundamentals and also check how the possible billion growth plan would fit the balance sheet.

Vienna International Airport Stock Analysis – Fundamentals

The first thing to note is how the business works. They take on debt to invest and build, then lower the debt levels as things go well and the projects are completed. This allows for higher dividends.

Further, small increases in revenues have a huge impact on the bottom line as the costs don’t go up at the same rate as revenues.

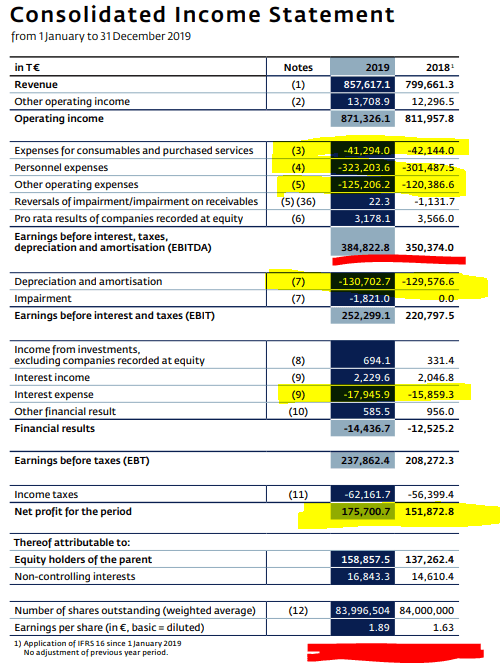

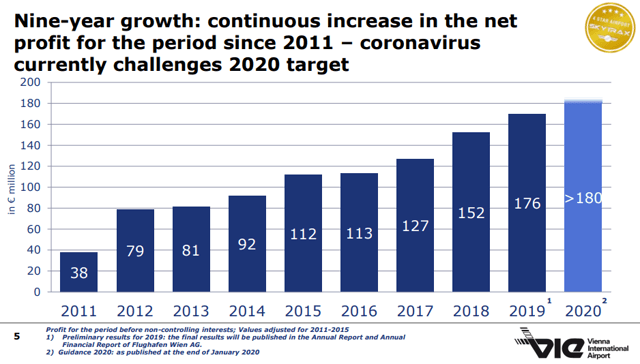

In 2019, revenue grew 7.2%, from 799 million to 857 million while ne profit grew 11.4% from 151 million to 175 million. If they can keep growing over time, build the third runway and constantly increase traffic, the business will reward shareholders for a long time.

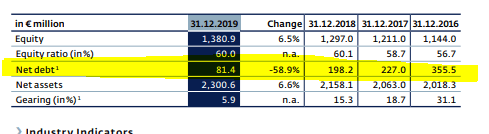

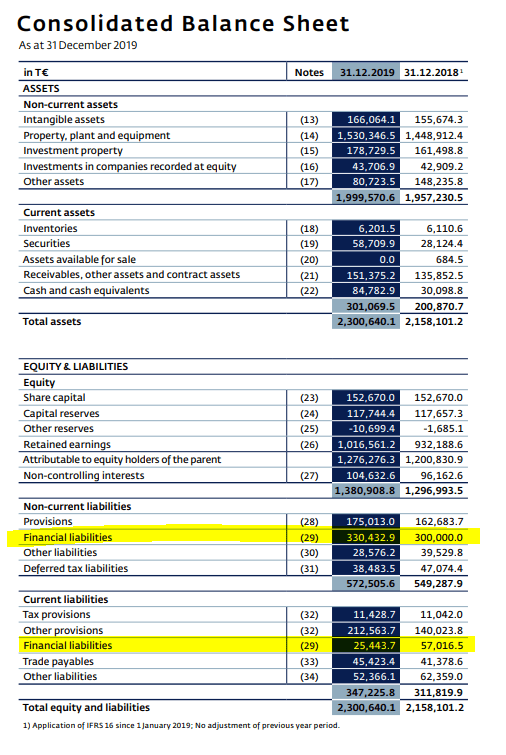

Total financial debt is 355 million on equity of 1.38 billion which is a low debt rate. If growth continues, I don’t think it would be an issue to set up the financing to build a third runway and leverage the balance sheet with almost a billion.

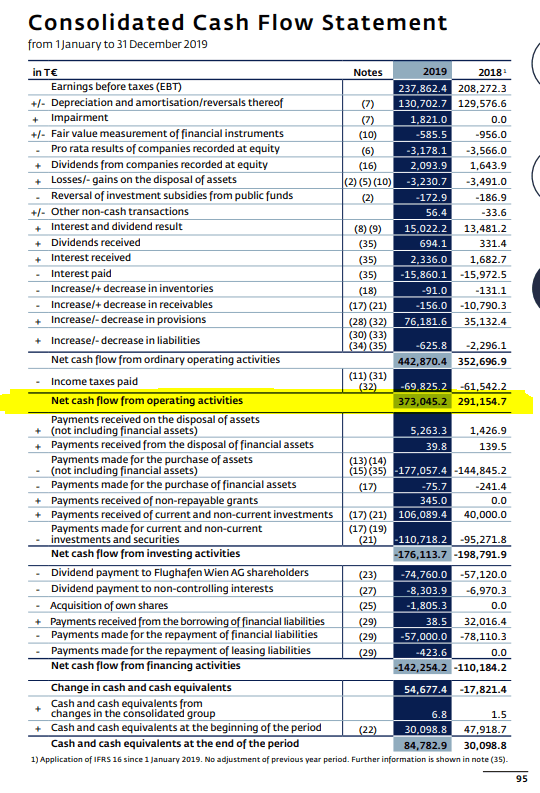

On operating cash flows of 373 million, if they borrow one billion, they could repay it in 3 good years, not even counting the growth coming from the expansion. The key question is whether there will be enough growth to justify the investment as competitors are not staying still and the population in Europe isn’t really growing.

All in all, with operating cash flows of 373 million, the business with a market capitalization of 2.1 billion looks incredibly cheap. Of course, if the COVID-19 situation remains just a 2020 issue and things return to normal in 2021. They forecasted capital expenditures of 230 million for 2020 but that includes also investments. This will be closer to 100 million now. I would assume sustaining capex to be at around 100 million over the long-term which would create free cash flows of around 273 million in a good year. The key question is when will the next good year come?

Wien Flughafen Stock Analysis – Investment thesis

If we model a valuation on 273 million EUR of free cash flows per year and 5% growth ahead, the stock is ridiculously cheap at a market capitalization of 2.1 billion as long as the investments are made at satisfying returns on capital. The key question is of course when will things return to normal? Given the situation, it is unlikely we will see a lot of improvement in 2020.

Given it is an airport, you can’t really use book value for valuation because the value is not in the concrete poured but in the possible cash flow that the business will generate in the future. They show assets of 2.3 billion but on 273 million of cash flows, the value is likely higher. Again, if things return to normal.

If they manage to grow earnings at 7% per year over the next decade, it doesn’t have to be in a linear way, profits in 2030 would be 346 million. Then, depending on interest rates the likely valuation could be close to 7 billion on a price to earnings ratio of 20. Without counting dividends, that would give a return of 12.7% per year to current shareholders. If we add a likely dividend yield of 3%, we are close to 15% yearly returns which would make it a staggering investment.

Wien Flughafen Dividend

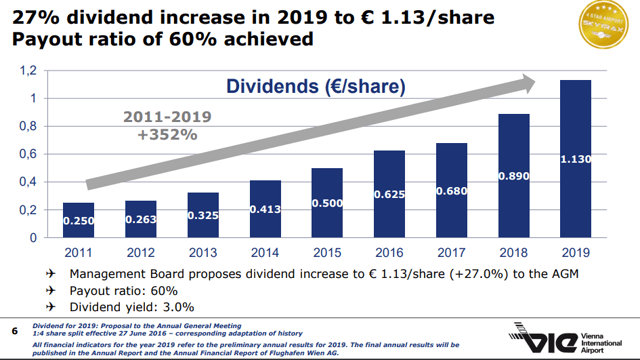

Wien Flughafen dividend has been increased alongside the growth in earnings.

The dividend has currently been suspended but past performance shows what can investors expect from a dividend perspective. Perhaps, when the investment cycle is over, the pay-out ratio might even increase and the stock might become a pure cash cow. On a 100% pay-out ratio, which is possible as you have to build your runway once and then enjoy the benefits, the dividend yield on current cost in 2030 could be above 15% if the above discussed assumptions are met.

Vienna Airport stock analysis – Investment conclusion

At this moment in time, with uncertain rewards, the investment thesis is more about whether you wish to own an airport and how does that fit your portfolio where the rewards are uncertain.

If things return to normal, the returns will be in the teens and shareholders that dare to buy Wien Flughafen stock now will be rewarded. If economic and travel activity doesn’t pick up, this could become an ugly investment but that is what investing is all about. On one hand we have unlimited upside while all we can lose is what we invest or simply own something where nothing happens for a while.

I don’t believe the world will stop, so Wien Flughafen stock looks like a good investment at the moment. I will continue with my Austrian stocks analysis and also add a new list that covers airport stocks where you can will be able to read my initial analyses on airports. For now, Wien Flughafen looks like a safer investment than related airline stocks that we have analysed like FACC stock analysis or DO & CO stock analysis, the airline catering company.

The Wien Flughafen Stock Analysis is part of the full Austrian Stock Market Analysis and of my Airport stocks analysis made by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundred of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: