FACC Stock Analysis Dividend & Risks

FACC Stock Analysis – Vienna: FACC

This FACC stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian Stock Exchange. Austria is one of the cheapest stock markets globally at the moment so please check the Austria Stock List for interesting investments.

This FACC Stock Analysis consists of the following segments:

- FACC Stock Price Overview

- FACC Stock Business Overview

- FACC Stock Fundamentals

- FACC Stock Dividend

- FACC Stock Investment Thesis

FACC Stock Price Overview

FACC went public with an IPO and a stock price of 9.5 EUR in 2014. Unfortunately for shareholders, the rewards haven’t been stellar.

In the first two years from the IPO, the company wasn’t profitable alongside negative free cash flows and consequently investing returns weren’t much. In 2017 the stock spiked on positive earnings and growth to reach a high of 23.2 EUR in 2018 only to decline 74% since.

The market capitalization is small at 280 million EUR, especially when compared to revenues of above 700 million. Let’s see whether the stock offers the potential to reward shareholders like it did over 2017 and 2018 and whether it might be able to sustain the performance.

The 55% owner of the company is the Aviation Industry Corporation of China (AVIC). AVIC acquired FACC AG in 2009 and it was the first Chinese acquisition of a western tier 1 aircraft supplier.

FACC Stock Business Overview

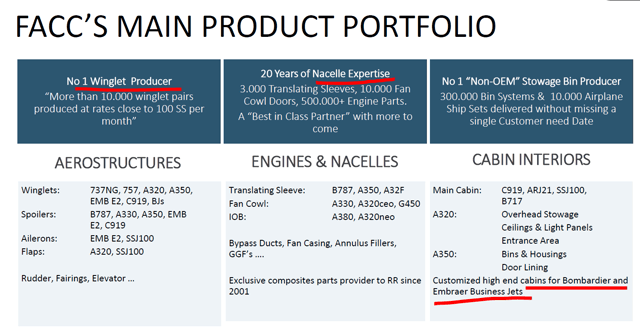

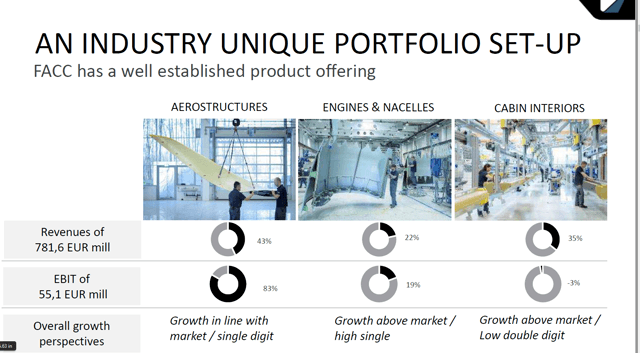

FACC AG is an aerospace company that designs and produces special components and systems and is a partner to all major aircraft manufacturers. The focus is on lightweight components, engine expertise, cabin interiors and maintenance.

When it comes to the aerospace business, it all depends on the cyclical demand. Yes, the market had been expected to grow at 5% per year over the coming decade, but that was prior to the COVID-19 virus.

Now, we don’t know how will the environment look like, how long it will take to surpass 2019 levels and how long it will take for airlines to absorb the created oversupply of aircrafts as many companies have gone or will go bust. The thing is that the stock has actually been declining since 2018 already, COVID-19 was just the final blow. Therefore, I would conclude here that the outlook is bleak as their products are pretty standardized and the revenue depends 100% on how many planes are sold in the world. However, the best investments are made when things look ugly and turn for the better.

The company’s current target is to grow as the market grows. Their organic growth won’t be as it was in the past decade where they tripled revenues and the managements’ main focus for growth is an increase in demand for their products due to more travelling thanks to population growth and development.

Their second business focus, where they hope to achieve growth are the following vehicles:

But, it seems to mee that if and when these flying cars get any traction, the competition will be extreme.

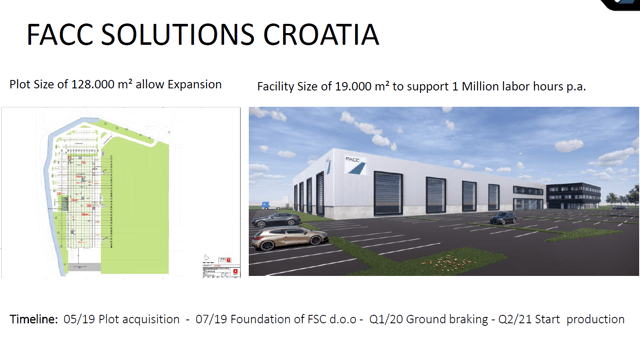

They have started with a significant investment in Croatia, but that has been delayed given the current aerospace environment. They goal was to make a low-cost production facility and improve their thin margins.

The thing is that the airline industry is extremely difficult. Airbus will simply buy the parts they need from the cheapest supplier and if they don’t need the parts, they will simply not buy them. So, the cyclicality of the sector is felt across the complete supply chain. I have analysed the airline industry here and feel free to read it if you wish to get a better sense of what investing in airlines and related businesses means. Another airline related business that we have analysed from Austria is DO & CO AG that has also been hit by COVID-19 and the situation is similar although the business is different – catering.

FACC Stock Fundamentals

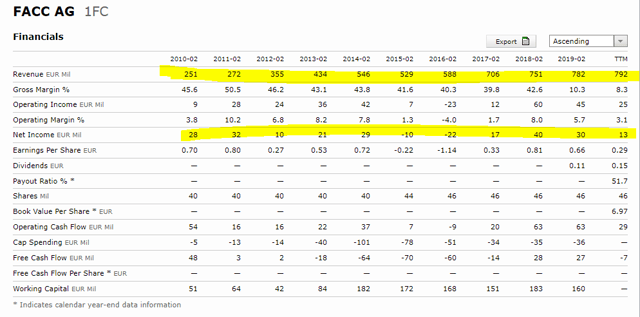

FACC’s stock fundamentals look shaky at the first look as EBIT isn’t anything special on the high revenues and where the cabin interiors segment that makes 35% of revenue isn’t even profitable.

Earnings have been volatile since the IPO and will likely remain so in the future as such is the industry. I did listen to Ryanair’s CEO during a conference call in 2019 and he said how new planes are too expensive due to high demand and that margins will return to the norm eventually. That happened sooner than expected but this also means it will be hard for FACC to increase margins.

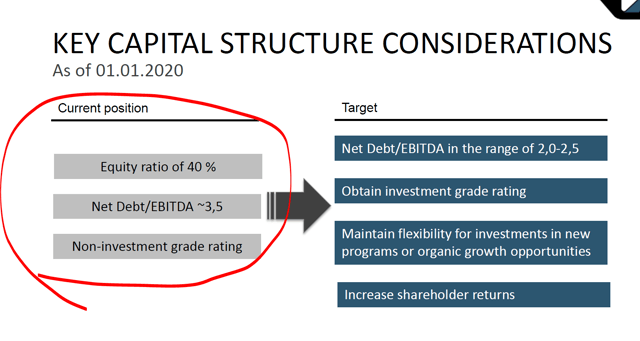

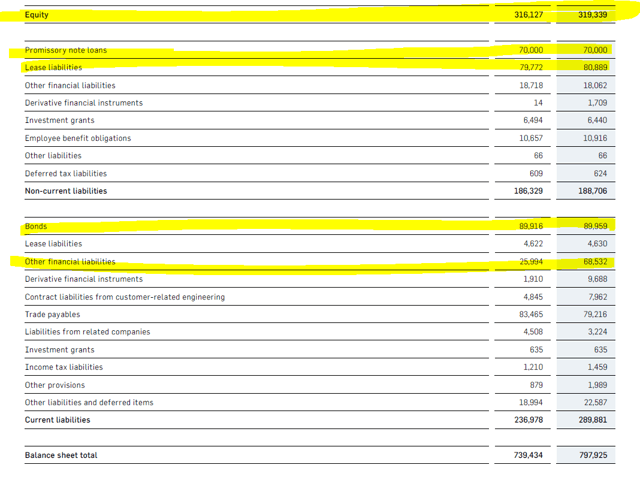

Their financial position was already shaky before the current crisis so I can imagine they are in for even more trouble at the moment. The net debt to EBITDA ratio was at a high level of 3.5 and given the situation, it is likely they will not reach their lower debt targets anytime soon.

However, if and when they reach their targets and improve margins, then the story could be really good for shareholders.

FACC’s revenues have been growing fast since the 2009 acquisition but the margins have always been really thin.

The stock is now trading below book value, but with the situation and with the high debt levels compared to their equity and market capitalization, things might get tricky for shareholders. So, even the book value per share perceived safety can quickly change with dilution or impairments.

One might argue that the owner’s target might not even be to make this company highly profitable but to simply get the technology and learn more about building aircrafts through producing for Airbus and Boeing. I would not be surprised that if the stock falls further, the owners decide to take it back to private at al lower prices than the IPO price (this is a risk with such small companies and happens often, especially in China)

FACC Stock Dividend

The company did pay a small dividend in the past but that has been waived due to the uncertainties related to the current COVID-19 situation, likely breach of bank covenants and low liquidity levels.

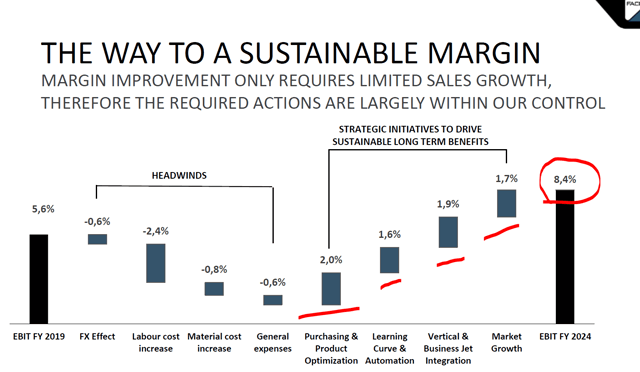

They might reinstate the dividend but I don’t think it will happen soon as their debts will surely increase over 2020 and 2021 and thus postpone the dividend for longer. Plus, given the highly competitive environment, it is also hard that they reach their targeted margin of 8.4% by 2024 and increase dividends over time.

FACC Stock Outlook & Investment Thesis

The outlook for FACC stock isn’t positive as even the management sees losses ahead both in 2020 and in 2021. They recently managed to refinance their bond, which is a positive thing and the main questions regarding investing in FACC stock are the following:

- When will things return to normal in the industry?

They expect a swift return to normality as that has been the case for the industry in the past. However, now the issues are of regulatory form and not just fear of flying or economic slowdown.

- Will they company ever reach higher margins and is it their goal after all?

It is an extremely competitive environment with several players. Thus, Boeing and Airbus are the winners.

- Even if things return to normal one has to keep in mind the constant cyclicality and fragility of the airline industry, plus the owner’s intentions.

What will be the next thing hitting the industry?!?

- If we start flying around with our cars, the competition there will be extreme and we can’t even know if the businesses segment for FACC would ever be profitable.

None of the business segments are profitable now, so not likely that will change over the long-term as we are in a highly competitive business where the returns on capital for investors have been negative even since the Wright brothers first took flight.

I am not going to follow FACC stocks because I prefer safer investments, with higher long-term potential and I also don’t want to depend on the Chinese government dealing with my shareholder rewards.

I would categorize FACC stock as a high risk, high potential reward investment. High risk because of the environment, the thin margins, high competition and negative industry returns given no competitive advantage. On the other hand, there could also be high reward because the market always looks at the last year or two and then projects the story into the future not minding cycles. If FACC manages to deliver two years of 8% EBIT margins on growing revenues, the stock might explode again like it did in 2018. On 800 million EUR in revenues, an 8% EBIT margin would lead to 64 million in EBIT and likely 50 million in net profits that would give earnings of 1.11 per share. Put a normal European price to earnings ratio of 20 onto that and you are soon in the 20s with the stock price.

If one really wants to get the low risk/high reward investment opportunity with FACC stock, one has to closely follow the business, possible business improvements that are likely to be sustained over a year or two and then buy when things start to turn for the better. This might happen only once in the next decade, but it might happen. Unfortunately, the current fundamentals don’t make it safe enough to just hold it and wait for an improvement in the environment. Also, if you own it, keep in mind the risks related to the industry, ownership and potential dilution if the situation doesn’t recover soon.

We will continue with the analysis of other, hopefully less risky stocks traded on the Austrian stock exchange.

The FACC Stock Analysis is part of the full Austrian Stock Market Analysis make by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundreds of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: